Get Ed Crooks' Energy Pulse in your inbox every week

What carbon capture needs to meet climate goals

Wood Mackenzie's CCUS conference this week found positive trends, but the industry needs more progress in policy, technology and consumer preferences

10 minute read

Ed Crooks

Vice Chair Americas and host of Energy Gang podcast

Ed Crooks

Vice Chair Americas and host of Energy Gang podcast

Ed examines the forces shaping the energy industry globally.

Latest articles by Ed

-

Opinion

Is the competitive power market model broken?

-

Opinion

Is fusion power here at last?

-

Opinion

Battery storage proves its value in moderating Texas power price volatility

-

Opinion

Can the LA Olympics in 2028 be a catalyst for clean energy?

-

Opinion

Strong El Niño event will have wide-ranging impacts on energy

-

Opinion

Why is it so hard to build big energy projects?

Environmental groups often complain that the purpose of the carbon capture, use and storage (CCUS) industry is to make it possible to continue to use fossil fuels while meeting climate goals. “A buildout of CCS projects threatens to extend the life of fossil fuels,” the group Earthjustice argued last year.

Viewed in a more positive light, it is a promise, not a threat. Oil, gas and coal have great advantages as energy sources, and are hard to replace for many uses. The resilience of demand for fossil fuels means that the only way even to come close to meeting the climate goals of the Paris Agreement may be by using CCUS at scale.

Wood Mackenzie’s Net Zero scenario, showing an emissions pathway consistent with limiting global warming to 1.5 °C, includes a ramp up of global carbon capture capacity from under 50 million tons per year operational today to about 7 billion tons per year by 2050. That level is equivalent to about a fifth of current global energy-related carbon dioxide emissions.

That crucial role for CCUS means it has received widespread support both in the oil and gas industry and in the Biden administration. Wood Mackenzie held its annual CCUS conference in Houston this week, and there was discussion of several positive recent developments in the industry.

On the policy side, the US Department of Energy a couple of weeks ago announced a plan to offer up to US$1.3 billion in grants for pilot and demonstration projects for “transformative” carbon capture technologies. The department said the grants were intended to strengthen commercial businesses’ confidence in adopting CCUS technologies, open up new possibilities for electricity generators and industrial emitters, and help reduce costs. The department is holding a webinar on 21 October to provide more details.

Meanwhile ExxonMobil, which has to date captured more carbon dioxide than any other company, has been making moves to expand its storage capacity. The company announced on Thursday that it had agreed the largest offshore carbon dioxide storage lease in the US, securing access to a 271,000-acre site in the Gulf of Mexico off the coast of Texas. Revenues from the lease will go to the state’s school fund.

ExxonMobil said the Gulf had “vast potential” for helping the US to reach net zero emissions. It already has a dominant position in onshore carbon dioxide storage and pipeline infrastructure in the US, mostly acquired in the acquisition of Denbury in 2023.

Another important milestone for the CCUS industry in the US was passed last month, with the first ever tax equity financing deal in the sector. Harvestone Low Carbon Partners, which owns ethanol biorefineries in North Dakota and Indiana, has closed a US$205 million tax equity financing deal with Bank of America for a carbon capture and storage project at its Blue Flint plant.

Tax equity deals, which allow projects with little or no tax liability to receive the benefit of federal credits, are a familiar financing structure in the wind and solar industries, but until now had been unknown in CCUS. The precedent set by Harvestone may help other projects find similar deals to support their development.

The significance of the deal was discussed on a recent webinar with Peter Findlay, Wood Mackenzie’s director of CCUS analytics, and industry leaders including Nick Knapp, a partner and senior managing director at CRC-IB, which advised Harvestone on the financing.

Wood Mackenzie view

Even though there is quite a bit of positive news around for the CCUS sector, Wood Mackenzie analysts have been striking a note of caution over hopes that the industry can grow at the pace needed to achieve the Paris climate goals. In fact, Wood Mackenzie’s Findlay says most of the CCUS projects that have been announced are potentially at risk.

The tax equity deal for the Harvestone Blue Flint project is undoubtedly an important step for CCUS financing. But that project is particularly well-placed to succeed, ticking just about every box an investor would want to see ticked.

Ethanol plants create a very pure stream of carbon dioxide, meaning that capture costs are relatively low. The plant is very close to the storage site, meaning that it needs only a very short pipeline connection. And the ethanol produced at the facility should be eligible for other incentives to provide additional revenue streams, including the 45Z federal tax credits for clean fuels.

Not every proposed CCUS project benefits from such a favourable alignment of circumstances. Profitable projects are absolutely possible in today’s markets with today’s policy frameworks. But getting to billions of tons per year of operational CCUS capacity requires progress on a number of fronts.

First, there have to be stable government-backed mechanisms that reward avoided emissions. That could be directly through carbon pricing, or indirectly through tax credits such as the US 45Q, or other incentives. Stability is important. The value of the US 45Q credit is quite generous by international standards. But it only lasts for 12 years, creating challenges for projects that could remain in operation for many decades.

