Sign up today to get the best of our expert insight in your inbox.

Can US success in tight oil and shale gas go global?

FOMO a factor driving appetite to invest in international plays

1 minute read

Simon Flowers

Chairman, Chief Analyst

Simon Flowers

Chairman, Chief Analyst

Simon is our Chief Analyst; he provides thought leadership on the trends and innovations shaping the energy industry.

Latest articles by Simon

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

Robert Clarke

Vice President, Upstream Research

Robert Clarke

Vice President, Upstream Research

Robert leads our US onshore research, with a particular focus on the evolution of the tight oil sector.

Latest articles by Robert

-

Opinion

6 questions answered on the return to global shale exploration

-

The Edge

Can US success in tight oil and shale gas go global?

-

Featured

Upstream-oil-gas-2026-outlook

-

The Edge

US Lower 48 upstream: the US Majors’ long-term strategic advantage

-

Opinion

Video | Tariff turmoil: how big a cost hit will US oil and gas operators take?

-

Featured

Upstream oil & gas regions 2025 outlook

Josh Dixon

Senior Research Analyst, Upstream

Josh Dixon

Senior Research Analyst, Upstream

Josh co-leads the Wood Mackenzie Plays Centre of Excellence.

Latest articles by Josh

-

Opinion

6 questions answered on the return to global shale exploration

-

The Edge

Can US success in tight oil and shale gas go global?

-

The Edge

Why Big Oil is warming to high-impact exploration

-

The Edge

How AI can unlock an extra trillion barrels of oil

-

Opinion

Q&A: Fields of dreams

-

Opinion

Introducing Analogues

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

Latest articles by Gavin

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

Opinion

Why US Henry Hub natural gas prices are set to rise | Webinar replay

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

The oil and gas industry needs to strengthen portfolios for the next decade to avert inevitable production declines. Could a reinvigoration of international shale – Global Shale 2.0 – become part of the solution? Our upstream specialists Robert Clarke and Josh Dixon shared their thoughts with me.

Why is shale different?

It’s more of a technical challenge compared with most conventional oil and gas fields. Early this century, pairing hydraulic fracturing with long lateral horizontal wells in the US unlocked vast resources of oil and gas held in these low permeability rocks, making shale economic. Exploitation requires high well density for modest recovery factors – wells have a short window of peak rate so there’s a constant need to invest in drilling new wells to sustain or grow production.

Yet doing things differently with shale has transformed the US into the biggest oil and gas producer in the world, bigger than Saudi Arabia and Russia combined when NGLs are included. Shale has become the backbone of American energy dominance.

Why haven’t shale plays taken off elsewhere?

There are plenty of other shale-rich basins around the world, in some cases holding vast resource potential that even exceed some US plays. None, though, has the same advantages the US had – access to rapidly improving technology, a huge service sector and expanding infrastructure, access to capital, liquid M&A markets and a relatively favourable fiscal regime.

Most importantly, nowhere else has a domestic oil and gas industry with hundreds of operators, large and small, with, at least in the early days, many prepared to bet the ranch in a Darwinian battle to capture and exploit the best acreage.

The absence of most of these drivers was a big part of international Shale 1.0 failing last decade, not helped by a weak external environment and tricky regulations. Ultimately, initial exploration didn’t justify the investment required to achieve scale and commercial breakeven costs as good as the options in the US, with those in the Permian the benchmark.

What’s enticing the industry to consider Global Shale 2.0?

Having ridden the US shale wave, larger US shale players are again looking to surf elsewhere. As US plays mature, it will get harder for companies to sustain their portfolios domestically. Companies are now ready to consider overseas opportunities to leverage the competitive advantages learned from the US Lower 48.

Transferring these advantages won’t be easy. Operators will need to have confidence that the latest US shale technologies can be imported and deployed at scale. One or two high-spec horizontal rigs and pressure pumping fleets entering a country is not enough to meaningfully lower costs. Project execution in the field must also perform dramatically better than in Global Shale 1.0.

{kind=link}

Where are the promising plays and what are the main challenges?

