Energy transition outlook: EU

The European Union maintains its position as a global climate leader, yet faces mounting challenges in translating ambitious targets into tangible outcomes – and implementation gaps are widening

3 minute read

Lindsey Entwistle

Principal Analyst, Energy Transition

Lindsey Entwistle

Principal Analyst, Energy Transition

Lindsey provides analysis and insights into global policy, regulations and disruptive technologies.

Latest articles by Lindsey

-

Opinion

Energy transition outlook: EU

-

Opinion

Energy transition outlook: Americas

-

Opinion

How is energy transition investment evolving in 2026?

-

The Edge

How the Iran war could change energy markets

-

Opinion

Energy transition outlook: UK

-

Opinion

Energy evolution: navigating the path to a sustainable future

Zoé Sulmont

Research Analyst, Energy Transition

Zoé Sulmont

Research Analyst, Energy Transition

Latest articles by Zoé

-

Opinion

Energy transition outlook: EU

-

Featured

Nuclear 2026 outlook

-

Opinion

Energy evolution: navigating the path to a sustainable future

-

Opinion

Hot rocks: geothermal momentum continues to build

-

Opinion

Rock solid: geothermal’s upward trajectory

-

The Edge

The coming geothermal age

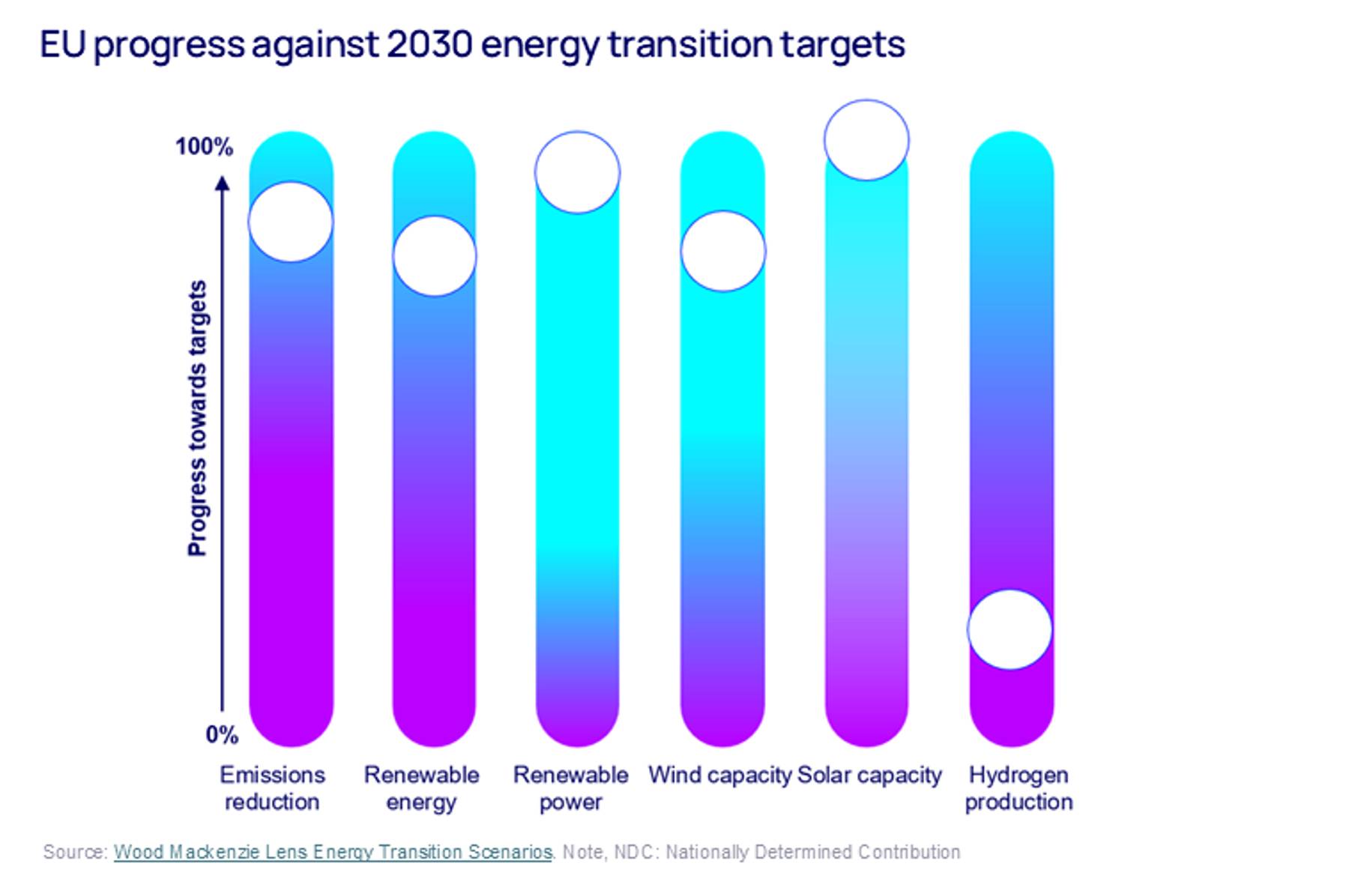

Tensions are mounting in Europe's climate ambitions. As the EU proposes tightening its 2040 emissions target to 85-90%, implementation gaps are widening across key sectors.

Our updated energy transition outlook (ETO), from our Energy Transition Service, maps out four energy transition pathway scenarios, while the regional updates delve into the detail at country level. The EU27 edition draws on cross-sector expertise across power and renewables, oil and gas, metals and mining, and emerging technologies including low-carbon hydrogen, CCUS, advanced nuclear and geothermal.

Read the EU27 energy transition outlook to discover:

- Why the EU is missing near-term climate targets despite comprehensive policy frameworks.

- Commodity and power market outlooks to 2060 across EU countries, in base case, delayed transition, country pledges and net zero scenarios.

- Where emerging energy transition technologies are rising to the occasion or falling short including coverage of electric vehicles and heating, low-carbon hydrogen, carbon capture and advanced nuclear.

- Investment implications across power, grid infrastructure and emerging technologies to 2060.

