Get Ed Crooks' Energy Pulse in your inbox every week

Middle East conflict spurs interest in American resources

Production in the Western Hemisphere will not replace all the lost supply from the Gulf, but can strengthen regional energy security

1 minute read

Ed Crooks

Vice Chair Americas and host of Energy Gang podcast

Ed Crooks

Vice Chair Americas and host of Energy Gang podcast

Ed examines the forces shaping the energy industry globally.

Latest articles by Ed

-

Opinion

Is the competitive power market model broken?

-

Opinion

Is fusion power here at last?

-

Opinion

Battery storage proves its value in moderating Texas power price volatility

-

Opinion

Can the LA Olympics in 2028 be a catalyst for clean energy?

-

Opinion

Strong El Niño event will have wide-ranging impacts on energy

-

Opinion

Why is it so hard to build big energy projects?

The situation in the Middle East conflict has remained broadly unchanged over the past week. The ceasefire in the Gulf has mostly held, but shipping traffic through the Strait of Hormuz has remained well below pre-war levels.

The US has continued its blockade of vessels moving to or from ports in Iran, stopping and boarding two tankers. Traffic to and from other countries in the Gulf has been infrequent, deterred by the threat of Iranian attacks.

While the disruption to supplies from the Gulf continues, signs of strain in the global energy system have been mounting.

Brent crude futures for June, which were briefly down to about US$86 a barrel ten days ago, had rebounded up to almost US$106 a barrel by last Friday evening. The average price of gasoline in the US is about US$4.10 a gallon, with diesel at US$5.46 a gallon.

The impacts of oil product shortages have been spreading. Lufthansa said it would cut 20,000 flights previously scheduled between now and October. Prices for latex products such as rubber gloves are soaring. In India, Diet Coke has disappeared from stores because of a shortage of aluminium cans.

Mike Wirth, chief executive of Chevron, warned in a CBS interview: “It's not just gas. It's LPG for cooking in in South Asia, it is jet fuel in Europe, a number of products are becoming very short in supply.”

As of Monday morning, there are no plans for more direct peace negotiations between US and Iranian officials. Interviewed on Fox News on Sunday, President Donald Trump indicated that talks would go ahead only if US conditions were met. “They cannot have a nuclear weapon. Otherwise there’s no reason to meet,” he said.

However the conflict is ultimately resolved, there are already signs that the supply shock it has caused is driving interest in oil and gas production elsewhere in the world.

In many cases, plans to increase production were already taking shape before the war began. But the outbreak of hostilities has created a new context for those plans, and is generating additional momentum behind efforts to bring them to fruition.

In Venezuela, for example, both the government and the industry have been moving swiftly since the capture of former President Nicolas Maduro in January.

Reforms to key legislation governing the oil and gas industry have been approved by the National Assembly. The reforms set new maximum rates for royalties and the Integrated Hydrocarbons Tax. PDVSA, the national oil company, lost its exclusive control of oil production and sales. Private companies are now allowed to have operational and commercial control of projects, and to have access to arbitration.

International oil companies with operations in Venezuela have been setting out their plans to boost production. Chevron has said it can increase output in the country by up to 50% within the next 18 to 24 months. Repsol is aiming for a 50% increase within 12 months, and a tripling over the next three years.

Chevron signed the first significant deals for international companies in Venezuela since the overthrow of President Maduro. It is increasing its stake in the Petroindependencia heavy oil joint venture with PDVSA in the Orinoco Belt, from 35.8% to 49%. It is also reshuffling a few other assets, relinquishing two gas blocks and stake in a small oil project, while taking on a new oil area to add to Petropiar, another Orinoco Belt heavy oil project.

Shell has also reportedly been in negotiations with Venezuela’s government to develop more offshore gas assets, in addition to the Dragon field, which it entered in 2023. Wael Sawan, Shell’s CEO, said last month that the company could take final investment decision (FID) on at least two projects in Venezuela before the end of this year, “if afforded the right fiscal and legal frameworks.”