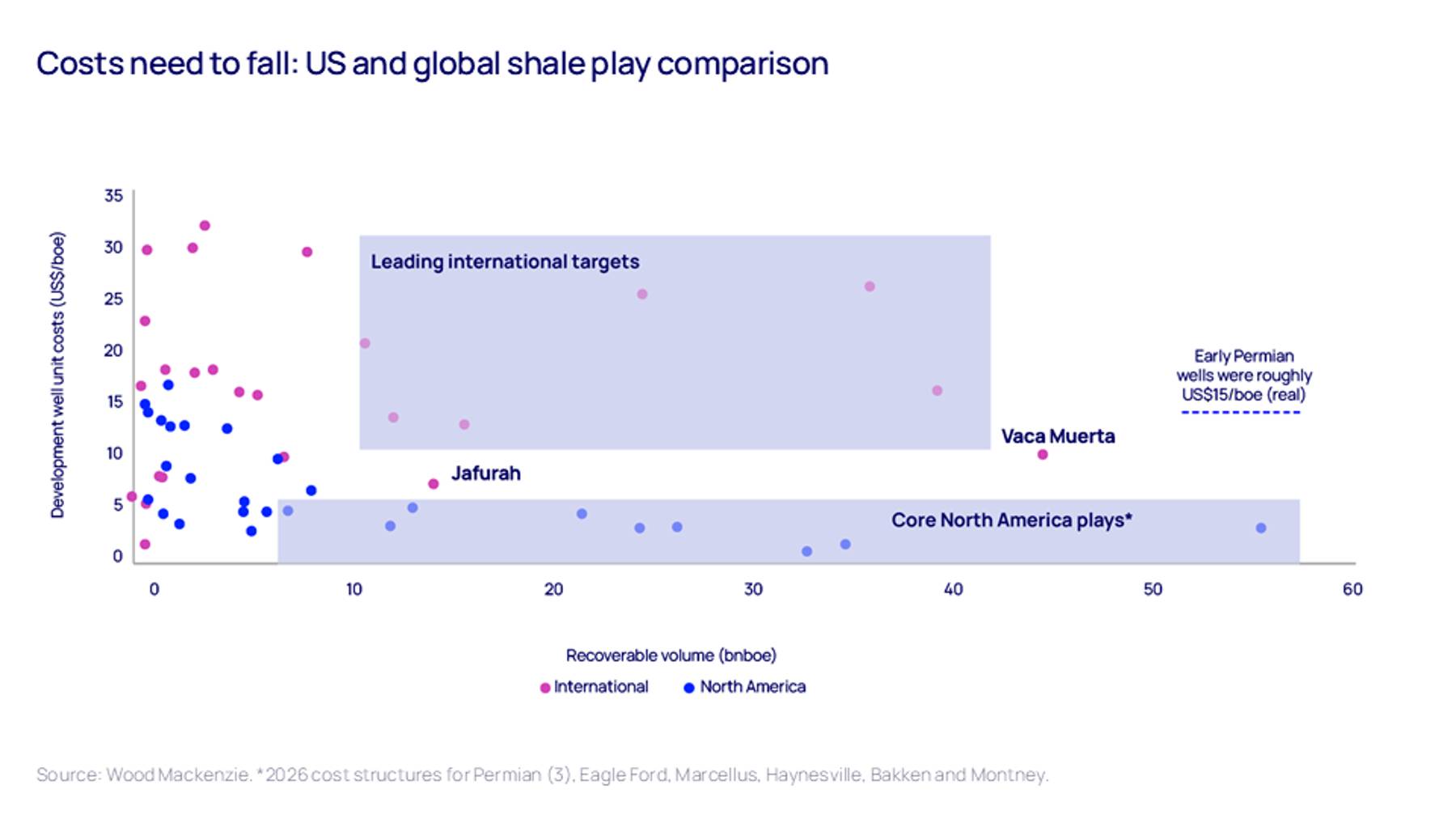

There are as many plays in the rest of the world as in North America, yet none on the horizon are looking remotely like the next Permian. Two have already proven the concept – Argentina’s Vaca Muerta and Saudi Arabia’s Jafurah, both with large resource and comparatively modest development well unit costs.

After a slow haul for over a decade, Vaca Muerta produces 1.0 million boe/d today. Saudi Arabia’s Jafurah shale gas play came onstream early in 2026. We expect these two plays together to attract investment of US$250 billion over their lifespans and produce a combined 2.5 million boed.

Among emerging plays, the UAE, Algeria, Mexico, Australia, Türkiye and Indonesia are attracting most of the industry’s interest. Our analysis explores the various challenges each faces whether geology and scale, infrastructure and services, government and social license, and investment momentum. Fiscal rules are another – production sharing contracts, common in many countries, were not designed for ongoing short-cycle capex projects. US operators are likely to seek the fixed royalty concessions they have thrived under domestically, provided the rates are low enough.

Will the war in Iran damage investment in Global Shale 2.0?

Importers certainly will look for greater diversity of oil and gas sources to strengthen their security of supply. That’s good news for any oil and gas basins outside the Gulf. That, though, doesn’t change the strategic option for the larger US players with portfolios concentrated in mature domestic shale and looking to repeat their success in international plays.

Six of our eight promising Global Shale 2.0 hotspots are situated well away from the Gulf, while those plays in the Gulf can mitigate risks posed by the war. The UAE and Saudi Arabia both already have alternative liquids export capacity that avoids the Strait of Hormuz and will build more.

Finally, many international oil companies missed the big opportunity in US shale and now have FOMO. The question they will be asking themselves now is whether, in a decade’s time, they will have similar regrets about Global Shale 2.0.

Make sure you get The Edge

Every week in The Edge, Simon Flowers curates unique insight into the hottest topics in the energy and natural resources world.

Sign up today using the form at the top of the page.