You can access a complimentary extract from the EU-27 edition by filling in the form at the top of the page. And read on for a short introduction to some of our most frequently asked questions.

Are EU climate targets on track?

Some members are achieving goals early; others are lagging behind.

The EU maintains its position as a global climate leader, yet faces mounting challenges in translating ambitious targets into tangible outcomes. The bloc's comprehensive policy framework, anchored by the Green Deal and Fit for 55 package, sets the world's most stringent decarbonisation pathway. But implementation gaps are widening as economic pressures, geopolitical tensions and industrial competitiveness concerns reshape priorities.

{kind=link}

How are geopolitical factors influencing Europe’s energy landscape?

Geopolitical tensions have locked-in LNG imports but low-carbon energy is essential to national and economic security.

The war in Ukraine fundamentally altered the EU energy landscape, accelerating the shift away from Russian fossil fuels whilst highlighting vulnerabilities in critical supply chains. The Middle East conflict has put energy security once more under the spotlight. Defence spending commitments compete with climate investments for fiscal resources.

Yet energy security and climate goals increasingly align, with domestic renewable capacity viewed as essential for strategic autonomy.

How is adoption of EVs, heat pumps and other energy transition technologies progressing in the EU?

Consumer adoption of key transition technologies faces headwinds. The proposed reversal of the 2035 ICE car ban undermines EV deployment. Heat pump installations lag targets across most EU member states, constrained by high upfront costs and complex installation requirements. Infrastructure gaps, particularly for EV charging, compound adoption challenges.

The bloc is recalibrating its technology strategy. Advanced nuclear, AI and offshore wind are in focus as hydrogen and CCS contend with price driven markets.

What’s the scale of the energy transition investment opportunity?

Globally, the energy transition presents a US$11.7 to US$16.2 trillion investment opportunity. Power generation and grid infrastructure require around two thirds of total capex across all scenarios.

Find out more about the investment opportunity in the EU – and the ambition and investment needed across all four energy transition scenarios – in the full report.