Discuss your challenges with our solutions experts

Middle East tensions: a litmus test for carbon market resilience, not transition momentum

Carbon, CCUS and the conflict?

1 minute read

Hetal Gandhi

Lead, Global forecasting and Asia Pacific Research, Carbon Mitigations

Hetal Gandhi

Lead, Global forecasting and Asia Pacific Research, Carbon Mitigations

Hetal leads CCUS for APAC with a growing team of analysts to help clients in decision-making and business planning.

Latest articles by Hetal

-

Opinion

Middle East tensions: a litmus test for carbon market resilience, not transition momentum

-

Opinion

India’s energy roadmap: 5 key themes for IEW 2026

-

Opinion

Is CCUS viable in power generation?

-

Opinion

The forces shaping the future of carbon management

-

Opinion

The future of CCUS: 2025–2050

-

Opinion

CCUS: the US$196 billion investment opportunity

Stephen Vogado

Senior Research Analyst, Carbon Policy

Stephen Vogado

Senior Research Analyst, Carbon Policy

Stephen focuses on carbon policy, taking a data-driven approach to help clients navigate the energy transition.

Latest articles by Stephen

-

Opinion

Four carbon policy developments set to impact E&P decision-making in H2

-

Featured

Carbon mitigation: 2026 half-time report

-

Opinion

4 carbon policy developments that impact E&P decision-making

-

Opinion

Middle East tensions: a litmus test for carbon market resilience, not transition momentum

-

Featured

Carbon management 2026 outlook

-

Opinion

Carbon policy: 5 things to look for in 2026

Stefania Albarosa

Research Analyst, Carbon Pricing

Stefania Albarosa

Research Analyst, Carbon Pricing

Latest articles by Stefania

-

Opinion

Middle East tensions: a litmus test for carbon market resilience, not transition momentum

-

Opinion

Carbon markets Q2 update: policy shifts and market evolution

Peter Albin

Senior Research Analyst, Carbon Markets

Peter Albin

Senior Research Analyst, Carbon Markets

Peter is part of the Carbon Research team which delivers intelligence, data and thought leadership pieces.

Latest articles by Peter

-

Opinion

Four carbon policy developments set to impact E&P decision-making in H2

-

Opinion

Middle East tensions: a litmus test for carbon market resilience, not transition momentum

-

Opinion

A conversation with Decarb Connect: 3 key takeaways

-

Featured

Carbon management 2026 outlook

-

Opinion

Carbon markets: 5 things to look for in 2026

-

Opinion

Forecasting carbon offset use to 2050: what you need to know

Jack Mageau

Senior Research Analyst, CCUS

Jack Mageau

Senior Research Analyst, CCUS

Jack provides strategic insight on the global CCUS landscape to project developers, governments and investors

Latest articles by Jack

-

Opinion

NZIA feasibility report: Is the NZIA achievable from a full value-chain perspective?

-

Opinion

Middle East tensions: a litmus test for carbon market resilience, not transition momentum

-

Opinion

Policy vs. Practicality: assessing the feasibility of meeting NZIA Article 23

-

Opinion

Enhanced oil recovery with captured CO2: insights on CCS-EOR

-

Featured

CCUS: 5 things to look for in 2024

Michelle Uriarte-Ruiz

Senior Research Analyst, Carbon Offsets Valuations

Michelle Uriarte-Ruiz

Senior Research Analyst, Carbon Offsets Valuations

Michelle is part of the carbon team, providing clients with insights and analysis of carbon offset projects.

Latest articles by Michelle

-

Opinion

Four carbon policy developments set to impact E&P decision-making in H2

-

Opinion

4 carbon policy developments that impact E&P decision-making

-

Opinion

What E&P firms need to know about the future of carbon offsets

-

Opinion

Middle East tensions: a litmus test for carbon market resilience, not transition momentum

-

Opinion

The forces shaping the future of carbon management

-

Opinion

Forecasting carbon offset use to 2050: what you need to know

Escalating conflict in the Middle East has delivered a sharp shock to global energy markets, driving volatility in oil and gas prices and raising concerns over supply security. As governments and companies respond, attention has quickly turned to the implications for carbon policy, carbon pricing, carbon offset markets and carbon capture, utilisation and storage (CCUS) - the key pillars of carbon markets.

In the near term, policymakers and corporates are prioritising inflation control, economic stability and operational resilience. This has created short‑term headwinds for some decarbonisation activities. Yet while the conflict introduces delay and uncertainty, it does not alter the long‑term imperative to reduce emissions. Across carbon markets and low‑carbon technologies, continuity – rather than reversal – remains the most likely outcome.