The Trump administration has been encouraging investment in Venezuela by relaxing sanctions. The US Office of Foreign Asset Control (OFAC) issued general licenses creating a comprehensive framework for international companies to develop projects in Venezuela under US oversight. The latest general licence, GL50A, specifies six approved operators: Chevron, Repsol, Eni, Shell, BP and Maurel & Prom.

There have also been signs of rising interest in upstream investment elsewhere in the Western Hemisphere in recent weeks. In Alaska, record revenue was generated by a lease sale for the National Petroleum Reserve.

In the Gulf of America, Occidental Petroleum this month announced an oil discovery that will help extend the working life of its production facilities. And last month, BP received the approval it needed from US Bureau of Ocean Energy Management for the development plan for its US$5 billion Kaskida project.

In Mexico, President Claudia Sheinbaum said she supported increasing the country’s natural gas production by developing unconventional resources. The country is heavily dependent on imports from the US, which supply about 75% of its demand for gas. The government aims to launch early-stage unconventional development this year, targeting 3.2 billion cubic feet per day (bcf/d) from unconventional sources by 2035.

Meanwhile Guyana, the outstanding success story for offshore oil development in the Americas over the past decade, is accelerating efforts to ramp up production, Reuters reported.

None of these pieces of news are world-changing in their own right. Taken together, they point to the ways that energy security concerns may change the world of oil and gas in the aftermath of the Iran war.

The Wood Mackenzie view

The first point to make clear is that none of the developments in the Americas can materially offset the immediate loss of oil and gas supply caused by the closure of the Strait of Hormuz.

The US unconventionals industry has a relatively rapid reaction time. But even there, there will be a three to 12 month lag between changes in commodity prices and changes in output. Companies want to know that higher prices will be sustained for long enough to justify increased capital spending. For now the oil futures curve remains in steep backwardation, with benchmark US WTI crude for December delivery trading at about US$78 a barrel.

So far, there is no sign of any general upturn in activity in the US industry. There were 407 rigs drilling for oil in the US last week, according to Baker Hughes, exactly the same number as immediately before the war began at the end of February.

Venezuela has been able to achieve a modest increase in output as a result of the easing of US sanctions. Oil production was running at about 900,000 b/d in January, and was up to about 1.1 million b/d in March.

Other sources, including Alaska, the Gulf of America and unconventional resources outside the US, will take several years to bring on additional supply.

However, although the short-term impact of all this activity may be modest, the consequences could be significant in the longer term.

In Venezuela, upstream development could lead to additional LNG supply, if gas can be piped to Trinidad to supply the Atlantic LNG liquefaction plant there. Eni and Repsol have reportedly reached an agreement with the Venezuelan government to export gas from the Perla field, using a floating LNG facility. Gas could also be piped to Colombia, to ease its growing reliance on LNG imports.

There are still significant hurdles to be overcome to deliver material increases in Venezuela’s production. Oil infrastructure and reservoirs have been degraded, and in some cases will need extensive restoration. Political risk remains a factor, as shown by recent protests over pay and pensions.

But Adrian Lara, a Wood Mackenzie principal analyst for upstream in Latin America, says it is those strategic possibilities that are attracting interest from international companies.

“It is not all about the short term,” he says. “The international companies think about the potential and risks in Venezuela not just over the next few months. It’s a medium-term story.”

In Mexico, there are also challenges to resource development, but President Sheinbaum’s target for production growth, while ambitious, looks achievable. New research from Wood Mackenzie’s Robert Clarke and Joshua Dixon identifies Mexico as one of the six countries that is best placed for the development of unconventional resources outside the US, in what they are describing as “global shale 2.0”.

Put these various pieces together, Wood Mackenzie’s Lara says, and you can see a new picture of energy security for the Western Hemisphere starting to take shape. Countries will aim to produce more of the oil and gas they consume, or at least source it from friendly neighbours.

As the US experience this year has shown, meeting oil consumption from domestic production does not provide complete insulation from international shocks, because prices for crude and products are set in global markets. But it does help mitigate the economic impact.

