Why are US distributed solar customer acquisition costs still on the rise?

Installers grow weary of investing further in marketing strategies amidst a residential market slowdown

5 minute read

As interest rates have risen and customer demand has weakened over the past year, residential solar installers are finding it increasingly difficult to acquire new customers. Customer acquisition costs remain the most expensive category within the residential solar cost stack, which is not expected to change anytime soon.

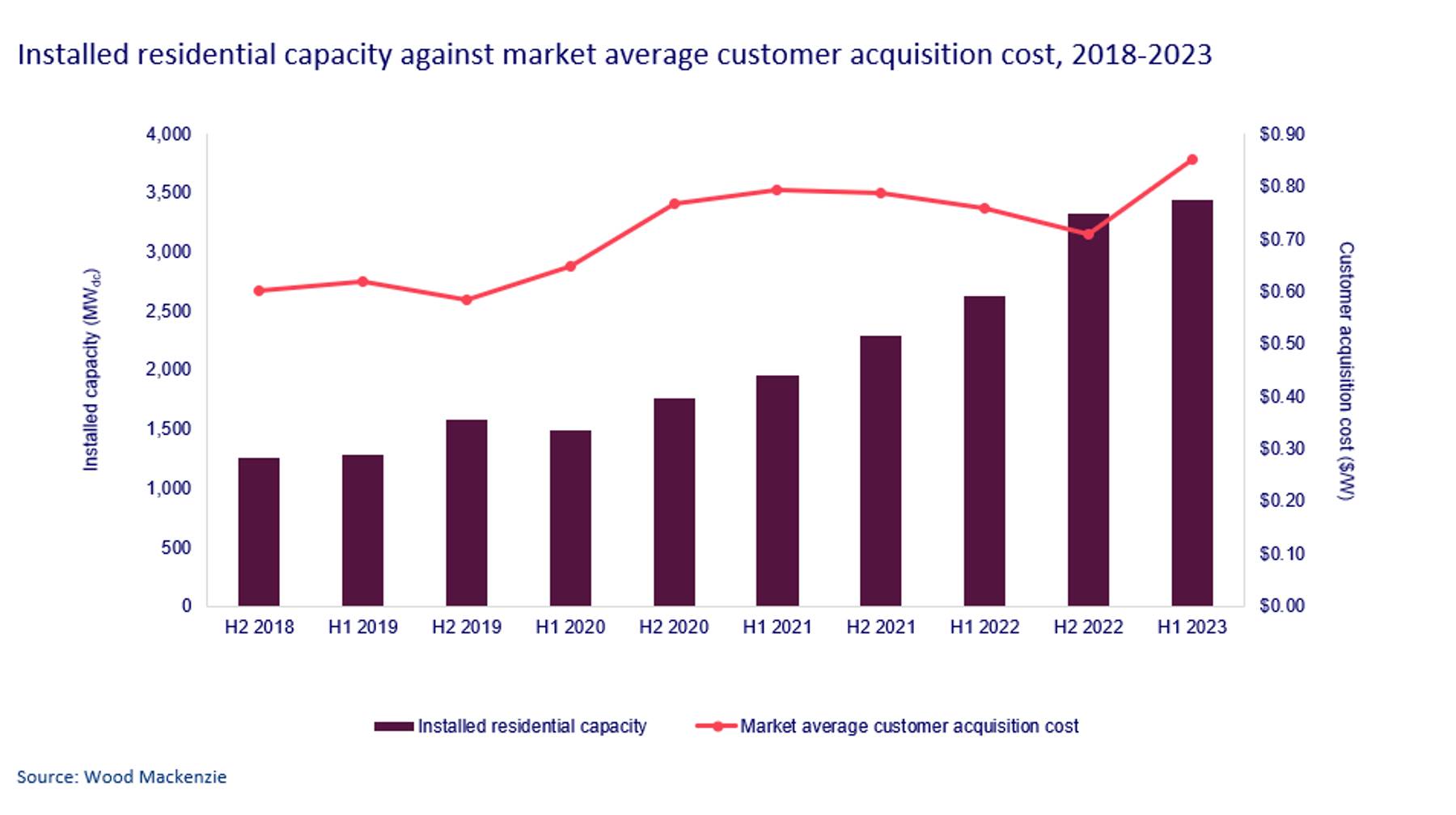

Customer acquisition costs were expected to decline in the years following 2021 as the COVID-19 pandemic drove large investments in digitalization. The wide adoption of digital sales and software solutions can create more operational efficiencies for installers, which would result in decreased costs in the years following. So, why is this not the case two years later? Residential customer acquisition costs reached a record high of $0.85/W in H1 2023, a 13% increase from H1 2022. A slowdown in residential solar demand is primarily driving increases in customer acquisition costs.