We assess what we know, what we expect and what lies ahead across four critical areas.

Carbon policies: at a crossroads

What we know

Geopolitical shocks often push short‑term economic protection ahead of long‑term climate ambition. Governments facing higher fossil‑fuel prices are considering targeted relief measures, including temporary subsidies, gas price caps and extended coal‑fired generation. Financing these interventions risks crowding out funding for climate incentives and decarbonisation programmes, particularly in economies most exposed to imported energy.

What we expect

Climate change does not pause during conflict. Once the immediate economic shock has been absorbed, policymakers will need to return to the structural challenge of transitioning away from unabated fossil fuels. The conflict reinforces a lesson seen repeatedly during energy crises: decarbonisation and energy security are increasingly aligned. Countries that expand domestic renewables, electrification and efficiency reduce exposure to geopolitical risk.

Europe’s response to Russia’s invasion of Ukraine showed how supply disruption can accelerate policy action. Similar dynamics are likely to emerge in Asia and the Middle East as energy security concerns intensify.

What lies ahead

Policy uncertainty remains a key challenge for corporates. While integrating decarbonisation into operations can enhance long‑term resilience, wavering political signals undermine first‑mover confidence. The balance between near‑term relief and credible long‑term transition policy will define investment momentum.

Carbon prices: stuck in the middle

What we know

Compliance carbon markets are sensitive to energy prices, particularly the EU Emissions Trading System (ETS). Prior to the conflict, the EU ETS was already fragile, weighed down by stretched speculative positions and political debate. As market sentiment shifted, prices fell sharply before stabilising at lower levels.

What we expect

Higher gas prices could initially support EU allowance prices through fuel switching into coal. However, sustained high prices risk demand destruction, reducing industrial output and emissions – and ultimately weakening allowance demand. This is why EU gas and carbon markets have correlated negatively since the conflict broke out. Amid concerns about forecasted high carbon prices, a struggling industry and increasing gas prices, proposals such as price caps or intervention have resurfaced, but these remain politically unsupported.

The most important drivers will instead be forthcoming regulatory decisions, including benchmark updates, reforms to the Market Stability Reserve and the 2026–27 ETS review. These will shape supply, demand and market confidence over the longer term.

What lies ahead

Even where short‑term adjustments are made, policymakers are unlikely to compromise the overall decarbonisation trajectory. Structural tightening of the EU ETS remains intact and will continue to define long‑term price dynamics, with implications for linked mechanisms such as the carbon border adjustment mechanism.

Carbon offsets: too soon to conclude

What we know

The Middle East contributes less than 1% of global carbon offset supply, limiting the conflict’s direct impact. Recent softness in demand appears to be driven more by broader market conditions than geopolitical disruption.

What we expect

Near‑term demand could soften among exposed sectors such as aviation, energy and financials. For aviation, profitability pressures and competing priorities could delay offset purchases under the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA). However, since compliance timelines extend to 2028, procurement deferral is likely, rather than structural demand loss.

What lies ahead

Long‑term offset market fundamentals remain largely unchanged. Political risk could increase the risk of CORSIA failing politically, but this wouldn’t necessarily lower airlines’ carbon costs. For example, international aviation’s inclusion in the EU ETS is one likely direct result, which would almost certainly result in a higher cost burden for impacted airlines.