It is possible that a future Congress will extend the 45Q, but it is not certain. It is also possible that a future Congress could scrap it. That seems unlikely: oil companies have been urging former President Donald Trump to retain it if he is re-elected. But in the context of what will be acute pressure on the public finances, whoever is in the White House, all tax credits will be under pressure, and uncertainty is a deterrent to investment.

Second, customers – both businesses and retail consumers – need to be willing to pay more for products with low associated emissions. Companies that are using CCUS hope to be able to sell their products at premium prices. A steel-maker, for example, could sell low-emissions steel to a car manufacturer to help it meet its own targets for decarbonisation in the value chain. And car manufacturers could promote their vehicles to customers as “green” products.

The problem is that so far it has generally been difficult to persuade consumers to pay much of a premium for low-emissions products with low associated emissions. To strengthen the case for CCUS, consumers’ preferences will have to shift so that they are reliably willing to pay extra for products made with lower emissions in the supply chain.

Third, governments and regulators need to do whatever they can to expedite the process of securing environmental approvals and community support for CCUS investments. Some concerns are inevitable, given that policymakers and businesses are trying to create an entirely new industry essentially from scratch in just a few years. But several speakers at the Wood Mackenzie conference suggested that the US federal government was at times putting a brake on projects, whether because of insistence on protracted assessments of community impacts, or a simple lack of capacity for processing environmental approvals.

Finally, the CCUS industry needs to help itself by bringing down costs, particularly for carbon dioxide capture and transport. Wood Mackenzie estimates that CCUS costs will fall 50% in real terms by 2050. The more those cost reductions can be accelerated, the more projects will be commercially viable.

Some of these required changes do not look imminent. At our conference, two industry leaders suggested a US carbon price of around US$150 a ton, in today’s money, in 2040 would be enough to support a large-scale CCUS industry. There is no reason to think that such a price could be introduced for the foreseeable future in the US, and the position in 15 years’ time may not look very different.

However, mounting costs from impacts linked to climate change could shift public opinion enough to make it possible. If and when that happens, the companies that have been building knowhow, capabilities and assets in the meantime will be in a leading position to benefit.

To dig deeper on the issues covered in the conference, take a look at this recent post: Can CCUS momentum overcome headwinds to the industry?

In brief

Oil prices have stabilised somewhat this week after leaping higher at the beginning of the month as a result of the escalation in the conflict in the Middle East. Gulf states have urged the US to stop Israel from attacking Iranian oil facilities, because of concerns that their own installations could be targeted in retaliation, Reuters reported. President Joe Biden reiterated US calls for Israel not to strike Iran’s oil and nuclear infrastructure, in a call with Israel’s prime minister Benjamin Netanyahu, according to a report on Israeli television.

Meanwhile, Iran’s foreign minister Abbas Araghchi visited Riyadh this week and met Prince Mohammed bin Salman, the Saudi Crown Prince and prime minister. Brent crude was trading at about US$78 a barrel on Friday morning, close to its level a week ago.

At least 14 people were killed and more than three million customers lost power after Hurricane Milton hit the coast of Florida. The storm came just two weeks after the devastating impact of Hurricane Helene, which is now known to have killed more than 230 people. The two massively destructive storms came after what had been an unusually quiet hurricane season up until the last week of September.

Form Energy, the long-duration battery storage company, has raised US$405 million in a new financing round, in a sign of confidence in its innovative technology. Form’s iron-air batteries are optimised to store energy for 100 hours.

Tesla has unveiled a new proposal for an autonomous electric vehicle taxi, to be called either a “Cybercab” or a “Robotaxi”. The company aims to sell the vehicle for US$30,000, and to have it on the road within two years.

Other views

The complexity of capital allocation for oil and gas companies – Simon Flowers and others

Chevron moves closer to Canadian divestment target with $6.5B asset sale to CNRL

Algeria’s gas market outlook: 5 key takeaways – Lucy Cullen and others

The new economics of industrial policy - Réka Juhász, Nathan Lane and Dani Rodrik (Relevant to some of the debates around the US Inflation Reduction Act)

Rio Tinto makes a multibillion dollar bet against China – Javier Blas

How Russia’s ‘shadow fleet’ gets its ships – Tom Wilson

Carbon abatement costs of green hydrogen across end-use sectors – Roxana Shafiee and Daniel Schrag

Quote of the week

“I will cut the price of ENERGY and ELECTRICITY in HALF within 12 months. We will seriously expedite our environmental approvals, and quickly double our electricity capacity. This will DRIVE DOWN INFLATION, and make AMERICA and MICHIGAN the best place on earth to build a factory.”

One the campaign trail in Detroit, Michigan, former President Donald Trump reiterated his pledge to slash the cost of energy for US consumers if he is re-elected.

Wood Mackenzie analysts have argued that while a Trump administration could make changes to regulations and lease sales that would boost US oil and gas production over time, it is highly unlikely to have enough of an impact to halve energy prices within 12 months as former President Trump has suggested.

