Sign up today to get the best of our expert insight in your inbox.

Why Big Oil is warming to high-impact exploration

Success in ultra-deepwater plays can create material value

1 minute read

Simon Flowers

Chairman, Chief Analyst

Simon Flowers

Chairman, Chief Analyst

Simon is our Chief Analyst; he provides thought leadership on the trends and innovations shaping the energy industry.

Latest articles by Simon

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

-

The Edge

Ten takeaways from WoodMac’s LNG Conference

Andrew Latham

Senior Vice President, Energy Research

Andrew Latham

Senior Vice President, Energy Research

With his extensive exploration expertise Andrew shapes portfolio development for international oil and gas companies.

Latest articles by Andrew

-

The Edge

Why Big Oil is warming to high-impact exploration

-

The Edge

How AI can unlock an extra trillion barrels of oil

-

Opinion

Q&A: Fields of dreams

-

Opinion

SEC 2025: Why the SEAPEX region still needs high-impact exploration

-

The Edge

How ultra-deepwater is revitalising oil and gas exploration

-

Opinion

Geothermal energy: the hottest low-carbon solution?

Josh Dixon

Senior Research Analyst, Upstream

Josh Dixon

Senior Research Analyst, Upstream

Josh co-leads the Wood Mackenzie Plays Centre of Excellence.

Latest articles by Josh

-

Opinion

6 questions answered on the return to global shale exploration

-

The Edge

Can US success in tight oil and shale gas go global?

-

The Edge

Why Big Oil is warming to high-impact exploration

-

The Edge

How AI can unlock an extra trillion barrels of oil

-

Opinion

Q&A: Fields of dreams

-

Opinion

Introducing Analogues

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

Latest articles by Gavin

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

Opinion

Why US Henry Hub natural gas prices are set to rise | Webinar replay

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

High impact exploration is enjoying a renaissance. A peer group of 30 of the world's largest E&P companies face production declines that average nearly 40% between 2025 and 2040. They need to look beyond the war and shape resource capture strategies to fill the gap in volumes.

I asked our experts, Dr Andrew Latham and Dr Josh Dixon from our exploration team, why Big Oil sees frontier exploration playing an increasingly important part of the solution.

Why do we need exploration?

The upstream industry has an enormous and ongoing challenge. For liquids alone, today’s onstream fields will fall short by 300 billion barrels of the almost 1,000 billion barrels needed to meet the cumulative demand through 2050 under our base case, absent reserve upgrades. Exploration can add not just volume but value by finding advantaged barrels to displace higher-cost or otherwise disadvantaged resources, whether oil or gas.

How much value is exploration creating?

Our analysis shows that the industry created US$54 billion of value after deducting US$97 billion of spend on exploration from 2021 to 2025, using a long-term Brent price of US$65/bbl (real). At US$85/bbl Brent, value creation more than doubles to US$120 billion.

Values in recent years are typically lower, given companies’ tendency to err on the conservative side with new discoveries. As more information has come to light, we’ve just doubled our initial US$2.8 billion development valuation (ex-E&A spend) to US$5.7 billion for BP’s (100% equity) giant Bumerangue oil, gas and condensate find in Brazil, announced in August 2025. That on its own lifts industry value creation in 2025 to over US$10 billion, in line with the industry’s five-year average.

Who is leading high-impact exploration?

Big Oil. The high-value creation opportunities are increasingly in ultra-deepwater frontier plays. You can just about count on two hands the number of companies with the risk appetite and skill set to operate in these environments – the seven Majors and a few national oil companies, including Petrobras, PETRONAS and Türkiye’s TPAO. Independents – including Murphy, Apache and Woodside – are also in the deepwater operators club but drill fewer wells.

These frontier exploration leaders are showing an inclination to take high equity stakes to gain more exposure to the upside of any success. To take two giant examples – BP with Bumerangue, and Eni’s 100% initial stake in Egypt’s Zohr gas discovery in 2015.

Another source of capital comes from others investing as non-operating partners. QatarEnergy, for example, has had considerable success as a joint venture partner, discovering new resources in Brazil, Namibia, Cyprus and the Republic of the Congo.

Is spend increasing?

Industry spend on exploration is relatively stable, averaging US$19 billion on 633 wells for 2021-25. In our view, the dip to US$16 billion on 388 wells in 2025 is an aberration. The resilience of investment reflects the long-term nature of the sharp end of the upstream value chain and is despite a near-doubling of rig day rates, which comprise a substantial part of well costs.

Where are the high-impact hot spots?

Ultra-deepwater plays in water depths greater than 1,500 metres. The focus follows the high-value-creating discoveries in the last five years, including those by ExxonMobil (Guyana), Eni (Côte D’Ivoire, Indonesia, Cyprus), BP (Brazil) and TPAO (Black Sea). Frontier explorers are widening the net to underexplored basins, including Brazil’s Foz do Amazonas, as well as extensions of existing plays in Angola, Suriname and elsewhere.

