Energy transition outlook: UK

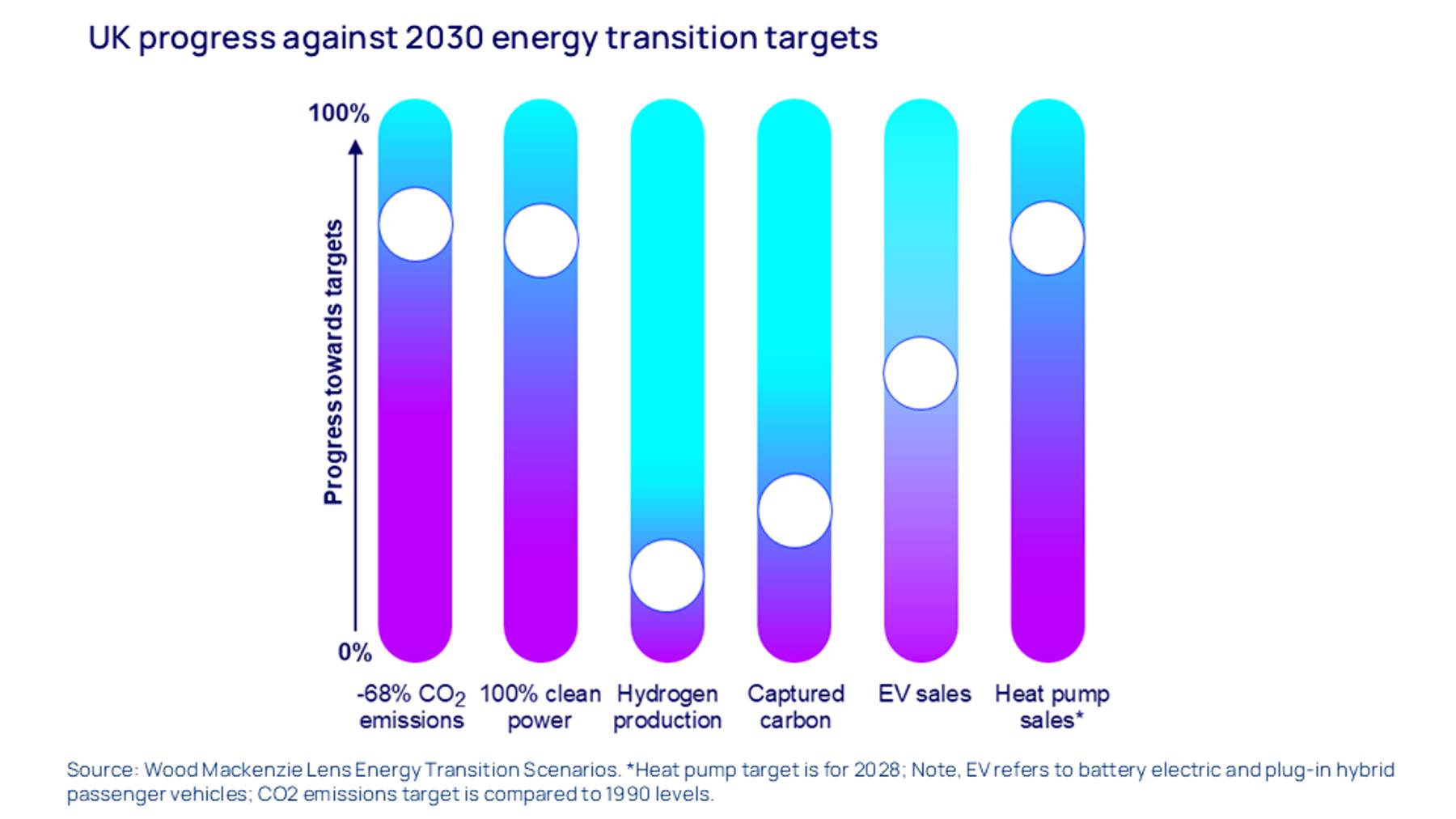

Crunch time for the UK energy transition – decarbonisation strategy has halved its energy-related emissions since 1990 but nearly all 2030 targets are currently out of reach

2 minute read

Lindsey Entwistle

Principal Analyst, Energy Transition

Lindsey Entwistle

Principal Analyst, Energy Transition

Lindsey provides analysis and insights into global policy, regulations and disruptive technologies.