For gas, the advantages of having domestic production are even greater. A comparison between North American and European prices makes the point very clearly. US benchmark Henry Hub is now about US$2.50 per million British thermal units (mmbtu), while European benchmark TTF is roughly US$15 / mmbtu.

The conflict in the Middle East is forcing a widespread reassessment of views on global security. A new focus on energy supplies that are regional and local, rather than global, could be one of the lasting impacts.

In brief

President Trump signed a series of executive memorandums related to the Defense Production Act (DPA), intended to increase US production of oil, gas, coal and grid equipment. The DPA, passed early in the Korean War in 1950, gives the government wide-ranging powers to make purchases, offer loans, and direct production by private companies to supply goods deemed necessary for national defence. President Trump argued in his memorandums that “our nation’s current inadequate and intermittent energy supply leaves us vulnerable to hostile foreign actors and poses an imminent and growing threat to the United States’ prosperity and national security.”

The move follows the president’s declaration on his first day in office in January 2025 that the US is in a national energy emergency. The memorandums are presented as orders to Chris Wright, the energy secretary, directing him to take steps including making purchases and financial commitments to expedite energy projects.

A key mechanism for implementing those orders is expected to be by using the Department of Energy’s Office of Energy Dominance Financing (EDF), previously known as the Loan Programs Office. Under the budget legislation passed last year, informally known as the “one big beautiful bill”, the EDF is authorised to back loans up to a total value of US$250 billion by the end of September 2028. The loan guarantees could cut the cost of financing for companies in the sectors covered by President Trump’s orders.

The governor of Maine, Janet Mills, has vetoed a bill backed by the state’s legislature that would have imposed a moratorium on new data centres. In a letter announcing her decision, Governor Mills said that while she acknowledged the potential downsides of data centre development, there was at least one project in the state with strong local support from its host community. The town of Jay in western Maine has attracted a US$550 million data centre project that is expected to create more than 800 construction jobs and 100 permanent jobs, and to contribute substantial property tax revenue.

If approved, the bill would have made Maine the first state in the US to ban data centre development. Concern about the impact of data centres on electricity bills, as well as about the wider impacts of AI on society, have risen high on the political agenda in many parts of the US.

Laura Swett, the chair of the Federal Energy Regulatory Commission (FERC), has said she is prepared to push up to “the absolute edge of precedent” in setting rules to manage the strains on the US energy system. In a speech to the Energy Bar Association, Swett said: “If I do something risky, it will be very deliberate… It will be grounded in the law. It will be grounded in my understanding of economic commercial realities from representing clients and with a very calculated determination that we will win.”

Her comments follow a call from energy secretary Chris Wright for FERC to take on new responsibilities for connecting large loads such as data centres to the electricity transmission grid.

Other views

Southeast Asia faces its deepwater gas 2.0 moment – Angus Rodger and Munish Kumar

CESCO 2026: key takeaways – Emily Brugge and Charles Cooper

There’s no such thing as the petrodollar – Brendan Greeley

The Iran war comes for ‘the king of chemicals’ – Christina Lu

Quote of the week

“The vase is broken, the damage is done – it will be very difficult to put the pieces back together. This will have permanent consequences for the global energy markets for years to come.”

Fatih Birol, executive director of the International Energy Agency, argued that the conflict in the Middle East would give a significant boost to renewables and nuclear power, and drive “a further shift towards a more electrified future”, cutting into world oil demand.

