A hydrocarbon copy: the upstream industry’s return to international shale exploration

April 2026

April 2026

Author(s):

Robert Clarke

Vice President, Upstream Research

Robert leads our US onshore research, with a particular focus on the evolution of the tight oil sector.

Latest articles by Robert

-

Opinion

6 questions answered on the return to global shale exploration

-

The Edge

Can US success in tight oil and shale gas go global?

-

Featured

Upstream-oil-gas-2026-outlook

-

The Edge

US Lower 48 upstream: the US Majors’ long-term strategic advantage

-

Opinion

Video | Tariff turmoil: how big a cost hit will US oil and gas operators take?

-

Featured

Upstream oil & gas regions 2025 outlook

Josh Dixon

Senior Research Analyst, Upstream

Josh co-leads the Wood Mackenzie Plays Centre of Excellence.

Latest articles by Josh

-

Opinion

6 questions answered on the return to global shale exploration

-

The Edge

Can US success in tight oil and shale gas go global?

-

The Edge

Why Big Oil is warming to high-impact exploration

-

The Edge

How AI can unlock an extra trillion barrels of oil

-

Opinion

Q&A: Fields of dreams

-

Opinion

Introducing Analogues

US shale has been a 20-year growth engine for global upstream, but the sector is now maturing. Shale specialists seeking more scale will need to look at new frontiers and greenfield opportunities. Moving North American shale expertise abroad could transform some oil and gas markets, and provide opportunities for exploration and production (E&P) firms to leverage differentiated technical advantages.

Operators already explored for international shale in the 2010s, with only two large-scale successes, in Argentina and Saudi Arabia. Their limited progress was not because of a lack of new play potential, but rather because better growth options became available. The top explorers retreated from unproven international prospects to focus on lower-risk, lower-cost acreage in the US Permian Basin.

The unfolding repeat of global shale exploration is very different ‒ and better for it. Technology has pushed down the cost of supply in all shale basins. Explorers have better data and are being more selective in their projects. And, unlike the last foray, there are no new mega-growth plays in the US to overshadow international endeavours.

With the conflict in the Middle East putting a spotlight on alternative sources of oil and gas supply, we think international shale is likely to come into increasing focus.

Seeking shale at scale

Unconventional plays – shale and other extremely low-permeability reservoirs – have earned an irreplaceable position in the upstream sector because of their differentiated scale. Shale is the most common sedimentary rock in the world, present in virtually every petroleum system. Engineering producible reservoirs out of higher-volume source rocks where oil and gas are generated was the equivalent of E&P alchemy.

Shale has allowed the US and its domiciled E&Ps to drive roughly the same degree of growth over the past two decades as the next 10 countries combined. For perspective, Guyana – the industry’s largest conventional growth play – has increased production by just 0.7 million boe/d since 2019. US unconventional production has grown by more than four times that rate over the same period.

Energy-thirsty economies around the world remain envious of the US Lower 48’s shale success. Without it, the US would no longer be the world’s largest oil and gas producer; it would just squeeze into the top 10.

Figure 1: Supply growth by country and resource theme (2005-25)

Source: Wood Mackenzie Lens; tight oil includes associated gas

Global shale 1.0: failure to launch

Exploration in the early 2010s – we refer to this as global shale 1.0 – was driven by the industry wanting to replicate US unconventional success. Greenfield frontier geographies close to end markets were the preference: hungry for production, with local prices high enough to support projected asset economics.

However, early attempts hit major hurdles in terms of costs and above-ground regulations. Dry holes were common and exploration wells took years to permit and drill, fatiguing management teams and stakeholders. On top of that, the brewing overperformance of US shale set the stage for the 2015 and 2016 oil-price downturn. Exploration spending was slashed and marginal global shale projects became uneconomic.

The nail in the coffin, though, was the evolving opportunity in West Texas. Leading global shale explorers, who had been chasing marquee exploration projects in Poland, Colombia, Germany and China, all chose the Permian Basin instead for short-cycle reserve growth. The Permian was cheaper to develop, easier to execute and faster to scale up. It contained better-quality resource, even if projects forfeited the price premium that production in other countries could fetch.

Having given up on their international forays, the largest global shale 1.0 participants pivoted to spend more than US$100 billion on Permian acquisitions between 2012 and 2025. They also invested more than US$130 billion developing these Permian positions. Breakevens were driven down by more efficient operations and dramatically improved well recoveries, positioning the Permian lower on the global cost curve.