Latest articles by Lindsey

-

Opinion

Energy transition outlook: EU

-

Opinion

Energy transition outlook: Americas

-

Opinion

How is energy transition investment evolving in 2026?

-

The Edge

How the Iran war could change energy markets

-

Opinion

Energy transition outlook: UK

-

Opinion

Energy evolution: navigating the path to a sustainable future

Prakash Sharma

Vice President, Head of Scenarios and Technologies

Prakash Sharma

Vice President, Head of Scenarios and Technologies

Prakash leads a team of analysts designing research for the energy transition.

Latest articles by Prakash

-

The Edge

Will falling populations reshape energy demand?

-

Opinion

How is energy transition investment evolving in 2026?

-

The Edge

How the Iran war could change energy markets

-

Opinion

Energy transition outlook: Asia Pacific

-

Opinion

Energy transition outlook: Africa

-

Opinion

Energy transition outlook: Middle East

Deliberate decarbonisation strategy has seen UK energy related emissions halve since 1990. Following this success, the UK government doubled down on its Paris Agreement pledge with an ambitious 2035 nationally determined contribution (NDC) target. But it’s now crunch time – and nearly all 2030 targets are currently unattainable.

Our latest energy transition outlook (ETO) draws on Wood Mackenzie Lens Energy Transition Scenarios to explore the progress made and obstacles to overcome on the road to net zero. The global ETO maps out four energy transition scenarios with increasing levels of ambition and investment, while the regional reports – now updated for 2025-26 – delve into the detail at country level.

Access a complimentary 19-page extract from the UK edition by filling in the form at the top of this page. And read on for a short introduction to some of the key themes.

UK climate targets are out of reach this decade despite big wins with coal power phaseout and record renewables

UK wind and solar generation has more than doubled since 2015 and coal power has been phased out. Renewables supplied over half of generated power in 2025.

Yet, while the UK has cultivated an international reputation for climate leadership through ambitious targets and widespread support packages for low-carbon sectors, progress towards its net zero targets falls short.

{kind=link}

Spiralling costs, delays to critical infrastructure deployment and shrinking consumer and industry confidence all undermine the UK’s ability to achieve its energy strategy. Policy uncertainty compounds these challenges, eroding investor confidence and hindering industrial planning.

Policy reversals on the internal combustion engine ban exemplify the problem – download the report extract to learn more.

Imports remain critical to the UK’s long-term energy strategy, despite domestic capabilities and resources

Oil and gas demand falls by 24% and 18% respectively by 2035, with EVs and renewable power driving the decline. Yet fossil fuels remain critical to UK energy supply. Transport is a key driver at 72% of oil demand, while 54% of gas demand remains from residential, commercial and agriculture sectors.

Oil and gas will therefore remain critical to transportation and heating homes for decades to come. Bans on new exploration licences in the North Sea drastically limit domestic supply, locking in dependence on imports. The government must now empower new sectors to create skilled jobs in affected areas to ensure continued support for a “just transition”.

Download the complimentary executive summary of the report to read more on why the UK remains hooked on imports – and where export opportunities could lie.

New energy transition technologies: searching for deployment pathways

UK support for new low-carbon technologies has historically been broad. It must now adopt a more targeted approach, directing resources towards strategic technologies with clear commercial pathways. Decision-makers must "fail faster", as protracted periods of policy or commercial uncertainty constrain emerging sectors and delay necessary course corrections.

Our UK energy transition outlook report highlights that:

- Offshore wind shows signs of revival following CfD reforms, although meeting 2030 targets remains unlikely.

- Carbon capture progresses through industrial clusters and subsidies, although behind schedule.

- Low-carbon hydrogen has been downgraded in the face of high-profile project cancellations of both electrolytic and blue hydrogen, as energy majors pivot strategies back to fossil fuel production.

- Advanced nuclear and artificial intelligence (AI) are in focus: an AI Growth Zone will collocate data centres with small modular reactors (SMRs) in a bid to leverage existing nuclear capabilities. Data centre scale-up lags China, the US and some European neighbours, reaching less than 2% of total power demand by 2030.

Download the 19-page executive summary of the UK energy transition outlook to learn more about the low-carbon technology landscape in the UK and the US$1.86-2.63 trillion investment opportunity between now and 2060.