Get in touch

-

Mark Thomtonmark.thomton@woodmac.com

+1 630 881 6885 -

Hla Myat Monhla.myatmon@woodmac.com

+65 8533 8860 -

Chris Bobachris.boba@woodmac.com

+44 7408 841129 -

Angélica Juárezangelica.juarez@woodmac.com

+5256 4171 1980

China leads global renewables race with record-breaking 230 GW installations in 2023

US$140 billion investment and mass scale in domestic market drives China’s advantage

2 minute read

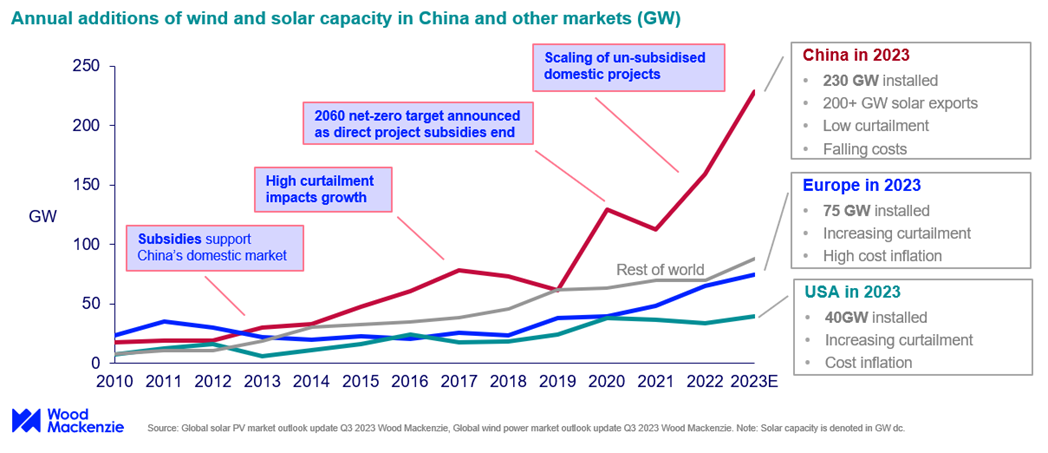

Currently on target to reach a record-breaking 230 gigawatts (GW) of wind and solar installations this year, China leads the global renewables market. This is more than double the number of US and Europe installations combined, according to latest report ‘How China became the global renewables leader’ by Wood Mackenzie.

Wind and solar project investment for China is expected to reach US$140 billion for 2023, according to the report’s findings.

Alex Whitworth, Vice President, Head of Asia Pacific Power and Renewables research at Wood Mackenzie, said: “China announced its 2060 carbon neutral target in 2020 and since then has been quietly re-organising the entire power sector to support rapid electrification and expansion of renewables. As we came out of COVID-19 lockdowns this year, it’s impressive to see how far ahead China really is. While some other markets are moderating renewables targets, China has pushed up its 2025 wind and solar outlook by 43% or 380 GW in just a couple of years.”

Direct subsidies give way to system-level government support

As costs of wind and solar fell in China, the country also withdrew preferential feed-in tariffs for renewables projects in 2022, saving the government hundreds of billions in subsidies.

China has budgeted US$455 billion in grid investments from 2021-2025, up 60% from the previous decade. This includes long-distance transmission lines over 1,000 km long which have unlocked more than 100 GW of renewables development in inland China.

China has become a leader in grid-connected energy storage, with capacity doubling from 2020 to hit 67 GW in 2023 and an outlook to expand to 300 GW by 2030.

Other government initiatives target grid flexibility. China has been criticised for a pipeline of over 200 GW coal plants under development, but new policies have also led to creation of a fleet of more than 100 GW of flexible plants which burn less coal and are designed to ramp up to backup intermittent renewables. China has also released new policies on the demand side such as higher peak pricing and setting targets for 50-80 GW of Demand Side Management (DSM) or “virtual power plants” by 2025.

The share of coal in power generation has been continuously falling, down 10 percentage points in the last five years to about 55% today. About 80% of the reduction was replaced by renewables and the rest mostly by nuclear power.”

Strong system integration and low costs give China the lead in wind and solar through the next decade

Growth in renewables has been helped by low solar and wind curtailment rates which hit levels of 2% and 4%, respectively, in 2022. This improves project economics significantly compared to curtailment of over 10% experienced before 2020.

Falling interest rates, low energy costs, intense price competition among domestic suppliers, and government support for Research & Development and manufacturing have all supported falling costs in China.

“China’s end-user power prices are less than half those in Europe or Australia and this supports a strong competitive edge in global trade. The China power market is now larger than that of Europe and the US combined, so if it can succeed in transitioning to a high share of intermittent renewables while maintaining stable prices, that would be an historic achievement,” concluded Whitworth.