Figure 2: Permian production with leading global shale explorers retrenching

Source: Wood Mackenzie Lens; companies include ExxonMobil, Chevron, Shell, BP, ConocoPhillips, Marathon, EOG and APA.

Global shale 2.0: this time, it’s different

Companies and investors are becoming more convinced that demand for oil and gas will remain stickier than many anticipated. Consequently, operators are dusting off global shale 1.0 concepts as a starting point for capturing undeveloped unconventional resource. Exploration is not just picking up where it left off, however. Critical screening changes include:

- A focus on controlling spending. While still closely aligned with strong demand and regional price signals, just 20 high-grade plays are in the spotlight today, compared with more than 100 opportunities last decade. We estimate that over US$1 billion was spent on Poland shale gas exploration alone between 2009 and 2015, for instance, with no commercial outcome.

- Regulation as a filter. Explorers know the countries to avoid. Bans on hydraulic fracturing or unworkable fiscal terms will make certain projects impossible. Companies also have a better understanding of supply-chain risks, such as red tape that restricts the import of critical drilling and completion equipment.

- Stronger geopolitical considerations. Russian tight oil in the Bazhenov and Domanik plays is a huge prize that is off limits to Western capital for the foreseeable future. US companies are unlikely to reengage with China’s Sichuan basin shale either, despite the country’s national oil companies (NOCs) having some success in tight gas and coalbed methane in the neighbouring Ordos basin.

Two US shale leaders stepping into global shale 2.0 have stoked the fire considerably. Continental has moved into Argentina through multiple deals and will operate one of its Vaca Muerta assets. It also has a new unconventional joint venture with the Turkish Petroleum Corporation (TPAO). Before the Iran war, EOG had made unconventional entries into Bahrain and the United Arab Emirates.

Each of these companies has a strong exploration commitment, access to leading technical skillsets and a history of breaking open new plays. In fact, some of the global shale 2.0 plays being studied are assets that EOG evaluated in global shale 1.0.

If other US shale specialists undertake similar moves abroad, momentum will accelerate and, with it, stakeholder acceptance for exploration. Fear of missing out will set in and even more US E&Ps will follow.

Figure 3: Unconventional target geographies – building on the last decade’s learnings

Source: Wood Mackenzie. Shale and tight oil and gas assets only. Excludes Russia.

The biggest difference: there’s no ‘new Permian’ in the US

The greatest advantage for global shale 2.0 is that there is no new US play on the scale of the Permian Basin to contend with.

US exploration all but dried up after the horizontal Permian boom took off. Frontier drilling was already on a downward trend. The only tangible exploration successes have been new and smaller zones within developed basins, or greenfield play concepts that are a fraction of the Permian’s size.

Figure 4: The US Lower 48 exploration drought

Source: Wood Mackenzie and Novi Labs, Inc. Well categorisations based on density rules within a five-mile radius at first production date.

The reasons to try to discover another Permian in the US are compelling. The maturing Permian now holds more value than all other Lower 48 basins combined. It has become the dominant project in ExxonMobil and Chevron’s global portfolios, and it offers cost-of-supply metrics on a par with top-tier conventional projects globally.

The prize would be great if it could be found, but nothing suggests that it will be.

Argentina and Saudia Arabia show the potential

Two major success cases from global shale 1.0 have proved that international scale is possible given the right commercial and technical factors. Combined, the Argentinian and Saudi Arabian projects will produce more than 2.5 million boe/d in the next decade. They are set to absorb a collective US$250 billion of capex and could be as transformational to their own domestic markets as the Permian has been to the US.

The Jafurah liquids-rich shale gas project came online in early 2026. It produces from the Jurassic source rocks that feed Saudi Arabia’s conventional behemoths. The rich gas play allows for greater oil exports, as the Kingdom can stop burning oil for power generation, particularly in its summer months. An electrifying economy needs more gas, and volumes from Aramco’s conventional fields alone cannot meet growing demand. Peak production is estimated at 2 bcfd of sales gas and over 600 kb/d of condensate.

