Wind from the east gathering strength: the outlook for OEMs

With the growth outlook for onshore and offshore wind looking healthy, Chinese wind turbine OEMs are hungry for global expansion

3 minute read

Endri Lico

Principal Analyst, Global Wind Supply Chain and Technology

Endri Lico

Principal Analyst, Global Wind Supply Chain and Technology

Latest articles by Endri

-

Opinion

Wind supply chain financials decoded: colliding margins and rising prices

-

Opinion

Onshore wind: diverging cost trends, converging turbine maker strategies

-

Opinion

Future wind installations: the great divide between Chinese scale and Western strongholds

-

Opinion

Liberation Day tariffs threaten to disrupt US wind and solar industries

-

Opinion

New frontiers: order intake by Chinese wind turbine OEMs advanced beyond domestic dominance in H1 2024

-

Opinion

Wind from the east gathering strength: the outlook for OEMs

We expect healthy growth in demand for onshore and offshore wind generation over the next ten years, providing a firm foundation for wind turbine manufacturers to build on across the board. But how are market dynamics evolving and who will be the biggest winners?

We recently published an in-depth forecast of market share by region for wind turbine OEMs in both onshore and offshore wind markets globally over the next ten years. Fill in the form at the top of the page to download a complimentary extract from the report, and read on for some key takeaways:

1. All wind OEMs will double their connected capacity over the next decade

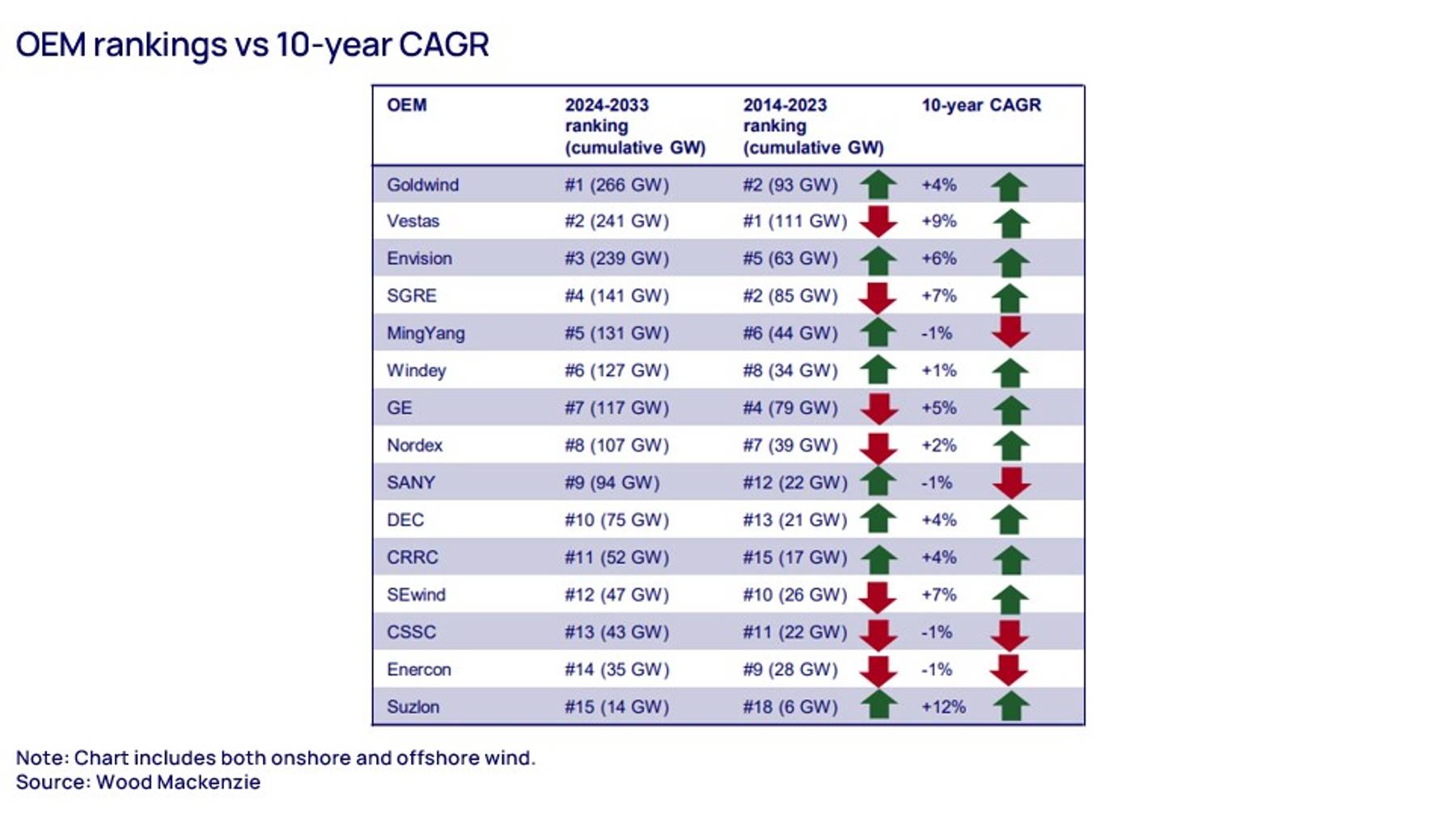

The prospects for original equipment manufacturers (OEMs) supplying the onshore and offshore wind sectors look robust over the next decade. We expect total wind demand to double by 2033, requiring the installation of nearly 25,000 new turbines. As a result, all the major wind OEMs will double their connected capacity. At an overall global level, Chinese firms Goldwind and Envision and Danish company Vestas stand out from the pack, each connecting above 300 gigawatts (GW) cumulatively over the entire forecast period. Goldwind will be the annual leading manufacturer through to the end of the decade, with Vestas rebounding to the top position from around 2030 onwards.

2. Chinese OEMs are hungry for overseas expansion

Chinese wind turbine manufacturers already completely dominate their home market, with soaring demand (fuelled by provincial targets) ensuring steady production volumes. However, fierce domestic competition is hitting profitability and driving OEMs’ ambitions to expand elsewhere. China’s Belt and Road Initiative provides a useful gateway into emerging markets in this respect, allowing firms to leverage the country’s existing international footprint, along with gigawatt-scale hydrogen projects.

Overall, Chinese OEMs will build 20% of global demand outside of China over the next decade, with Envision and Goldwind leading the export push. These firms are thriving in the Middle East, Africa and Central Asia, while also presenting fierce competition to Western OEMs in Latin America and the rest of Asia Pacific. Their success is largely thanks to economies of scale, lower prices, and expertise in power system integration.

3. Western OEMs remain focused on their core markets

The EU and the US remain strongholds for Western OEMs due to firms’ entrenched positions, bolstered by protectionist policies and energy security concerns that favour domestic supply. These mature markets are well protected from Chinese imports by measures including financing, permitting, health and safety requirements, and project sizes. As a result, a shift in focus by Western OEMs towards profitability over volume – and therefore local markets over expansionism – is paying off in the short term.

Going forward, Western OEMs GE and Nordex Acciona will continue to focus their attention close to home, capitalising on strengthening demand in the US and European Union respectively. Elsewhere, however, Chinese manufacturers have already benefited from the vacuum created as Western OEMs prioritised their core markets. Continuing project selectivity and higher turbine prices from Western firms could help open the door further for Chinese companies to fill the resulting gap in the market.

4. Siemens Gamesa and Vestas control almost 90% of the global offshore markets, excluding China

Offshore wind turbine demand will soar in the coming decade, offering vast opportunities. Siemens Gamesa maintains its leading position in the offshore market, helping compensate for lost revenue in the onshore sector caused by quality issues with its two newest turbine models. Vestas is also thriving in offshore, capitalising on V236 success, which has already concentrated above 18 GW of accumulated orders, while GE exercises selectivity on new projects and focuses on executing its current backlog.

{kind=link}

Learn more

Don’t forget to fill out the form at the top of the page to access your complimentary extract from the full report, which includes a range of charts and data exploring these themes in more detail.