Discuss your challenges with our solutions experts

After the crash: five key changes in US Gulf of Mexico

How offshore E&Ps have adjusted their budgets and production levels in response to the 2020 oil price crash

1 minute read

By Mfon Usoro, Research Analyst, US Gulf of Mexico Upstream Oil and Gas, with contributions from Justin Rostant, Principal Analyst, US Gulf of Mexico Upstream Oil and Gas, Fiona Piggott, Research Analyst, Jamie Thompson, Research Analyst, North Sea Upstream Oil and Gas, and Mark Oberstoetter, Director, Canada/Alaska Upstream Oil and Gas

The latest oil price crash comes at a time when the US Gulf of Mexico (GoM) is leaner and nimbler. It is better prepared to weather the storm compared to the last downturn. The region is resilient at low oil prices and nearly 82% of oil production has a short-run marginal cost of US$10/bbl Brent.

Additionally, over 60% of rig contracts are short-term which gives operators the flexibility to defer capex and maintain positive cashflow.

Although the US GoM remains afloat, budget cuts in the region have been swift, and some fields have been shut in due to the unprecedented low oil prices. Investment, exploration and project sanctions have all seen major recalibrations. We used Lens Upstream to highlight how US GoM operators have responded to the latest oil price crash.

Here are five key changes that we uncovered when we revised our Lens Upstream dataset to reflect the current reality