The Vaca Muerta play, meanwhile, has been slow to build, but is now producing roughly 1 million boe/d. We think it can produce over 1.6 million boe/d at peak. Competition from 20 companies is driving progress and there is volume upside from better-developed oilfield service (OFS) support and even more mergers and acquisitions (M&A) to bring in new players with ideas and ambition. This growing ecosystem of technology, engineering and capital is opening up global waterborne export opportunities for both oil and gas that will strengthen the Argentinian economy.

Figure 5: Argentinian unconventional production forecasts growing steadily

Source: Wood Mackenzie

Which global shale prospects are most attractive today?

International plays must closely match top US projects on a host of geological analogue factors, including stratigraphy, mineralogy, geochemistry and structure. Pathways to infrastructure buildout and flexibility in project planning are also needed, particularly for dense well developments and high-frequency permitting. Partnerships must be incentivised to increase data sharing and collaboration.

Operators will also need to have confidence that the latest US shale technologies can be imported and deployed at scale. One or two high-spec horizontal rigs and pressure pumping fleets entering a country is not enough to meaningfully lower costs. Project execution in the field must also perform dramatically better than global shale 1.0.

Figure 6: Costs need to fall: US and global shale play comparison

Source: Wood Mackenzie. *2026 cost structures for Permian (3), Eagle Ford, Marcellus, Haynesville, Bakken and Montney.