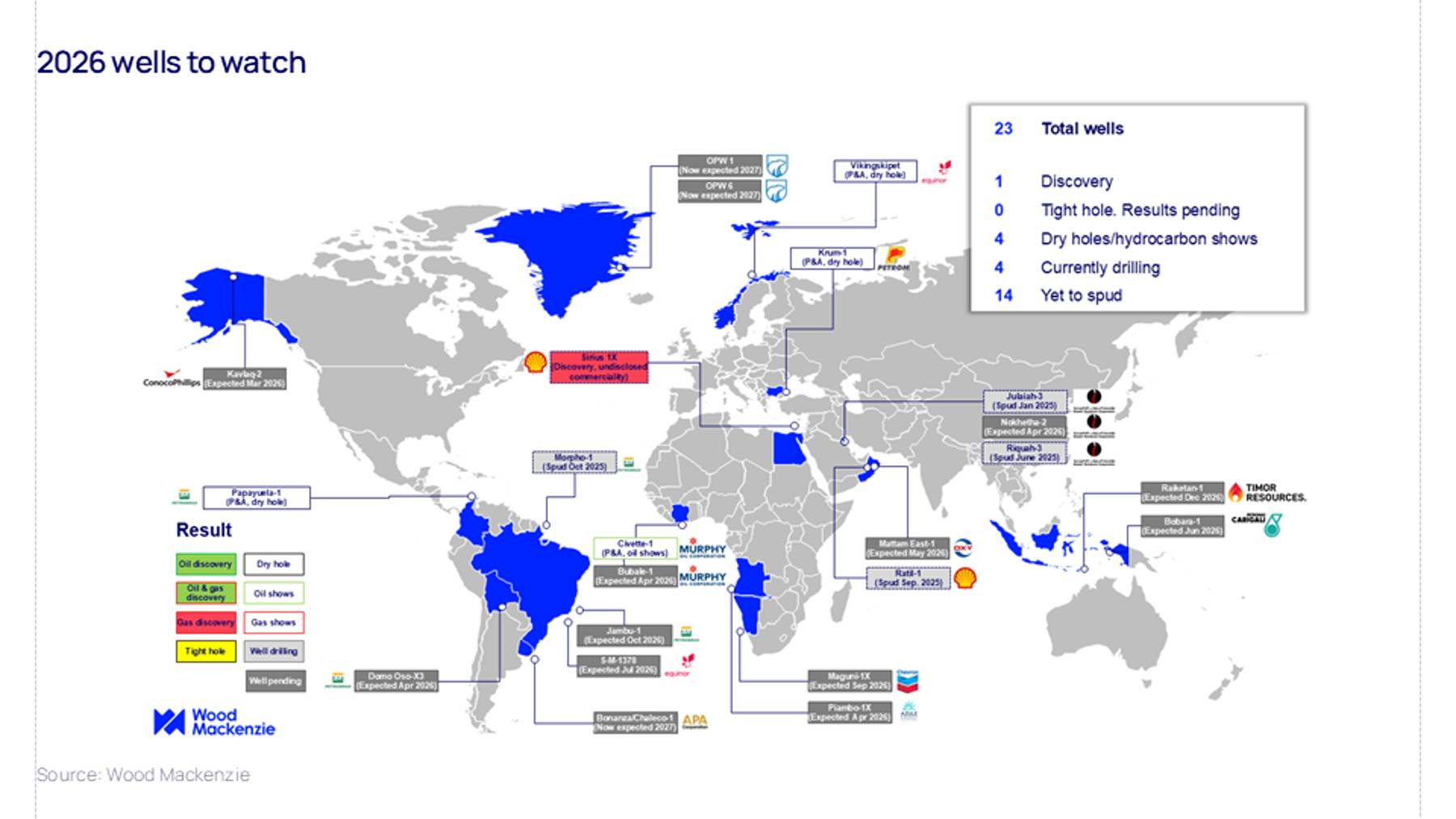

What are the big frontier wells to watch for in 2026?

First, it’s been a sobering start to the year. The first four big wells we’d been watching all came in dry – that’s the game, and players know the risks.

Of the 23 wells we identified in January as Wells to Watch in 2026, these four are of high potential value:

- Morpho (Petrobras 100%), currently drilling is an 800-mmboe potential play-opener in the Foz do Amazonas, Brazil’s most northerly basin, adjacent to French Guiana.

- The OPW1 (800 mmboe) and OPW6 (338 mmboe) licences (Greenland Energy Company 70%), a highly anticipated campaign on Greenland’s eastern coast testing prospects in a play analogous to the adjacent – and prolific – Norwegian shelf.

- S-M-1378-1 (Equinor 100%) in Brazil’s Santos Basin will target the same pre-salt microbial carbonates of BP’s Bumerangue giant discovery.

- Murphy’s Bubale-1, second of its three well programmes in Cote d’Ivoire, is a 440-mmboe oil prospect.

{kind=link}

Make sure you get The Edge

Every week in The Edge, Simon Flowers curates unique insight into the hottest topics in the energy and natural resources world.

Sign up today using the form at the top of the page.