Get in touch

-

Mark Thomtonmark.thomton@woodmac.com

+1 630 881 6885 -

Hla Myat Monhla.myatmon@woodmac.com

+65 8533 8860 -

Chris Bobachris.boba@woodmac.com

+44 7408 841129 -

Angélica Juárezangelica.juarez@woodmac.com

+5256 4171 1980

Bulks most affected by Russia-Ukraine conflict; rising power prices a key concern

1 minute read

Trade dislocations due to sanctions, high power prices and disruption to production facilities in the conflict zone are three major threats to the metals and mining industry as result of escalating conflict between Russia and Ukraine, says Wood Mackenzie, a Verisk business (Nasdaq:VRSK).

Wood Mackenzie vice president Robin Griffin said: “The impact of any sanctions will depend on the exact nature of constraints put on Russian commodities and companies. Russian trade has typically stood up well during past sanctions, but previous policies have been very targeted, often focussed on individuals and specific companies. A Europe-wide or UN-led global approach would be a unique challenge.

“The most likely outcome of a strict EU sanctions regime would be that affected Russian-sourced commodities are re-directed and a trade shift would see European demand backfilled. But the shift will be messy, and there are often more constraints than expected due to quality differences.

“Suppliers hesitate to divert tonnes when there is no guarantee that the sanctions will last. The price premium required to justify the shift is often much greater than a simple analysis of the change in supply and demand volumes. China’s ban on Australian coal imports has provided a salutary lesson in that regard.”

