As politicians bicker, Australia’s energy and natural resources exports to China are booming

Despite increasing rhetoric, mutual benefit should ensure Chinese demand for Australian iron ore, coal and LNG remains strong

1 minute read

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

Latest articles by Gavin

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

Opinion

Why US Henry Hub natural gas prices are set to rise | Webinar replay

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

Sino-Australian diplomatic relations are spiralling downward. Already deteriorating prior to the pandemic, Canberra’s calls for an independent international inquiry into the origins of Covid-19 provoked an angry response from China. A recent editorial in the state-run Global Times newspaper called the dispute “…an all-out crusade against China and Chinese culture, led by Australia”.

This matters. Australia’s export trade with China is huge. By value, China currently buys around a third of everything Australia exports and the ongoing diplomatic bust-up risks spilling over into trade. Chinese media are discussing boycotts of Australian goods. Import bans and tariffs have been mooted on products like beef and wine. China’s ambassador suggested Chinese tourists and students may have “second thoughts” about choosing Australia.

None of this would be welcome. But the appetite of China’s consumers for Aussie tenderloin and Merlot is insignificant in terms of overall trade. Iron ore, coal and LNG are what really matter. How might these sectors be impacted and what could this mean for supply and prices?

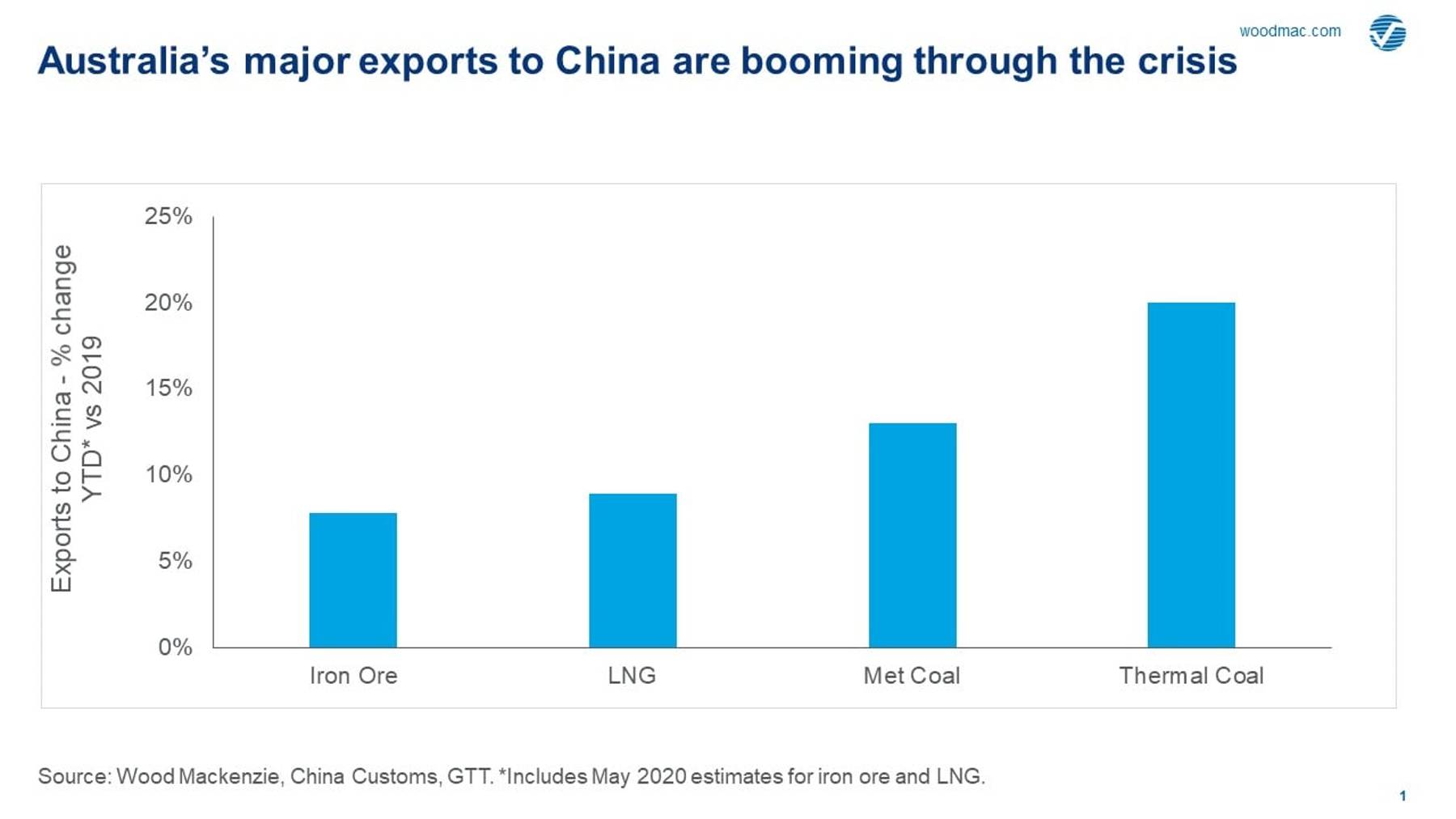

Australia’s ‘Big 3’ exports to China are surging

Despite the increasing war of words, Australia’s energy and natural resources exporters are in over-drive. As China recovers from the pandemic, demand for Australian iron ore, coal and LNG is booming – iron ore and LNG imports are up 8% and 9% year-to-date respectively versus 2019. Chinese imports of Australian coal are way ahead of where they were before the pandemic.

