Discuss your challenges with our solutions experts

The two polyester feedstocks – purified terephthalic acid (PTA) and monoethylene glycol (MEG) – in the world's most important polyester market China, have recently moved towards a total paper business.

The MEG futures market was officially launched on December 10 at the Dalian Commodity Exchange (DCE), while the decade-old PTA futures market at the Zhengzhou Commodity Exchange (ZCE) moved to welcome non-Chinese participants on November 30.

Foreign access to Chinese contracts

The ZCE allows any company or individual who is willing to put up the guarantee deposit of up to 20% of the value of the transaction to participate in PTA futures trading. Non-Chinese businesses are now allowed to place the deposit in the US dollar equivalent.

This is attractive for some foreign PTA players who face occasional shortages, particularly during seasonal booms when the downstream polyester industry swings into maximum operations. Prohibitive pricing vis-à-vis China in some of these less active markets can also contribute to the lure.

As of early December, at least a handful of PTA and polyester businesses in Korea, India and Indonesia have started trades at ZCE's PTA bourse. More from the rest of Asia, as well as the Middle East and Europe could join in the coming months.

The MEG futures market, on the other hand, is not open to non-Chinese registered businesses, suggesting a parochial approach at least for now.

Futures as hedging tools

With this increase in liquidity – both in terms of funds and participation – comes price fluctuations, which is already seen in the PTA market in recent years.

Paper trades also present a useful tool for hedging against risks, especially price fluctuations. The market leader for PTA, Chinese producer Yisheng Petrochemical, has used the futures market to not only hedge its risks into the forward months, but also to maximise its profits and/or minimise its losses in China.

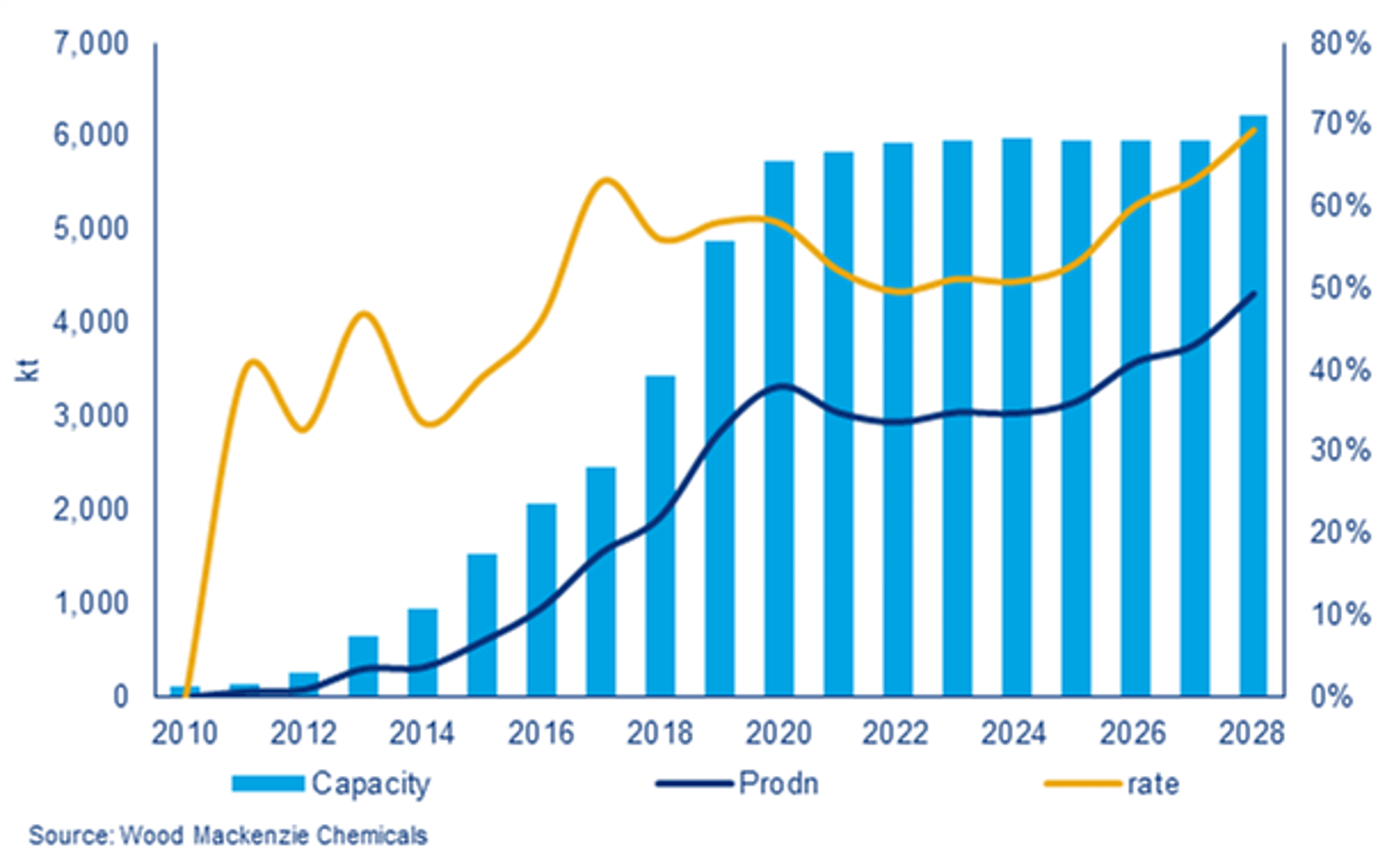

This is especially important in an increasingly insular Chinese PTA market which has flipped into serious overcapacity since 2015.

With a glut of fresh capacities starting up from 2019 onwards, peaking by 2021, the world of MEG could see gross overcapacity in 2-3 years. With the MEG futures market becoming more sophisticated by then, it presents a good tool for buyers and sellers alike to hedge their risks in a supply overhang.

Marginalisation of coal-based MEG

Specifically on MEG, the move towards paper trades based on the rules of the DCE is actually a de facto marginalisation of products churned out by coal-based units, via the dimethyl oxalate route. Already a controversial way of MEG production itself, the end-product is viewed with suspicion by many market participants, especially end-users.

{kind=link}

The exclusion of coal-based MEG from the futures market by DCE, because of the need to adhere to the stringent specification of at least 99.9% of purity against water, could save traditional producers using ethylene as raw material from being forced to bow out of the market, and hence cushion the impact of an oversupply into the 2020s.