As US LNG cancellations kick in, Asian buyers are sticking to the script, for now

The economics of US LNG have worsened as global prices have fallen, but most buyers in APAC have yet to cancel US cargoes

1 minute read

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

Latest articles by Gavin

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

Opinion

Why US Henry Hub natural gas prices are set to rise | Webinar replay

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

Companies across Asia Pacific helped underpin the phenomenal growth of US LNG export capacity. Attracted by an alternative to oil-indexed pricing and US LNG’s inherent flexibility, Asian LNG buyers hold over 28 mmtpa of tolling agreements and capacity sold under SPAs with producing projects. Japanese utilities and trading houses alone account for around half of this volume.

But the global gas market today looks vastly different to when these contracts were signed. The economic chaos wrought by the coronavirus lockdown has cratered demand and worsened the LNG oversupply, pushing global gas prices even lower. Over the past month, European spot prices have traded below Henry Hub. The great LNG pushback has started and US supply is out of money. What does this mean for Asian buyers?

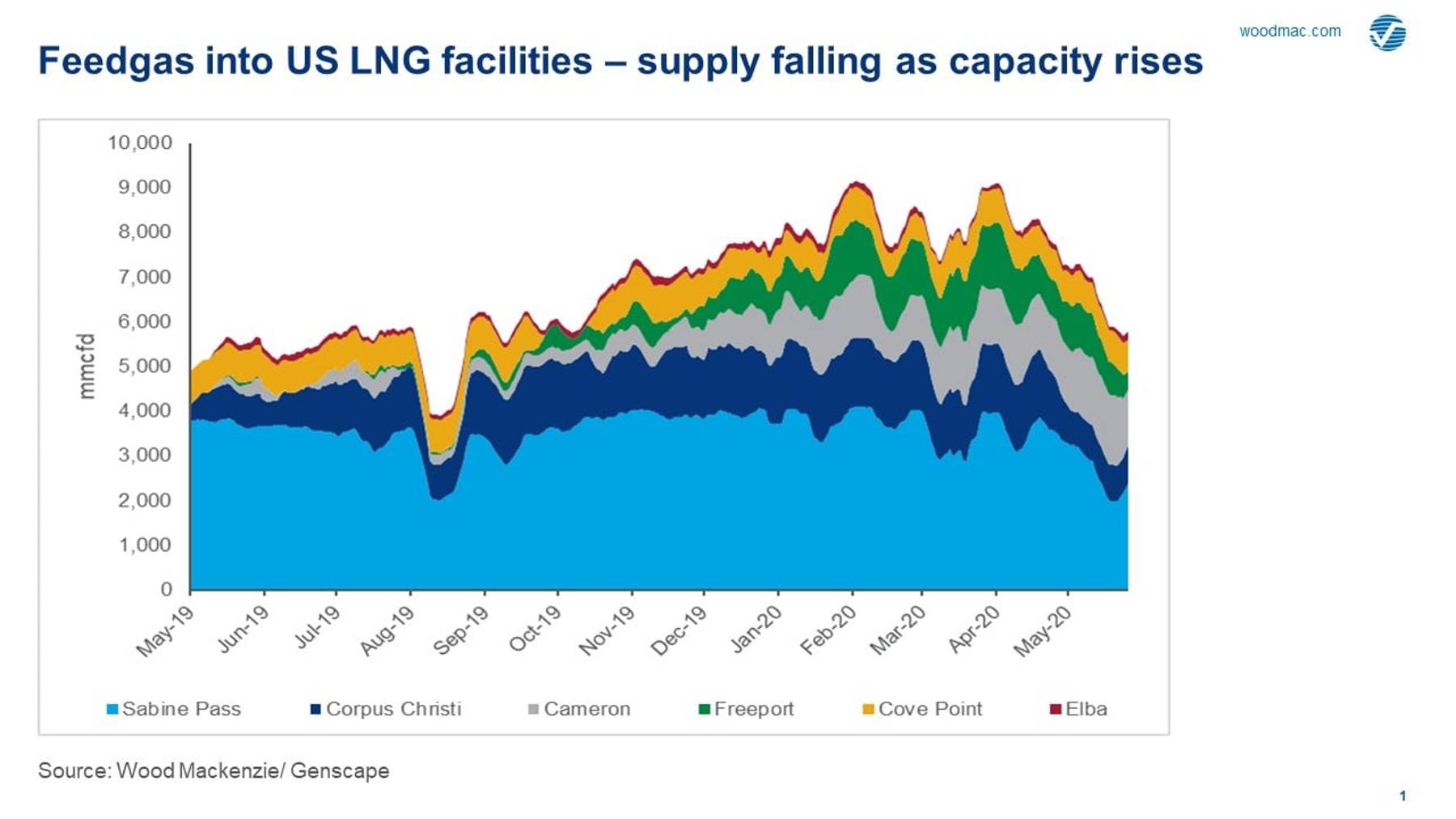

US LNG supply bracing for reduced output

Off the back of exceptionally strong winter utilisation rates, US LNG feedgas levels have been falling since early April. This comes even as new capacity at Freeport and Elba has entered service, and commissioning has begun at Cameron Train 3. Sabine Pass, Corpus Christi and Freeport have been most impacted to date.