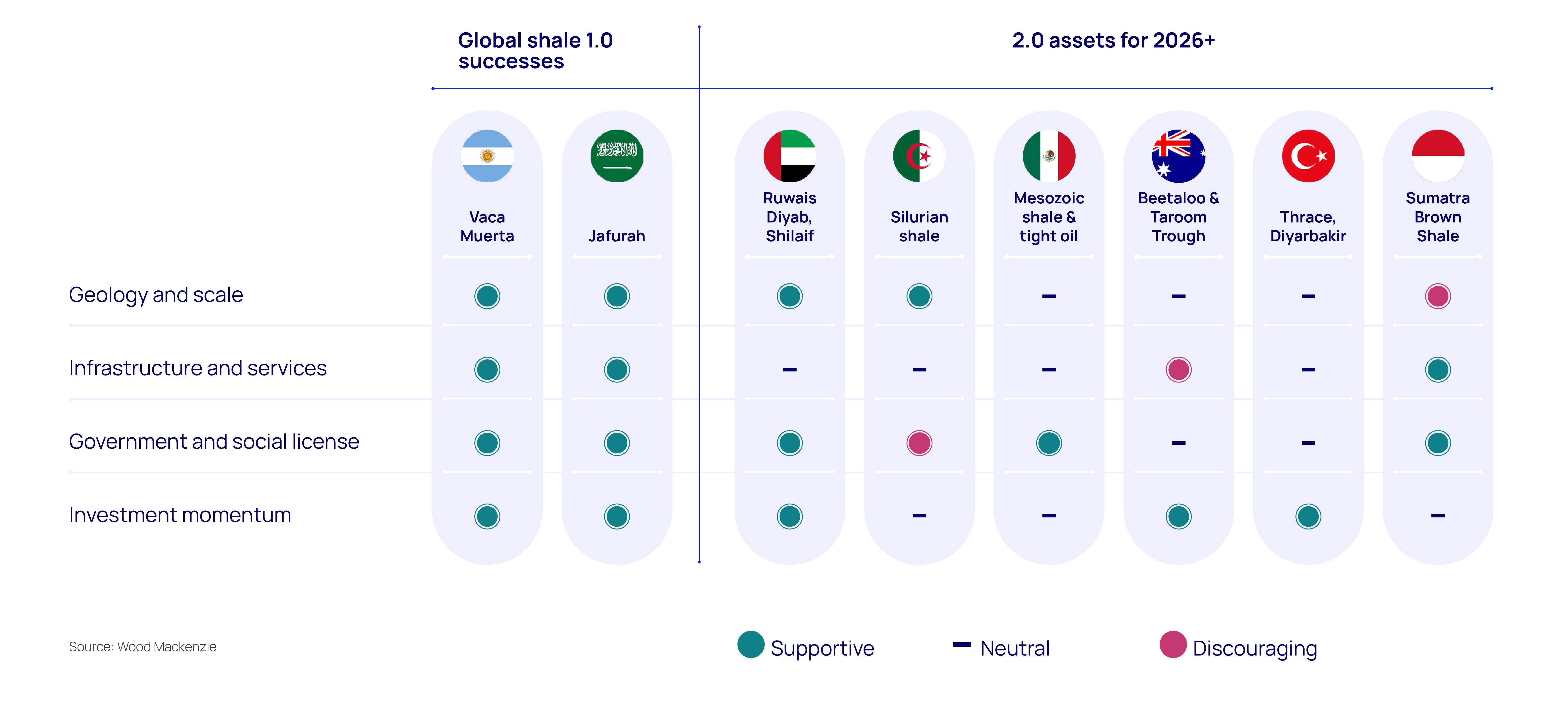

It is key that US operators ask harder and smarter questions about these challenges. The UAE, Algeria, Mexico, Australia, Türkiye and Indonesia are leading focal points, even if some of the plays were already studied for global shale 1.0.

Figure 7: Highest-focus targets in global shale 2.0

{kind=link}

Source: Wood Mackenzie

Ranking the shale prospects

We’ve applied a scorecard system to the above plays to rank growth potential, with a focus on scale and timelines.

- UAE: the Abu Dhabi National Oil Company (ADNOC) is moving beyond the de-risking phase of its unconventional programme. Final investment decisions (FIDs) were expected in 2026 before the Iran war began. The company is prioritising unconventional gas to support a 2030 gas self-sufficiency target. There is a spotlight on fiscal, offered gas prices and regulatory flexibility to attract and retain global interest. Over 300 wells per year could be drilled.

- Algeria: the Lower Silurian shale has exceptional subsurface potential and the market prize is piped exports that diversify Europe’s gas supply. Algeria already has a tight gas sector, but additional OFS bottlenecks need to be fixed for ExxonMobil and Chevron to proceed with exploration partnerships.

- Mexico: Pemex has aggressive but achievable shale gas and tight oil production targets for 2030 that have been prioritised because of US trade tensions. Targets span beyond the extension of the US Eagle Ford play. Equipment imports will be easier than in other countries, and US operators would be more comfortable with nearby geographies for operations.

- Australia: gas exploration in the Beetaloo sub-basin is progressing with a unique blend of global upstream and OFS partnerships. However, other plays, including deep coals and tight oil and gas in the Cooper and Bowen basins, add upside. Liquified natural gas (LNG) backfill and supply to the premium-priced east coast market are core drivers.

- Türkiye: Continental is drilling exploration wells in the Diyarbakır and Thrace basins in a project moving at lightning speed compared with activity in the 2010s. Neighbouring countries’ gas-market dynamics mark this strategic supply opportunity longer-term, but Türkiye’s aspirations to be a regional gas hub require significant infrastructure investment.

- Indonesia: regulators and domestic producers are actively seeking US participation in the Sumatra basin. Tight oil projects will benefit from new OFS technology partnerships, and the government has experience regulating high-density drilling campaigns. Targets include lacustrine (lake deposition) sediments, which are different from the geology of the largest US shale plays. Lacustrine shales were once thought too challenging to commercialise, but this has been disproven by the success of the Uinta basin in the US.

The potential obstacles

Commercially successful outcomes are far from a sure thing. The scars of global shale 1.0 failures run deep. To create a competitive renaissance, countries serious about enabling shale must commit to bringing projects into existence.

Redefined commercial, procurement and fiscal frameworks are necessary. Production-sharing contracts were not designed for short-cycle capex developments, as high reinvestment rates quickly consume cost-recovery pools. Ring-fencing a resource play is complicated as well, because of ill-defined field boundaries. US players will favour the familiarity of fixed royalty concessions, provided rates are low enough.

Geopolitical uncertainty in some target plays remains high and investors may prefer to wait for stability. Elections, for instance, have upended global shale potential before; look no further than hydraulic fracturing bans in Colombia and the UK. Argentina, too, has a history of cyclical capital controls.

Horizons Live

Watch the replay of our Horizons Live webinar. This month's report authors discussed the key findings and tackled your questions in a Q&A session.

Explore our latest thinking in Horizons

Loading...

For details on how your data is used and stored, see our Privacy Notice.

Why sign-up?

By submitting your details you’ll gain access to the latest Horizons report, part of a thought-leadership series exploring the themes shaping the energy natural resources landscape. You’ll also receive the Inside Track, our weekly newsletter, so you won’t miss out on future editions.