Discuss your challenges with our solutions experts

Is there more upside for oil prices in 2023?

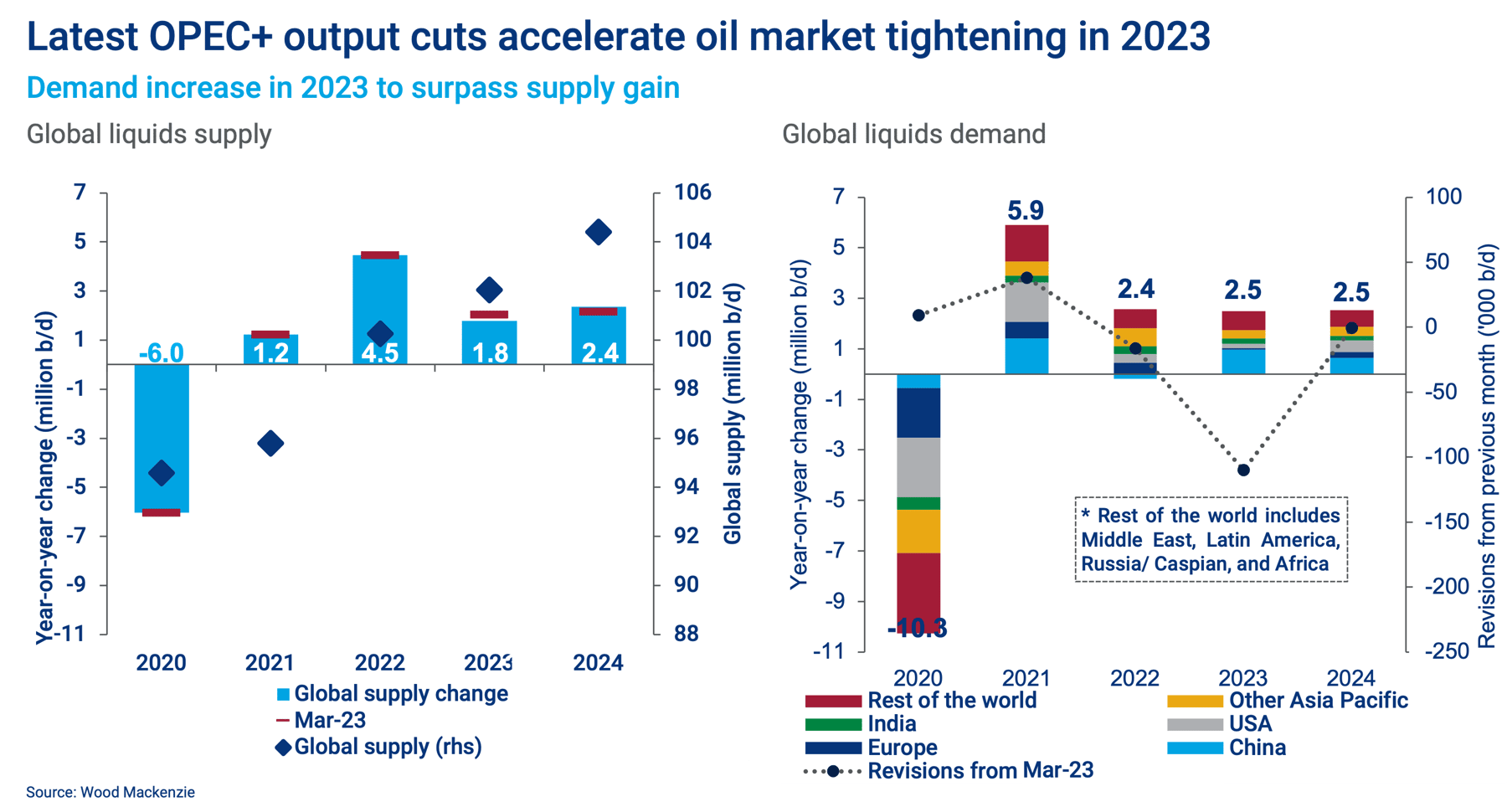

OPEC+ output cuts hasten market tightening

3 minute read

Simon Flowers

Chairman, Chief Analyst

Simon Flowers

Chairman, Chief Analyst

Simon is our Chief Analyst; he provides thought leadership on the trends and innovations shaping the energy industry.

