Get in touch

-

Mark Thomtonmark.thomton@woodmac.com

+1 630 881 6885 -

Hla Myat Monhla.myatmon@woodmac.com

+65 8533 8860 -

Chris Bobachris.boba@woodmac.com

+44 7408 841129 -

Angélica Juárezangelica.juarez@woodmac.com

+5256 4171 1980

Energy transition represents a US$14 trillion uncertainty for upstream oil and gas

Even a rapidly transitioning world needs oil and gas supply for decades to come

1 minute read

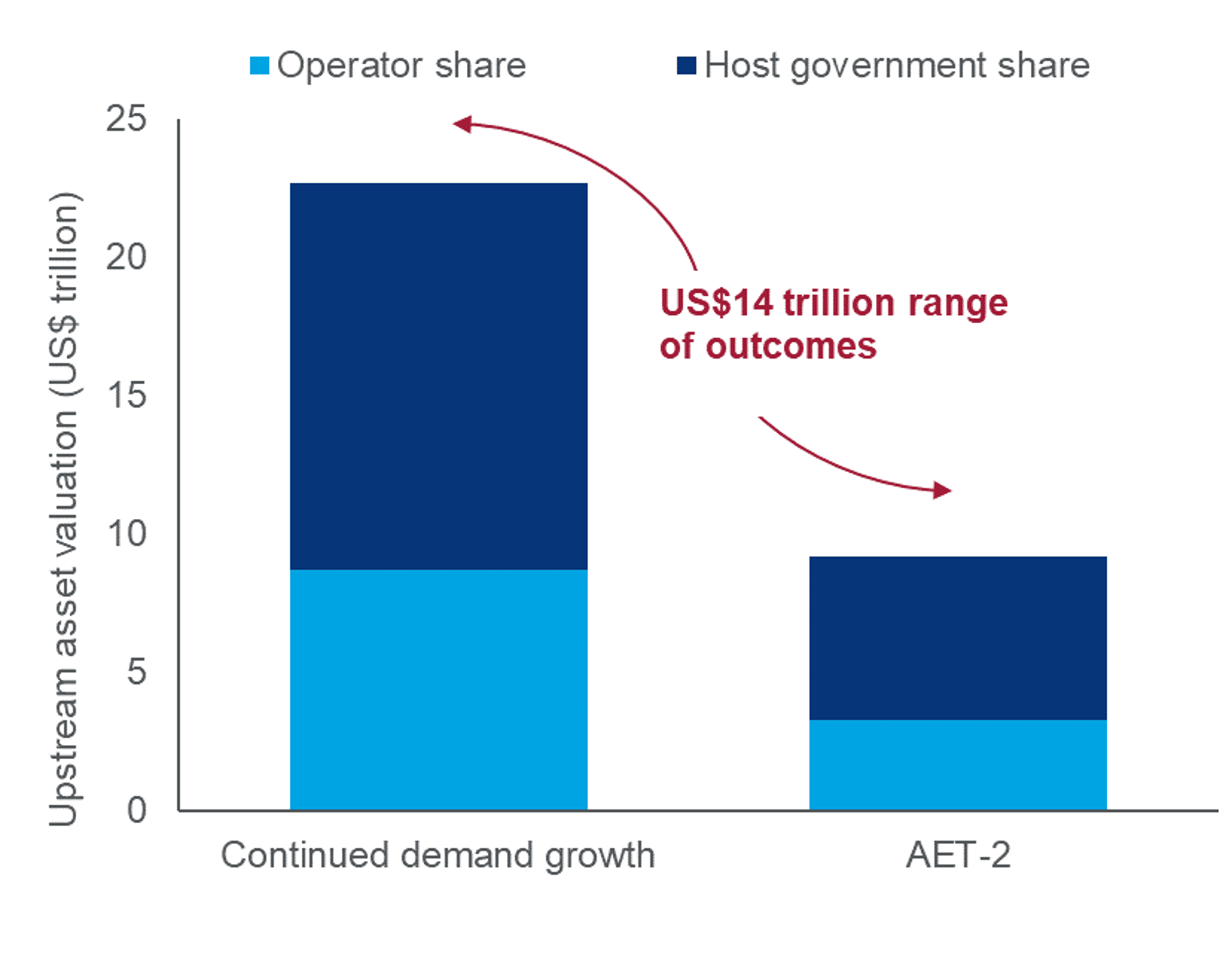

The energy transition represents US$14 trillion worth of uncertainty for upstream oil and gas, according to a new report by Wood Mackenzie.

Oil and gas is a risky business. Over the years, those risks have been tempered by a single tenet – that demand would continue to rise indefinitely. As the energy transition gathers momentum, that belief has all but evaporated.

Oil demand may continue to grow for another decade or more. On the other hand, if the world acts decisively to limit global warming to 2°C by 2050 – our AET-2 scenario – oil demand and prices would fall rapidly later this decade. Gas demand and price, however, would be more resilient.

While this range of outcomes has major implications for the oil and gas industry, in either scenario there is still a huge amount of upstream value on the table. Using its global Lens asset-by-asset modelling, Wood Mackenzie estimates the range of pre-tax future valuations for upstream is a staggering US$14 trillion – from US$9 trillion to US$23 trillion. On a post-tax basis, operators’ share of this economic rent ranges from US$3 trillion to US$9 trillion.

Wood Mackenzie vice president Fraser McKay said: “The industry now finds itself having to supply oil and gas to a world in which future demand – and price – are highly uncertain. The range of possible outcomes is dizzying. But the world will still need oil and gas supply for decades to come, and the scale of the industry will remain enormous.”

{kind=link}

Delivery and discipline are paramount in all aspects of the upstream value chain as the macro environment for oil and gas gets tougher. Performance against budgets and timelines has improved dramatically since the last downturn. The industry needs to remain relentless in its push to improve efficiency, drive down costs and deliver projects flawlessly. Oil and gas companies need to send a strong signal to stakeholders that they can be reliable stewards of capital.

Wood Mackenzie research director Angus Rodger said: “Only exceptional, low-cost projects will work in all demand scenarios. Inevitably, the cost of capital and the cost of doing business in oil and gas will increase.”

Oil and gas companies must improve their environment, social and governance (ESG) credentials. The bond of trust with stakeholders must improve. For the biggest players, new energies will play an increasing role, but this is a not an option for many industry participants. They will need to cut Scope 1 and 2 emissions to reduce their exposure to increasingly expensive debt.

Investment will shift to gas, ending oil’s long supremacy. “The industry will have to figure out the conundrum of weaker economics if the giant gas projects the world needs are to happen. The returns on developing a barrel of oil are currently higher, with oil-production and cash-flow profiles delivering more value upfront. Gas prices are lower than oil prices on an energy-equivalent basis; that relationship will have to invert as it does in our AET-2 scenario to make this happen,” said Rodger.

McKay added: “And business models must adapt to maximise value as the oil and gas sector matures. Consolidation to bolster margins will gather momentum. Specialists will carve out niches. Applying the right technology and retaining the right people will determine their success. Just a few more years of firm oil prices would strengthen balance sheets, making transition strategies easier to execute.”

Note: Wood Mackenzie’s Accelerated Energy Transition 2 (AET-2) scenario shows our view of a possible state of the world and of the energy industry that is consistent with limiting the rise in global temperatures since pre-industrial times to 2 degrees Celsius. There could be multitude of potential pathways for meeting that condition, and the AET-2 scenario represents our interpretation of the likeliest route, given the policy drivers and technological innovation required. We do not assign a probability to the likelihood of any scenario being realised.