{kind=link}

Could relations deteriorate to the extent that demand for these commodities is damaged? It’s possible. Placing tariffs, quotas or other restrictions on Australian iron ore, for example, would be the clearest signal that China is no longer prepared to tolerate what it sees as Australian political interference. Recent talk of import restrictions and quotas on Australian coal, while nothing new, has also resurfaced over the past few weeks.

Depending on their extent and duration, the impact of any such measures on Australian producers – as well as on the country’s public finances - could be severe. But such a move would also come at a cost to China. Any disruption to its imports of Australian energy and iron ore would have an immediate impact on both price and China’s own supply needs. Longer term, the damage to strong existing trade relations could be irreparable.

Australian iron ore still critical to China’s economy

China depends highly on Australian iron ore. Around two thirds of its imports come from Australia, with this supply making up half of all iron ore consumed in China. Placing restrictions on Australian iron ore imports would hurt domestic steel producers just as the Chinese government is directing stimulus money into construction and infrastructure.

Diversifying supply away from Australia will also be challenging. Brazilian iron ore output remains disrupted by coronavirus plus wet weather and the fallout from last year’s Brumadinho dam disaster. We are forecasting a further 4% fall in Brazilian exports this year following a 13% fall in 2019. The halting of the Itabira complex last week as Vale strengthens Covid-19 controls highlights the downside risk. India, Russia and South Africa have increased exports, but only marginally.

Hence, no disruption yet to Australia-China iron ore trade. Right now, Australian miners are operating at capacity and struggling to increase output. This is due to infrastructure and capacity constraints, not because of Covid-19 or trade barriers. China did amend some iron ore import screening regulations at the start of June, introducing regulations that could be used to target Australian iron ore. But given constraints on Brazilian supply I don’t expect this is the intention of these regulations. The market seems to agree: Fortescue’s share price is at a record high, while BHP and Rio Tinto are both trading back at broadly pre-pandemic levels.

Read more: Global iron ore short-term outlook May 2020

A more mixed picture for coal

Coal may be different. With China way more self-sufficient in coal, punitive actions against Australian coal would be less damaging for power generators and steel mills. Plus, coal production is far more critical to the Chinese economy than iron ore mining, and efforts to restrict coal imports support domestic mining activity.

But this is yet to show up in the numbers for metallurgical coal imports. Seaborne imports in the first four months of 2020 were 28 Mt, already more than half of the 52 Mt imported for the whole of 2019. Met coal imports are over 80% Australian sourced, and while being only a fraction of total demand, coastal Chinese steel mills rely heavily on Australia’s high-quality low volatile, low-sulphur premium hard coking coals (HCCs). And don’t overlook the arbitrage. Prices for the best HCCs from Australia are around US$116/t CFR (delivered) today: similar domestic coals cost around US$163/t. If anything, concerns over import quotas have pushed down seaborne prices, making Australian supply more attractive.

Australian thermal coal faces greater risk. Chinese buyers have been largely absent in the Australian high ash market since last month’s ‘Two Sessions’, particularly government-owned buyers. Their absence is too recent to show up in trade figures but could have an impact if it continues.

LNG exports remain on a stable footing

As China first began to battle the coronavirus outbreak at the beginning of the year, LNG imports looked immediately vulnerable. Strong oil prices ensured that contract prices stayed high and PetroChina and CNOOC reportedly declared force majeure on contracted LNG cargoes.

But the worst never happened. LNG imports through May this year were up almost 9% on the same period in 2019 as demand has recovered and Central Asian piped imports have fallen. Low spot prices are also helping. Australia’s market share slipped slightly in May (ironically dented by rising imports from the US), but still accounted for around half of all LNG imports. Moves against Australian LNG look an unlikely prospect given the scale and contracts in place.

Read more: Global LNG demand faces first seasonal contraction in 8 years

Cool heads, dialogue and pragmatism

Trade disputes rarely end well. They are a zero-sum game, nobody wins. Australia and China both benefit hugely from their well-established trade in iron ore, coal and LNG. Australia has a large share of these import markets in China precisely because it is a reliable, competitive and trusted partner. All relationships go through their bad patches, but both sides would likely be worse off if the current diplomatic spat were to escalate further. Now is the time for cool heads, dialogue and pragmatism to prevail.

APAC Energy Buzz is a blog by Wood Mackenzie Asia Pacific Vice Chair, Gavin Thompson. In his blog, Gavin shares the sights and sounds of what’s trending in the region and what’s weighing on business leaders’ minds.