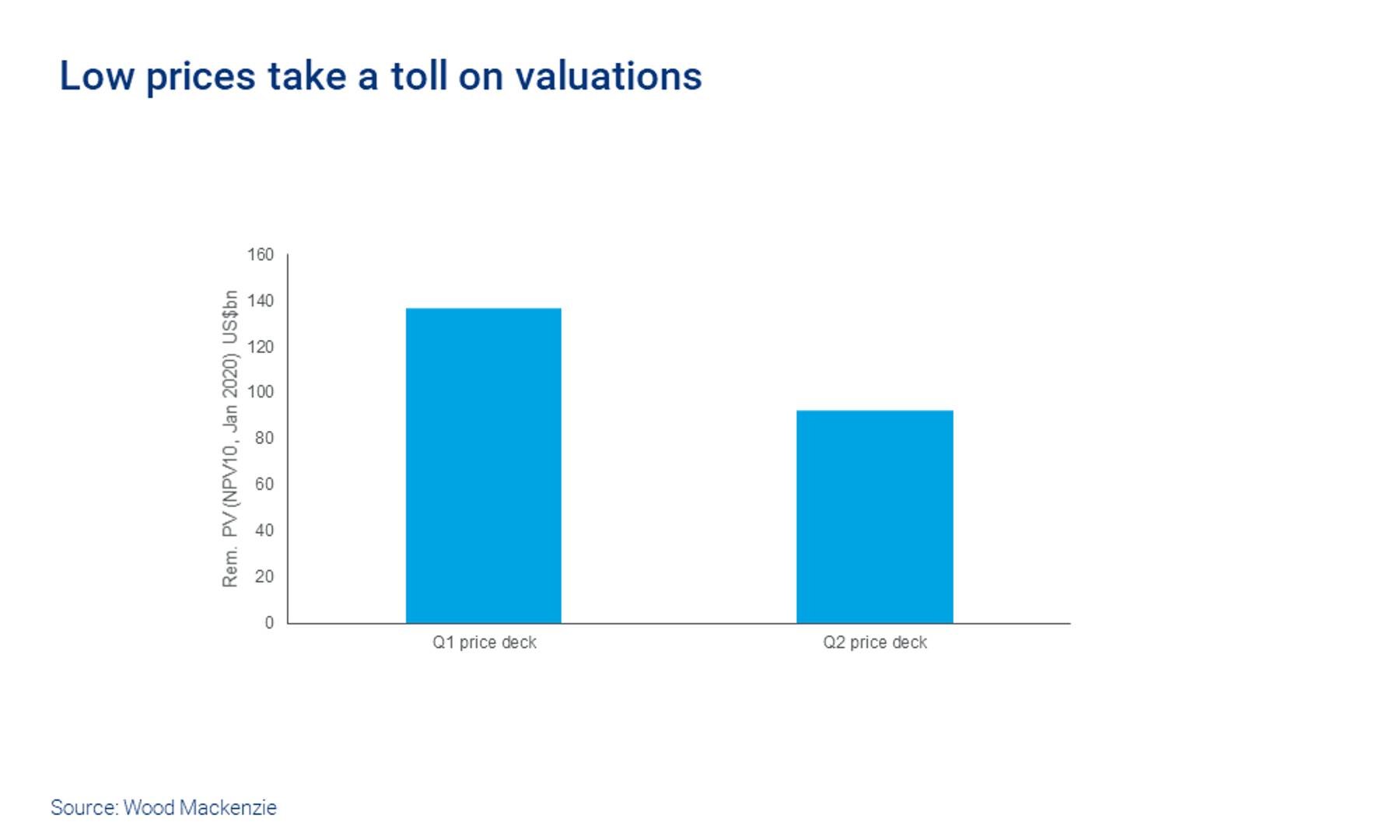

1. The decline in oil price has wiped off 30% of the remaining value from the US GoM deepwater asset base

In analysing the full impact of the downturn, we must isolate the effect of the fall in the oil price. We changed our long-term Brent oil price assumption from US$60/bbl to US$50/bbl and updated the 2020-2022 forward curve prices. This change alone, not accounting for changes to production or costs profiles on the assets, wiped off roughly 30% of the remaining value (NPV10, Jan 2020) from the US GoM deepwater asset base.

2. Roughly US$4 billion in investment has been cut from 2020, a 22% reduction from 2019

Depressed commodity prices have an obvious knock-on effect on corporate investment priorities. Taking into account dampened demand as a result of coronavirus and the initial lack of OPEC agreement, we expect capex to fall from our pre-Covid-19 projections by roughly 35% to US$7.4 billion. This represents a 22% decline from 2019 investment. Both the under-development and onstream opportunity sets have felt the pinch.

3. Production could decrease for the first time since 2013, but recovery awaits in 2021

The fall in investment caused us to revise our production outlook, as new projects, drilling campaigns, and brownfield phases have faced delays and potential changes of scope. At the start of the year, we predicted production of 2.2 mmboe/d – which would have been another production record in the US GoM. But our forecast has fallen by 200 kboe/d.

Recovery in production is expected in 2021. This is because near-term major project start dates have not shifted.

