Discuss your challenges with our solutions experts

Beyond Germany: what the Netherlands and Belgium teach us about European battery economics

Europe’s utility-scale battery storage market is no longer a story about a handful of pioneering markets

1 minute read

Alex Cipolla

Senior Research Analyst, Energy Storage

Alex Cipolla

Senior Research Analyst, Energy Storage

Alex specialises in European storage markets

Latest articles by Alex

View Alex Cipolla's full profileEurope’s utility-scale battery storage market is no longer a story about a handful of pioneering markets. It is becoming a continent-wide investment class, and the analytical standards required to navigate it are rising accordingly. Wood Mackenzie has expanded its battery revenue forecasting coverage to include the Netherlands and Belgium, adding them to our existing suite covering Germany, Spain and France.

Alongside this expansion, we published a battery revenue benchmark, an independent reference point for what batteries actually earned across different configurations, market conditions and operating strategies, now covering six markets with the goal of doubling that coverage by the end of the year. In a market where revenue assumptions underpin billions of euros of investment decisions, the ability to validate methodology against real performance is not a footnote. It is the foundation.

Two markets, one shared challenge

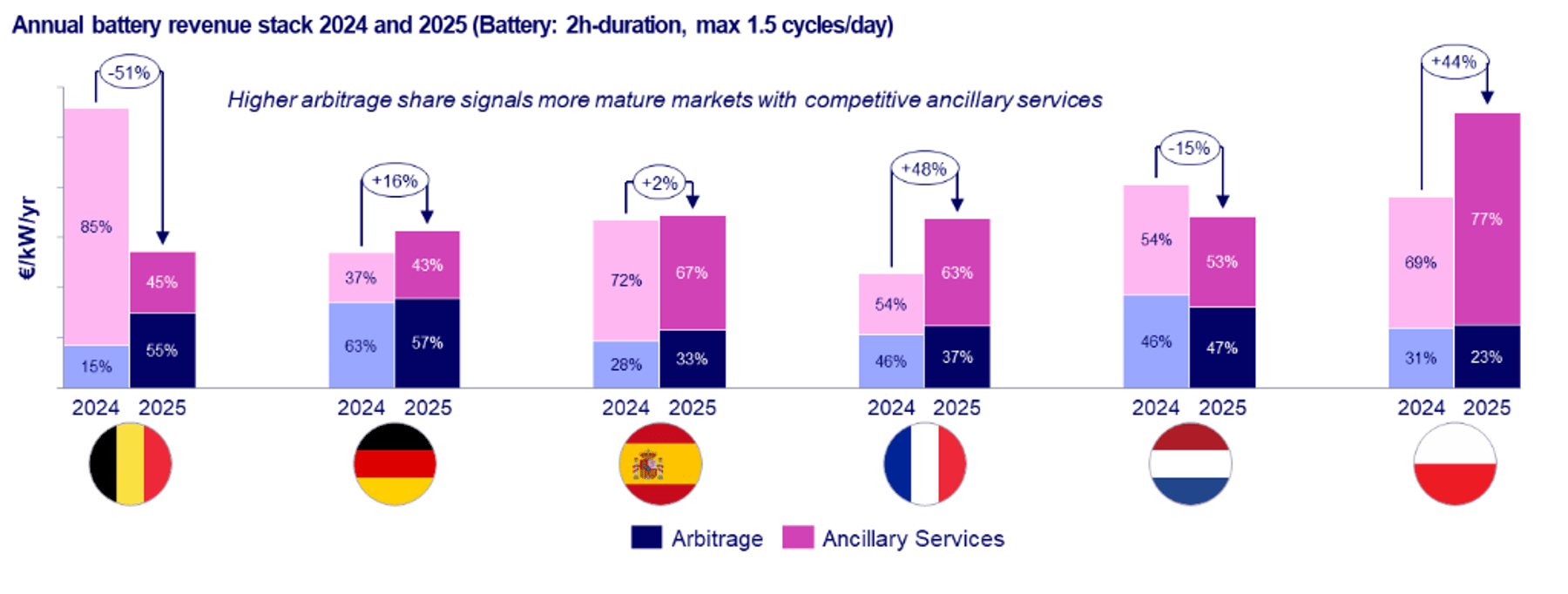

The Netherlands and Belgium are similar in size and geography and yet when it comes to battery storage, they tell quite different stories. Their grid fee structures differ, their regulatory philosophies diverge, and on capacity markets, Belgium has a well-established mechanism while the Netherlands has none at all. And yet both markets are navigating the same underlying transition: the era of ancillary-led battery revenue is ending, faster than many developers wished.

