Get in touch

-

Mark Thomtonmark.thomton@woodmac.com

+1 630 881 6885 -

Hla Myat Monhla.myatmon@woodmac.com

+65 8533 8860 -

Chris Bobachris.boba@woodmac.com

+44 7408 841129 -

Angélica Juárezangelica.juarez@woodmac.com

+5256 4171 1980

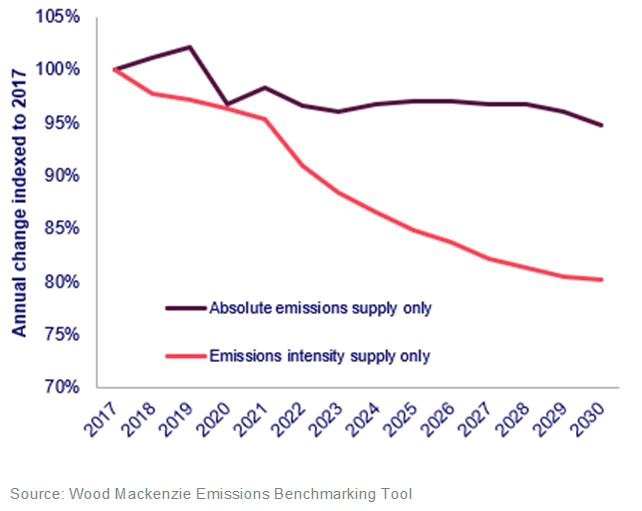

Upstream scope 1 & 2 emissions intensity down 12% since 2017, but more work is needed on absolute emissions

Despite the industry’s decarbonisation efforts, higher production volumes will push total value chain emissions to pre-pandemic levels by 2028

1 minute read

Scope 1 and 2 upstream emissions intensity has declined 12% since 2017, however, absolute emissions could plateau due to production growth, according to a new report from Wood Mackenzie.

According to the report “Is upstream oil & gas delivering on decarbonisation?” Wood Mackenzie finds that while flaring reduction, methane detection and repair, electrification, and CCUS have put quite a dent in emissions intensity, higher volumes are increasing absolute emissions in some regions. Including the other components of the oil and gas value chain, absolute emissions could exceed pre-pandemic levels by 2028.

“Flaring, methane, and venting initiatives show that progress can be made, but efforts need to move beyond the low-hanging fruit,” said Adam Pollard, principal analyst with Wood Mackenzie. “For example, over 10 bcf of gas is still flared daily. Overall upstream emissions remain intrinsically linked to production. Combustion emissions remain the largest sources, but progress on abatement has been limited. Electrification can deliver big reductions but only where low carbon power is available.”

Majors and International Oil Companies (IOCs) have led the way on emissions intensity improvements, driven by net-zero commitments and increasing regulations and carbon taxes. However, National Oil Companies (NOCs) account for 51% of upstream emissions and not all have followed the IOCs lead, according to Pollard.

Super emitters play a significant role as well, with half of the upstream sector’s emissions coming from just 165 oil and gas fields. This category includes persistent flarers, giant Middle East fields, oil sands projects and integrated LNG.

“Moving forward, new developments will have lower than average industry emissions and companies will use M&A as a lever to maximise the proportion of advantaged barrels in their portfolio,” said Pollard. “However, many companies and governments have catching up to do. Ramping up efforts on emissions starts with setting targets, developing decarbonisation strategies, joining existing decarbonisation initiatives and learning from the Majors, IOCs and NOCs that are already on the journey. “