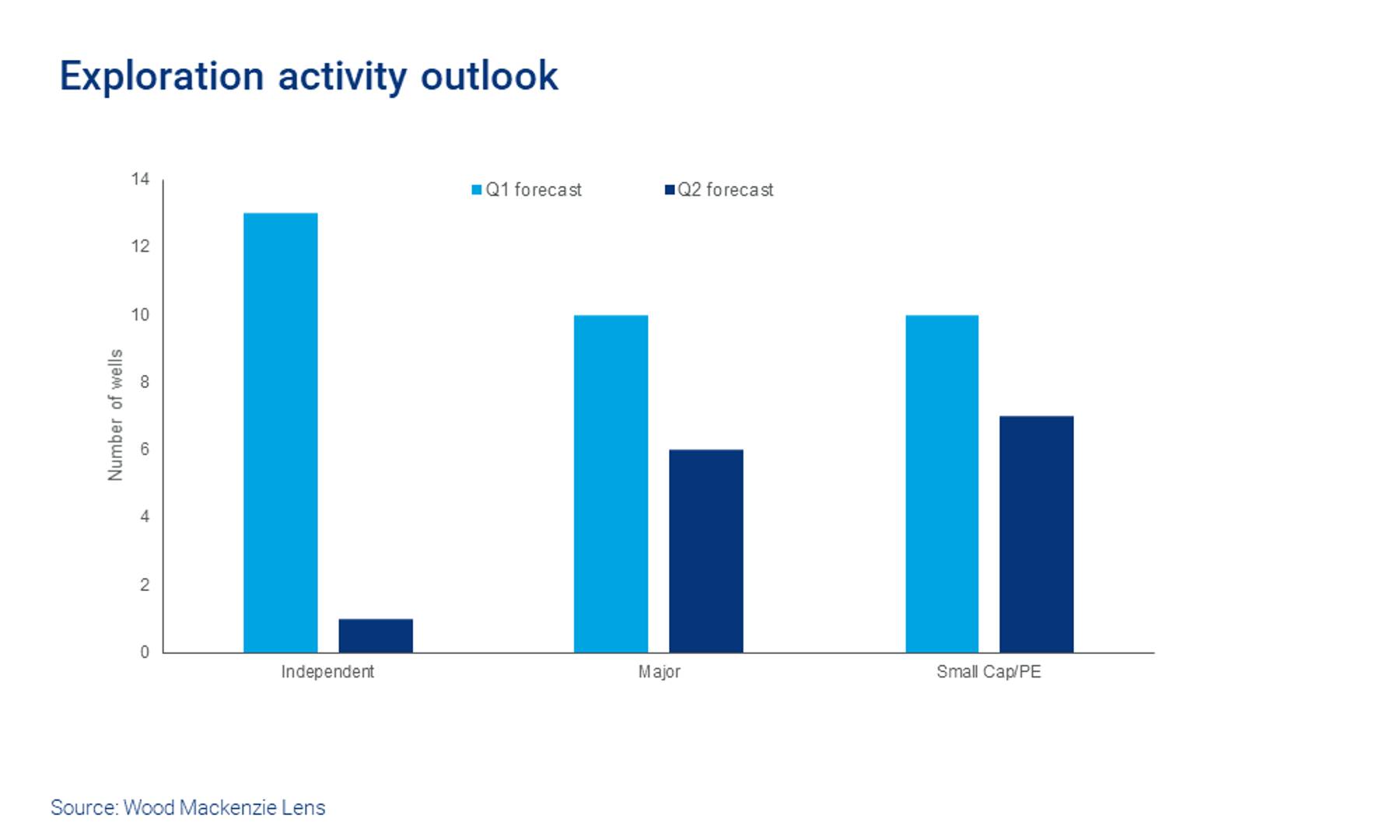

4. Exploration will fall to historic lows in 2020, and a rebound will take time

We were expecting exploration activity in 2020 to be on par with 2019, which was the first year that exploration saw an uptick in over three years. But in response to announced budget cuts, we have reduced our exploration forecast by 55% to 15 wells. This will be a historic low in the region and the recovery will be anything but quick.

The downward revision was largely dominated by Independents, while the Majors and small privates have forged ahead with exploration plans, albeit slightly scaled back.

{kind=link}

{kind=link}

5. No greenfield projects will be sanctioned in 2020 and subsea tie-back projects could struggle as well

Momentum was building in US GoM project sanctions and we expected a new record in 2020 with three greenfield projects requiring total investment of around US$10 billion. But the oil price crash quickly halted FID plans globally due to the heightened risks. As a result, we do not expect any US GoM project to be sanctioned in 2020. But, unlike the last downturn, where some projects were cancelled, this time project FIDs have simply been deferred. This is attributed to the relatively competitive economics of the pre-FID projects in the region, which could come down even further with cost deflation.

After the crash – what's changed in the US Gulf of Mexico?

Purchase the full report in store and you’ll receive additional analysis of the companies operating in the US Gulf of Mexico, as well as the following data:

- Q1 and Q2 valuations

- Pre-coronavirus and revised capex forecast out to 2026

- Production forecast out to 2030

- Cashflow and exploration spend by company

- And more