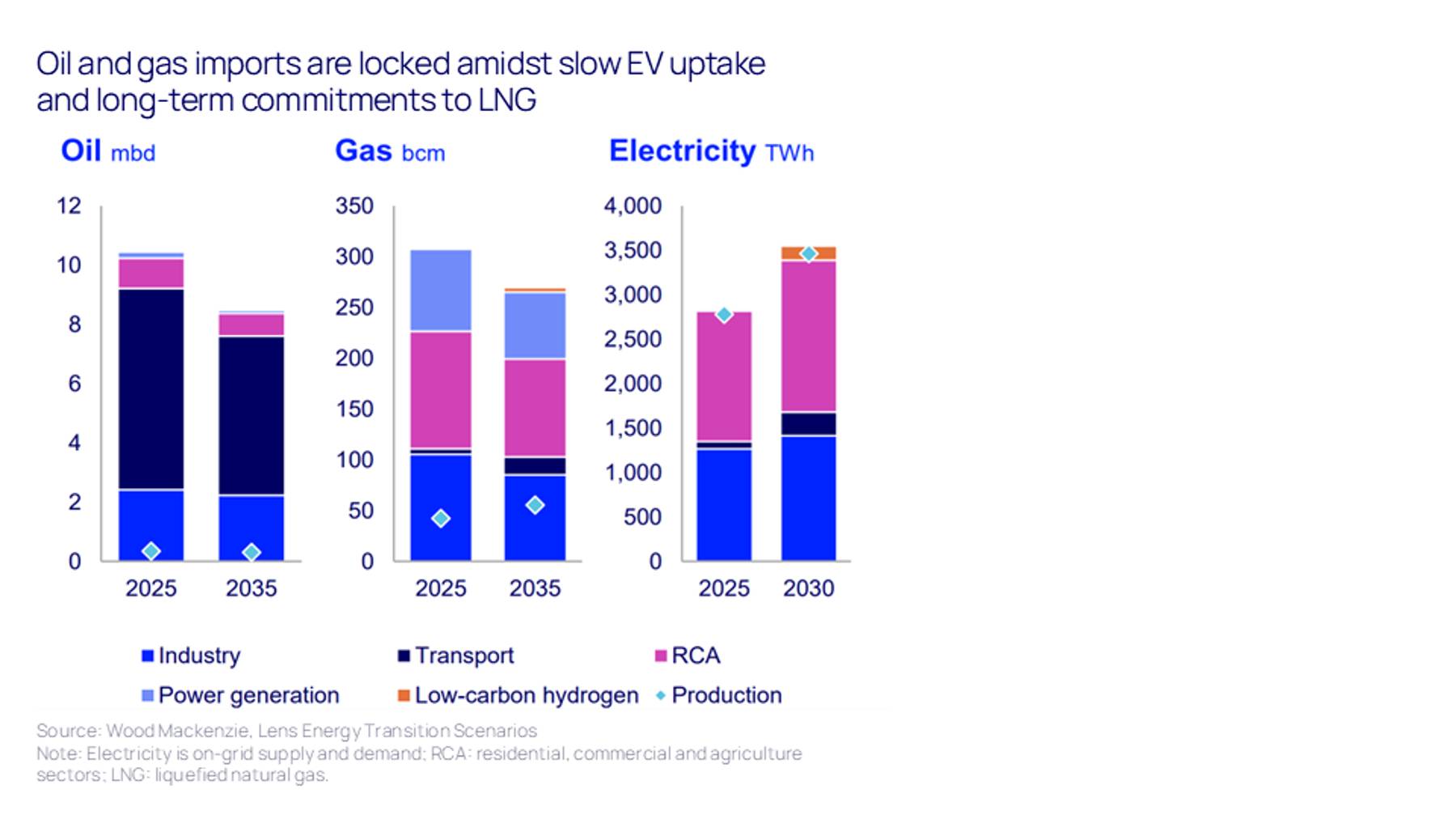

Chart of the week

This comes from a recent report on the outlook for the EU’s energy system, by Wood Mackenzie analysts Lindsey Entwistle and Zoé Sulmont. The bars show historic and forecast EU consumption of oil, gas and electricity, and the blue diamonds show the region’s production of those commodities.

The conflict in the Middle East has highlighted the vulnerabilities created by reliance on imported energy. And despite efforts to cut the EU’s consumption of fossil fuels, the region is expected to remain heavily dependent on imported oil and gas, out to the mid 2030s and beyond. Download the summary report for more detail on the key issues in European energy.

{kind=link}

Get The Inside Track

Ed Crooks’ Energy Pulse is featured in our weekly newsletter, the Inside Track, alongside more news and views from our global energy and natural resources experts. Sign up today via the form at the top of the page to ensure you don’t miss a thing.