FCR and aFRR markets in both countries have experienced sharp revenue declines, as shown by the revenue benchmark. The mechanism is the same one visible in Great Britain and increasingly across the continent: as battery capacity scales, competitive pressure on ancillary services intensifies, prices fall, and the revenue stack rebalances toward energy arbitrage. In the Netherlands and Belgium, arbitrage now represents the dominant share of projected lifetime revenues, and that share will only grow through the 2030s.

What distinguishes the two markets is not the direction of travel. Both are converging toward the same destination: arbitrage as the dominant revenue source, capex deflation providing a meaningful tailwind, and the 4-hour configuration emerging as the strongest performer. What sets them apart is the starting point and the regulatory environment that either cushions or amplifies that transition.

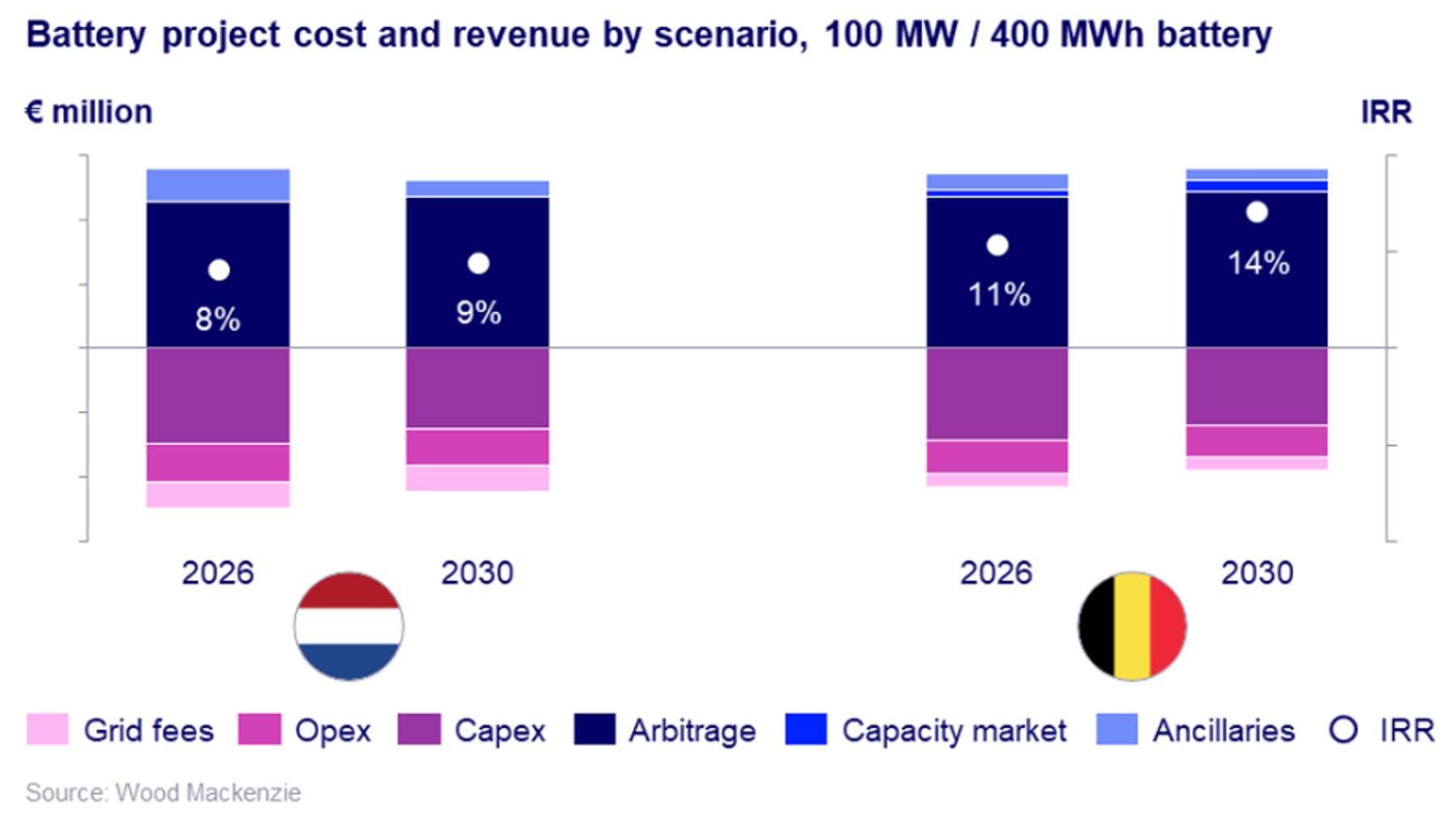

Belgium enters this period from a position of relative strength. A well-established capacity market mechanism provides a meaningful revenue layer on top of merchant revenues, and transmission-connected assets currently benefit from a 10-year grid fee exemption that materially improves project economics. The result is that Belgium presents one of the more compelling utility-scale BESS investment cases in Europe today, with returns remaining resilient even under stress scenarios. The key risk is not the market itself, it is regulatory: the current fee exemption will likely not persist, and timing investment around that uncertainty is one of the most important decisions facing developers in this market.