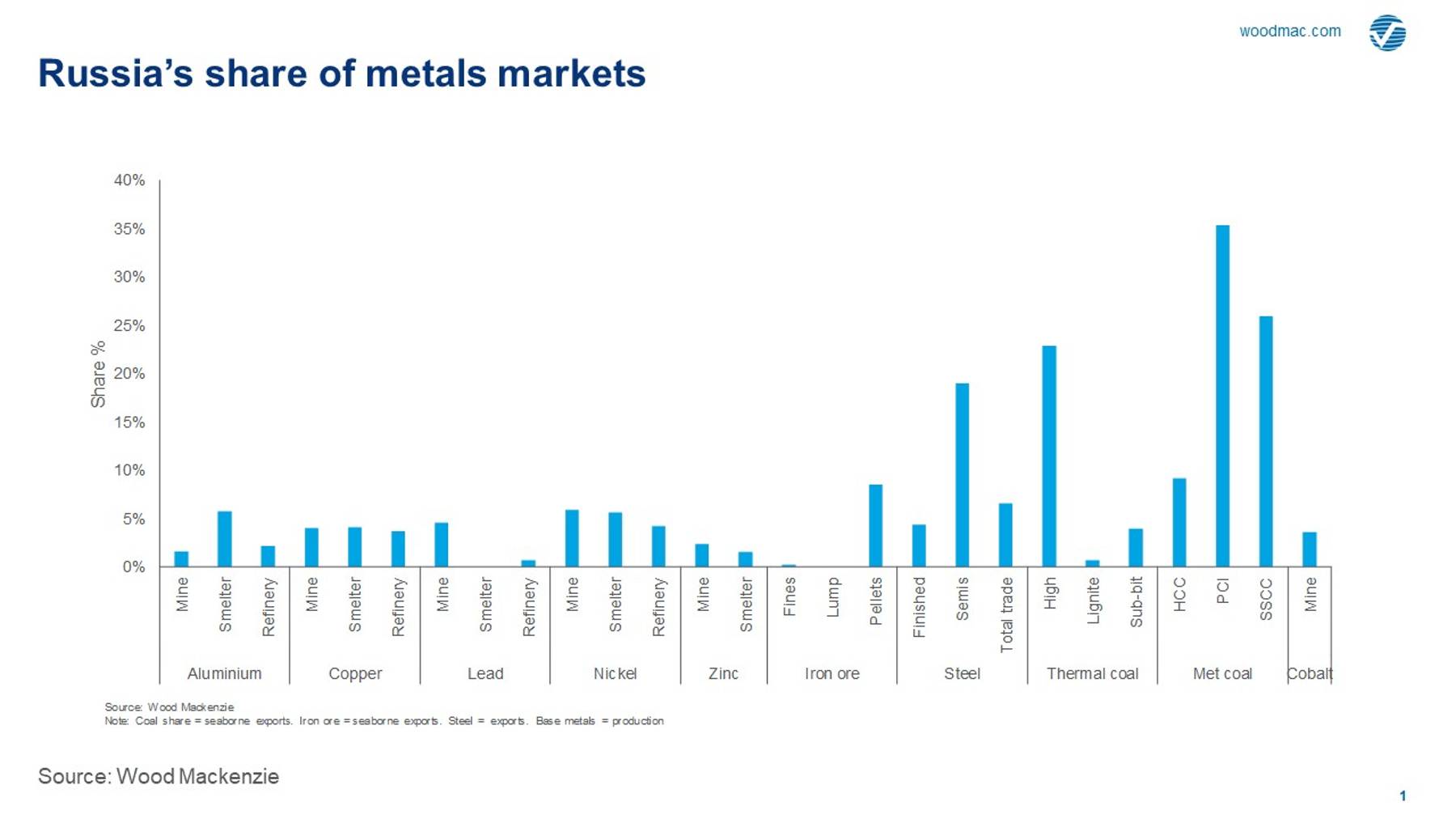

An analysis of Russia’s supply share of global metals and mining markets suggests bulk commodities would be most at risk. Russia supplies multiple commodity markets, but typically accounts for 5% or less of base metals and rare earths production, or trade. This share compares to more than 15% of the seaborne metallurgical and thermal coal trades. Importantly, Russia supplies Europe with almost all of its low sulphur-content PCI (Pulverised Coal Injection), and 60% of its high-energy thermal coal.

{kind=link}

A blanket EU ban on Russian coal imports – unlikely though it may be – would guarantee a large hole in EU coal supply. US and Colombian thermal coal suppliers would struggle to fill the gap, given the current constraints in those markets, and US coals can also bring with them issues around sodium, chlorine and sulphur contents. Meanwhile, replacement for low sulphur PCI would be near impossible in the short term. Australia – the only other major supplier of PCI coals – has seen spot PCI supplies dry up almost completely since mid-2021.

For base metals, Russian supply is not insignificant, but the sanctions are most likely to cause changes in regional rather than global pricing. Under most circumstances China is likely to be able to take some of the material redirected from Europe. For instance, 75% of Russia’s 300-400 kilo tonnes per annum (ktpa) lead concentrates goes to China, with much of the remainder ending up in Kazakhstan.

Another major threat as a result of escalating the conflict is the potential for higher power and energy prices, particularly affecting supply of energy-intensive products. The relationship between gas and power prices is already playing out in EU markets, and any further gas price rises would push electricity prices higher as well.

Griffin said: “Gas supply, and its impact on other energy markets, dominates fears about the impact of an armed conflict in Ukraine. All industrial activity in Europe will feel the effect of higher power prices. For metals and mined commodities markets, energy-intensive smelting is at most risk, particularly aluminium and zinc, although all base metals production and steel would feel a pinch.”

Power constitutes nearly 35% of the cost of making aluminium on average, and higher in some European smelters. An escalation in power prices across Europe has already led to significant aluminium production cuts. Wood Mackenzie estimates that an additional 400 ktpa capacity is at risk of shutting down if energy prices escalate further. Europe accounted for 15% of ex-China aluminium supply in 2021 and thus supply cuts could have a material effect on prices for refined metal. Zinc smelting is also very vulnerable to energy price rises. And at 2.2 million tonnes per annum (mtpa), Europe accounts for 16% of global refined zinc output.

Griffin said: “There are also direct risks to production facilities inside the potential conflict zone in Ukraine, especially in the border regions. The country has a long history of industrial activity and has some large production facilities across the metals and mining sector. But outside of the bulks sector, most production lies some distance from the border.”

Ukraine’s steel production represents a tiny proportion of global supply, and it is hard to see a prolonged impact on global steel prices. But exports of steel semis do register on a global scale. If Ukraine’s 4 mtpa of exports to Europe are affected, then some further upward pressure on steel prices is inevitable in that market.

Exports of Ukrainian coal have now all but disappeared, but they are still importing between 10 and 13 Mt of metallurgical coal each year, of which Russia and the US typically make up 65% and 25% respectively. Thermal coal imports remain at between 3 and 4 Mt, largely from Russia, the US and Kazakhstan.

Griffin said: “From a market perspective coal could see some impact as US, Polish or Australian suppliers attract additional demand from Ukraine steelmakers. But that assumes it is logistically possible to get coal to steel mills. Deliveries into Black Sea ports are already being disrupted and there’s no guarantee that imported coal could make its way further inland into eastern Ukraine. For other base metals and mined commodities production facilities in Ukraine are typically small.”

The ultimate impact on markets will depend upon the geographic spread of the conflict, and the breadth of retaliatory sanctions. Trade bans – if strictly implemented - will eventually see Russian products diverted to other markets.

Griffin said: “But as we have seen during other market interventions, the rebalancing can be messy and typically comes with a price impact that goes beyond the additional costs of obtaining alternative supply. There is little doubt that any conflict would add to the growing inefficiency of commodity supply that has been a feature of markets over recent years, due to resource nationalism, trade disputes, and pandemic disruption.”