Long anticipated by the market – and long feared by project participants – multiple US LNG cargoes are now being cancelled as margins turn negative. At least 20 cargoes scheduled for June loading will now no longer be lifted. My colleagues at Genscape have reported a major fall-off in feedgas into US projects as we enter June, with May closing out at 6 bcfd and June starting 2 bcfd lower at 4 bcfd. US LNG is today operating at below 50% capacity.

Are the cracks starting to show for Asian buyers?

Looking across all buyers of US LNG, Alex Munton, principal analyst with our Americas LNG team, believes that offtake by Asian buyers looks relatively secure, for now. According to Alex, “many are onselling on a DES basis into Asian markets and so able to better pass through costs. Meanwhile, some can also use US LNG volumes to meet portfolio commitments.” Right now, the greater risk is from the European Majors and utilities. While much of their offtake has been contracted to European customers, including to those without cancellation rights, other volumes remain unsold.

Feedgas data into the tolling projects supports this. Although Freeport output is currently down, other facilities where capacity is held by Asian buyers – Cove Point and Cameron – are now running at higher utilisation than Sabine Pass and Corpus Christi, where several European utilities as well as Shell and Total hold two-thirds of capacity sold under SPAs.

Given this, I would expect to be seeing rising volumes of US LNG coming into Asia. But shipping data shows that right now more output from the US is going into Europe than Asia.

{kind=link}

{kind=link}

There is no doubt Asian gas markets are weak, but might this also suggest that Asian US LNG project participants are struggling with feedgas and other contractual commitments through the crisis? High utilisation of tolling capacity could reflect a lack of flexibility in feedgas procurement, rather than an appetite to continue placing cargoes into the market. Similarly, existing shipping and logistics contracts may also be making it more challenging for Asian buyers to curtail offtake.

Deliveries into Europe by Asian offtakers must be resulting in negative margins. European offtakers have been quicker to respond. With more time to adjust their operations, it’s likely that we could see some Asian buyers making similar announcements around curtailing exports.

But let’s look for the positives

There are reasons to remain positive on the ability of Asian buyers to continue to utilise a large proportion of their contractual capacity. As discussed, Japanese tolling contracts at Freeport and Cameron are underpinned by volumes onsold on a DES basis into Asia. And the likes of Mitsui and Mitsubishi can place US LNG volumes into portfolio.

You might be interested in: 2020 Wood Mackenzie Japan Gas Series Webinar

For KOGAS, cancellation risk for volumes under its SPA with Cheniere is low. In addition to volumes already onsold to Total, with South Korean wholesale gas prices set by the its weighted average cost of gas, KOGAS can pass through its SPA costs. GAIL’s SPA with Cheniere is 100% take-or-pay, posing minimal cancellation risk. The company has already successfully onsold a significant volume of its 3.5 mmtpa contract.

Read also: Is the scene set for coal-to-gas switching in Japan and South Korea?

Among the remaining buyers, PERTAMINA and Woodside have both onsold portions of their Corpus Christi volumes. Pavilion Energy notably cancelled a US cargo in November last year.

Perhaps most encouraging (and surprising) has been the re-emergence of China as a buyer of US LNG. Chinese buyers took 10 US cargoes in April and May, having taken none over the previous 12 months. China is currently holding up APAC deliveries of US LNG. Will this continue given the souring political relationship? Hard to say, but worth noting that none of the recent cargoes were a part of the existing Cheniere deal with CNPC.

Unlike during previous downturns, Asian demand growth won’t be coming to the rescue of global LNG supply – not this summer at least. Indeed, we now expect a repeat of current US capacity under-utilisation during summer 2021. But this could change. If economic recovery and low spot prices support demand response going into winter, then a price correction could begin earlier than previously anticipated.

But for now, Asian buyers must now adapt fast to the current market. Cancellations of some of their US cargoes are increasingly possible this summer, and potentially next.

APAC Energy Buzz is a blog by Wood Mackenzie Asia Pacific Vice Chair, Gavin Thompson. In his blog, Gavin shares the sights and sounds of what’s trending in the region and what’s weighing on business leaders’ minds.