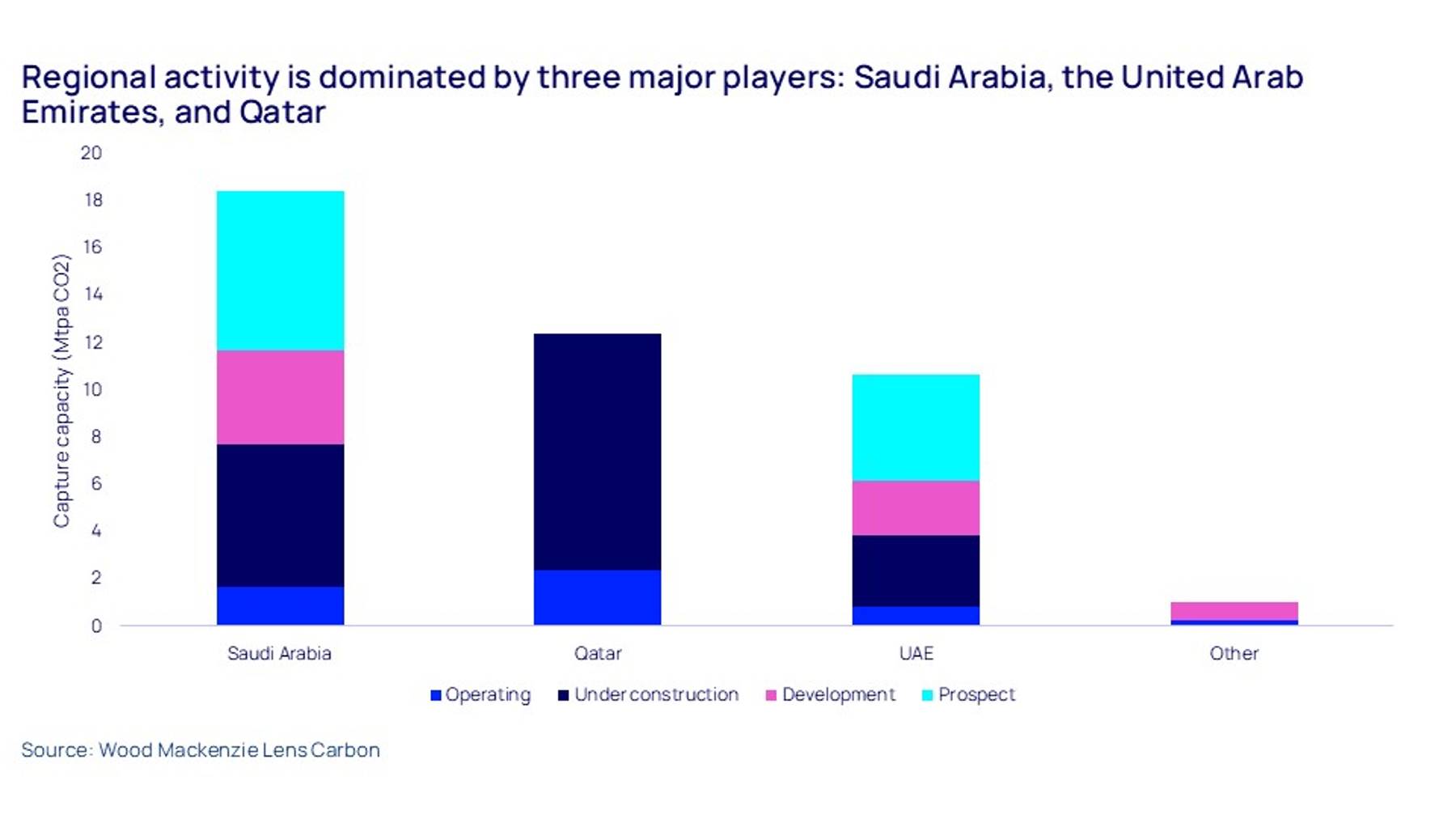

CCUS: another hurdle to cross

What we know

Middle East CCUS infrastructure has suffered direct disruption, with missile strikes targeting major gas facilities in Qatar and the UAE leading to operational suspensions and construction delays. Ras Laffan, the world’s largest post-FID CCS facility hub, is particularly exposed.

What we expect

Delays to operations and construction will be the most immediate impact, affecting a portion of the region’s 38 Mtpa of capacity currently under construction. However, in the long term, national oil companies with strong balance sheets and long-term investment horizons will limit the impact on our global outlook.

{kind=link}

What lies ahead

The situation is fluid, and significant downside risks remain. Higher capital and energy costs, potential capital reallocation toward defence and a possible loss of investor confidence could weigh on investment. Even so, Middle East CCUS strategies have proven resilient through past oil price shocks, pandemics and regional instability. The region also benefits from deep-pocketed national oil companies with long-term investment horizons.

Despite the conflict, Wood Mackenzie expects the Gulf region to remain a major player in the global CCUS landscape, with capture capacity surpassing 200 Mtpa by 2050. However, near-term impacts are likely, as direct disruptions may lead to operational suspensions and construction delays. As a result, we have revised our base-case 2035 capture capacity forecast for the region downward by 20%.

What this means

The Middle East conflict is reshaping short‑term energy and carbon market dynamics, but it does not change the long‑term direction of travel. As with previous crises, energy security concerns are likely to reinforce the strategic rationale for decarbonisation rather than undermine it.

For deeper analysis of the evolving geopolitical situation and its implications for oil, gas and energy markets, explore our full coverage at Iran tensions: oil and energy market implications.