Wood Mackenzie’s US distributed solar customer acquisition cost outlook 2023 highlights recent trends and forecasts in customer acquisition costs and strategies in the residential and community solar markets. Fill out the form on the right to access a complimentary extract from the 2023 report, or read on for some key highlights.

Economic headwinds and consumer hesitancy in the US residential solar market make for a difficult environment to acquire new customers

After a brief decline in 2022, customer acquisition costs are once again on the rise. As national residential solar installations rose in 2022, customer acquisition costs inversely fell. This decline did not last long, however, as costs jumped almost $0.15/W from H2 2022 to H1 2023. High interest rates and consumer hesitancy are persistent trends in 2023, contributing to the struggle for installers to close sales.

At $0.81/W, customer acquisition costs are the highest cost category in the residential solar system cost stack, ahead of $0.49/W for modules. According to Wood Mackenzie, the total residential solar system price will decrease by 2% on average annually through 2028, whereas customer acquisition costs will decline by 1% annually on average. Soft costs, such as customer acquisition costs, are a potential area of optimization for installers that can lead to increased revenue and potentially more favorable pricing for customers. Stiff market competition and tight budgets for sales and marketing investments leave many installers with no choice but to pay higher customer acquisition costs, leaving little wiggle room in pricing.

{kind=link}

Customer acquisition costs and installation volumes tend to have an inverse relationship, but the first half of 2023 proved that trend wrong. Installation backlogs created under California NEM 2.0 and high retail rates in some states contributed to overall strong H1 2023 installation volumes. However, growth was not as strong in traditionally larger markets with lower retail rates and many installers reported a continued decline in sales during this period.

Installers now face tough decisions on the riskiness of investing in marketing while trying to stay afloat in a contracting market. Despite the market slowdown, many installers have increased or kept marketing budgets the same to keep up with competition, driving up acquisition costs. Wood Mackenzie expects that costs will continue to increase up to $0.87/W in 2024 as the residential market contracts by 4%. After 2024, we expect acquisition costs to decline by 7% on average through 2028.

Larger installers who can afford to invest during low sales periods may not feel the impact of the residential market slowdown as intensely. Sunrun has been able to increase their sales and marketing budget by an average of 6% per quarter since Q2 2022 to drive demand in a contracting market. This investment has been uniquely effective, as their customer acquisition costs have in turn decreased by 23% year-over-year in Q2 2023, despite the market average increasing.

Customer acquisitions cost are also on the rise for community solar developers

Although community solar is an entirely different business model than residential solar, there are distinct similarities in customer acquisition strategies that residential installers and community solar developers use. In both cases, customer acquisition tactics require a high level of community engagement and trust building to ensure success.

Although the cost of acquiring community solar customers has also increased over the last few years, a decrease in community solar demand was not the driver. Instead, as community solar programs evolve, more and more states implemented strict requirements for low-to-moderate income (LMI) subscription levels. Acquiring LMI customers is nearly two times more expensive than acquiring non-LMI residential customers on a $/kW basis. Therefore, as the share of project capacity subscribed by LMI customers increases, customer acquisition costs will also increase. To minimize these costs, community solar developers almost always partner with a third-party subscriber management company. These companies have regional expertise and often utilize software tools to optimize cost efficiency.

Installers are reluctant to invest in new growth mechanisms

The use of virtual sales spiked during the COVID-19 pandemic, as installers heavily invested in digitalization. However, despite previous predictions that virtual sales would continue to grow, most installers returned to in-person sales. Investments in digitalization did not pay off as expected, as economic headwinds forced installers to return to elementary business practices.

Although many installers are hesitant to increase investments while competing for market share, software tools can draw in more potential customers. Lead generation platforms and third-party sales organizations can create efficiencies and produce cost savings for installers, leading to greater customer satisfaction and increased referrals, two key elements for installer growth.

Software solutions give installers the opportunity to close the gaps where failure most often occurs. Customer satisfaction typically drops around the close of sale stage, after customers have signed the contract. Software solutions can alleviate customer anxiety during the installation process by automating communication between customers and installer, making sure customer queries do not go unanswered.

Although the cost to acquire residential solar customers has not yet reached its peak, a hopeful future of decreasing costs is not far away. We expect installers to feel the effects of the market slowdown for the next year, but customer acquisition costs will steadily decline from 2024 to 2028. Software solutions remain a key factor in optimizing efficiency, lowering soft costs for installers, and improving customer experience.

Learn more

For a closer look at our US distributed solar customer acquisition cost outlook, fill out the form at the top of the page to download your complimentary extract of our US distributed solar customer acquisition cost outlook 2023 report.