Latest articles by Simon

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

Oil prices have had a volatile start to the year. Hardly surprising with a slowing global economy, high inflation, a banking crisis and OPEC+ slashing production targets for the second time in six months. Ann-Louise Hittle, Head of Macro Oils, predicted prices would strengthen this year and it’s still her firmly held view. I asked her why.

Is the economy playing out as expected?

What has been unfolding since late 2022 is supportive for the oil market. The early part of the year was always going to be tough for the global economy with interest rates at multi-year highs and inflation rampant, albeit starting to cool in key economies. We still expect global GDP growth to ease from 3.0% last year to 2.2% in 2023. So far, the economic news in Europe and the US has been a little better than expected, the authorities managed the mini-banking crisis and Asia has avoided the worst of the slowdown. Meanwhile, China’s economic bounce back in 2023 from lockdown seems on course.

How much will oil demand grow in 2023?

Our Macro Oils Service is forecasting another year of robust growth as global demand continues to recover from the deep trough of Covid. Our forecast of a nearly 2.5 million b/d gain in 2023 is unchanged from early in the year and a tad higher than last year’s 2.2 million b/d. Non-OECD countries provide almost 90% of this year’s growth, with China alone accounting for nearly 1 million b/d. As China’s economic recovery gathers pace, we expect the recovery from zero-Covid lockdown to lead to strong increases in oil demand through the rest of the year from gains in personal mobility, air travel and new petrochemicals capacity.

Will liquids growth keep up with demand?

Not quite. We expect global liquids supply to increase by 1.8 million b/d in 2023 after taking into account the latest minimal output cuts by OPEC+. Of the total, non-OPEC production rises by a healthy 1.6 million b/d, marginally down on last year, but reflecting gains from the US – with the Lower 48 and Permian, in particular, the growth engine – along with producers such as Canada, Brazil and Kazakhstan.

So why did OPEC+ decide to cut production earlier this month?

To boost prices after a steep fall in mid-March and to pre-empt concerns about short-term demand risk. Oil prices had weakened after the collapse of the Silicon Valley Bank in the US and the enforced takeover of Credit Suisse by UBS raised the spectre of another banking crisis with potential negative implications for the global economy. Brent fell by about US$10/bbl from the range it had been holding of roughly US$80-$85/bbl. OPEC+ has repeatedly signalled its willingness to step in and manage the market’s recovery since the depths of the Covid downturn in 2020. It saw an opportunity to act swiftly, announcing on 2 April a surprise 1.66 million b/d cut in its production target. The effect was immediate, with Brent regaining the ground lost and trading in the mid-US$80s per barrel since.

Will prices rise higher still?

Yes, provided a significant recession does not develop. Our view has been that rising demand would bring the market into balance later in the year and the additional OPEC+ cuts bring forward the tightening we have been anticipating for the third quarter. The Macro Oils service forecasts Brent to rise average US$94/bbl in Q3 and hold that level through Q4. There may even be a need for OPEC+ to raise output again if, for example, Russia’s oil production falls further than expected.

What are the main risks?

The economy is still a downside risk for oil demand, with interest rates and inflation testing the surety of central banks’ touch and China’s recovery is critical. The direction of Russian production is another. We expect output to fall from 10.7 million b/d in 2022, to 10.2 million b/d this year. Russia’s output could move lower than our forecasted level for this year. It’s not beyond the realms of possibility that Russia announces another cut to its output as it did in March 2023, ahead of the OPEC+ target cut announced on 2 April.

{kind=link}