The Netherlands tells a more constrained story. The structural case for storage is strong, high VRE penetration, persistent grid congestion, and rapidly growing power price volatility all points to sustained demand for flexible assets. But the commercial viability of projects is highly sensitive to grid connection fees, which remain among the most significant cost items in the Dutch project stack. Recent regulatory reforms have introduced more flexible connection structures, and new congestion management revenue streams are beginning to emerge, but the margin for error remains narrow. The 4-hour configuration stands out as the strongest performer in both markets, and the dynamics of duration, cycling and fee exposure are closely interrelated.

The Netherlands tells a more constrained story. The structural case for storage is strong: high VRE penetration, persistent grid congestion, and rapidly growing power price volatility all point to sustained demand for flexible assets, fundamentals that rival Germany's, and in some respects surpass them. But grid connection fees transform that potential into a frustrating gap. Depending on the scenario, Dutch projects lose between 5 and 10 percentage points of IRR relative to their German counterpart, a drag that turns what would be an attractive investment case into a marginal one. Recent regulatory reforms have introduced more flexible connection structures, and new congestion management revenue streams are beginning to emerge, but the margin for error remains narrow.

{kind=link}

{kind=link}

Why our forecasts are different

Producing a credible battery revenue forecast requires more than assembling a revenue stack and stress-testing a financial model. It requires getting the inputs right, and that means having access to the right expertise across the full value chain. Wood Mackenzie’s battery revenue forecasting is built on the integration of three analytical capabilities that few organisations can bring together under one roof.

On the cost side, our dedicated supply chain team provides detailed battery system cost breakdowns and forward-looking deflation curves that feed directly into our financial models. Those cost forecasts are themselves informed by Wood Mackenzie’s metals and mining practice, which tracks and projects the prices of the major input materials. This is proprietary view is grounded in a global commodities research capability that spans the full upstream supply chain.

On the revenue side, our power market team produces the price and volume forecasts for every revenue pool we model, wholesale market, FCR, aFRR, and capacity markets. These are not isolated price series. They are the output of a fully integrated power market model that incorporates the build-out trajectories of wind, solar and storage alongside gas, coal and carbon price forecasts from what is widely regarded as the most established gas market research team in the industry. When we model how ancillary prices evolve as BESS capacity scales, we are doing so within a framework that reflects the full competitive dynamics of the market not a simplified extrapolation.

On the asset side, our battery storage specialists bring the technical depth required to model how batteries perform over the project life. Degradation curves, round-trip efficiency, depth of discharge constraints, availability factors, cycling limits, these are not footnotes in our model. They are central inputs that determine the gap between a theoretical revenue ceiling and what an asset will actually earn in practice.

Many revenue forecasts in this market are, in effect, optimistic by construction. They model each revenue stream in isolation, at maximum participation, without accounting for the operational constraints that govern real-world dispatch or the competitive depth of the markets being accessed. Our forecasts are built differently. They reflect the fact that a battery cannot simultaneously optimise across every value pool, that ancillary markets have volume limits, and that cycling strategies involve genuine trade-offs between short-term revenue and long-term asset health.

Beyond the baseline: How our interactive tool fills the gaps

In current market structures, battery projects’ final output varies enormously in their technical configuration, financing structure, grid connection terms and commercial strategy and the economics are sensitive to all of these variables in ways that a fixed set of cases cannot fully capture.

For clients who need to go further, Wood Mackenzie has developed an interactive financial modelling tool that allows users to explore their own assumptions across the full range of technical and financial parameters, duration, cycling regime, degradation profile, capex variance, grid fee scenarios, capacity market participation and more. The tool draws on the same underlying models and data that power this report, and is designed to support the kind of iterative, scenario-based analysis that investment decisions in this market genuinely require.

To learn more about Wood Mackenzie’s battery revenue forecasting coverage across Europe, or to discuss how our analysis and interactive tool can support your investment process, please contact Alex Cipolla at alex.cipolla@woodmac.com or reach the EMEA Energy Storage team directly.