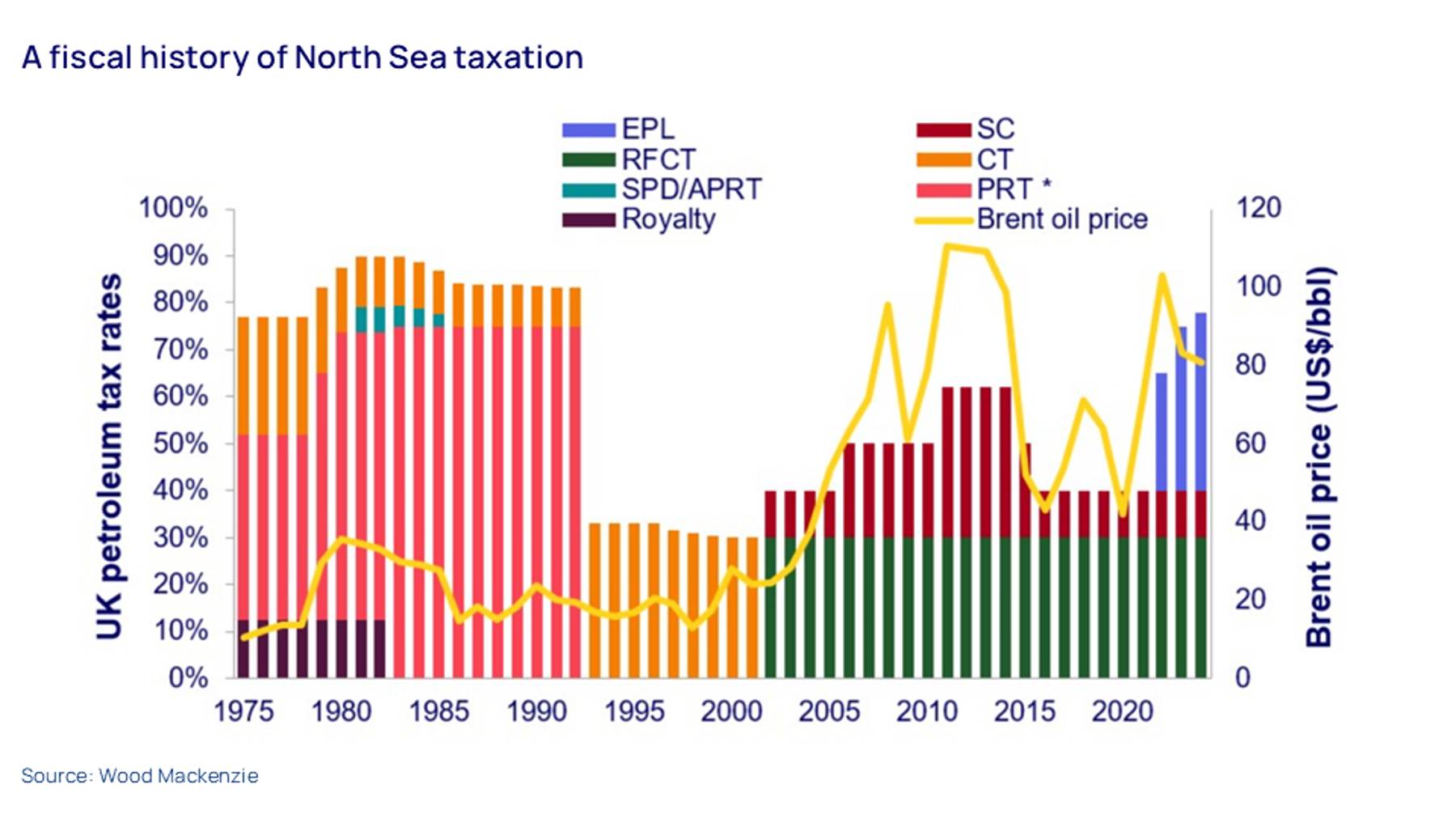

Chart of the week

This gives an at-a-glance overview of UK petroleum taxation since 1975. It comes from a recent post by Graham Kellas, Wood Mackenzie’s senior vice president for global fiscal research, warning that the UK North Sea’s future as an oil and gas producing region “hangs in the balance”. You can see that the total effective rate of tax, including the Energy Profits Levy that began in 2022, has risen to its highest since the early 1990s. in a new report, Wood Mackenzie’s Kellas says recent and proposed modifications to the Energy Profits Levy – currently set to end in 2030 – have created “unparalleled sector uncertainty and consternation.”

Kellas adds: “North Sea oil and gas operators are trying to make long-term financial decisions beyond 2030, but the current fiscal regime does not allow for such clarity. Price responsiveness, predictability, fairness, simplicity and transparency must all be considered to ensure the correct outcome is reached at what is a crucial juncture for the sector.”

{kind=link}

Get The Inside Track

Ed Crooks’ Energy Pulse is featured in our weekly newsletter, alongside more news and views from our global energy and natural resources experts. Sign up today via the form at the top of the page to ensure you don’t miss a thing.