Discuss your challenges with our solutions experts

Can Russia continue to keep pace with Europe's LNG demand?

The answer lies with Europe's true pipeline capacity

1 minute read

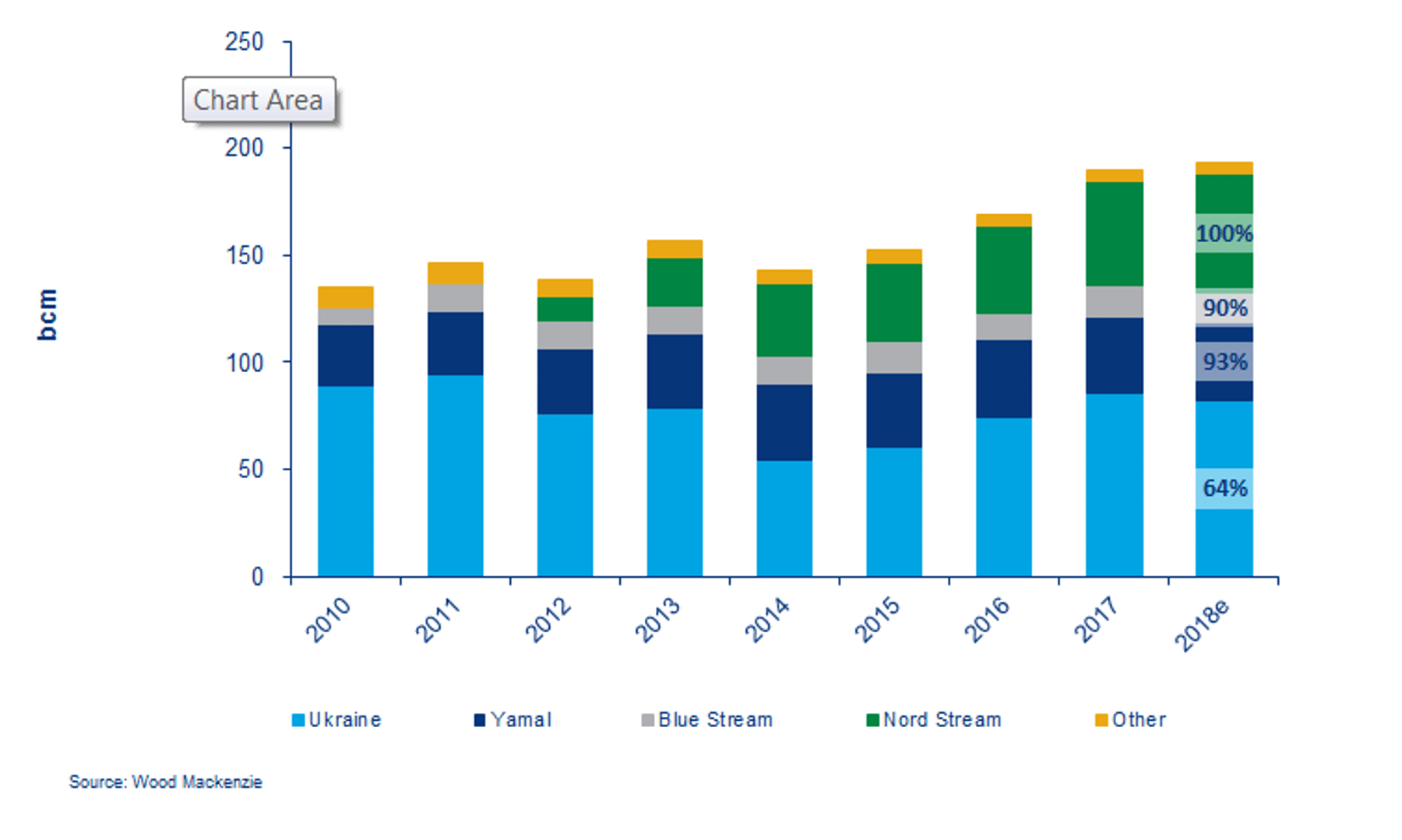

This year, Russia is on target to deliver 200 billion cubic metres (bcm) of piped gas into Europe, a figure which meets close to 40% of the region’s gas demand.

But Europe’s import requirements are growing – Wood Mackenzie estimates it will need a further 77 bcm per annum by 2025 – and there are doubts Russia’s export capacity will be able to keep pace.

The problem isn’t that Russia doesn’t have the capacity or volumes to export, it’s that infrastructure bottlenecks in Europe will limit Russia's export capacity, forcing European consumers to turn to LNG.

Wood Mackenzie believes Europe’s LNG requirements will more than double by 2025. Europe's growing gas import dependency, coupled with constraints on Russian pipeline exports, mean that LNG imports will have to increase.

What's the true capacity of available infrastructure?

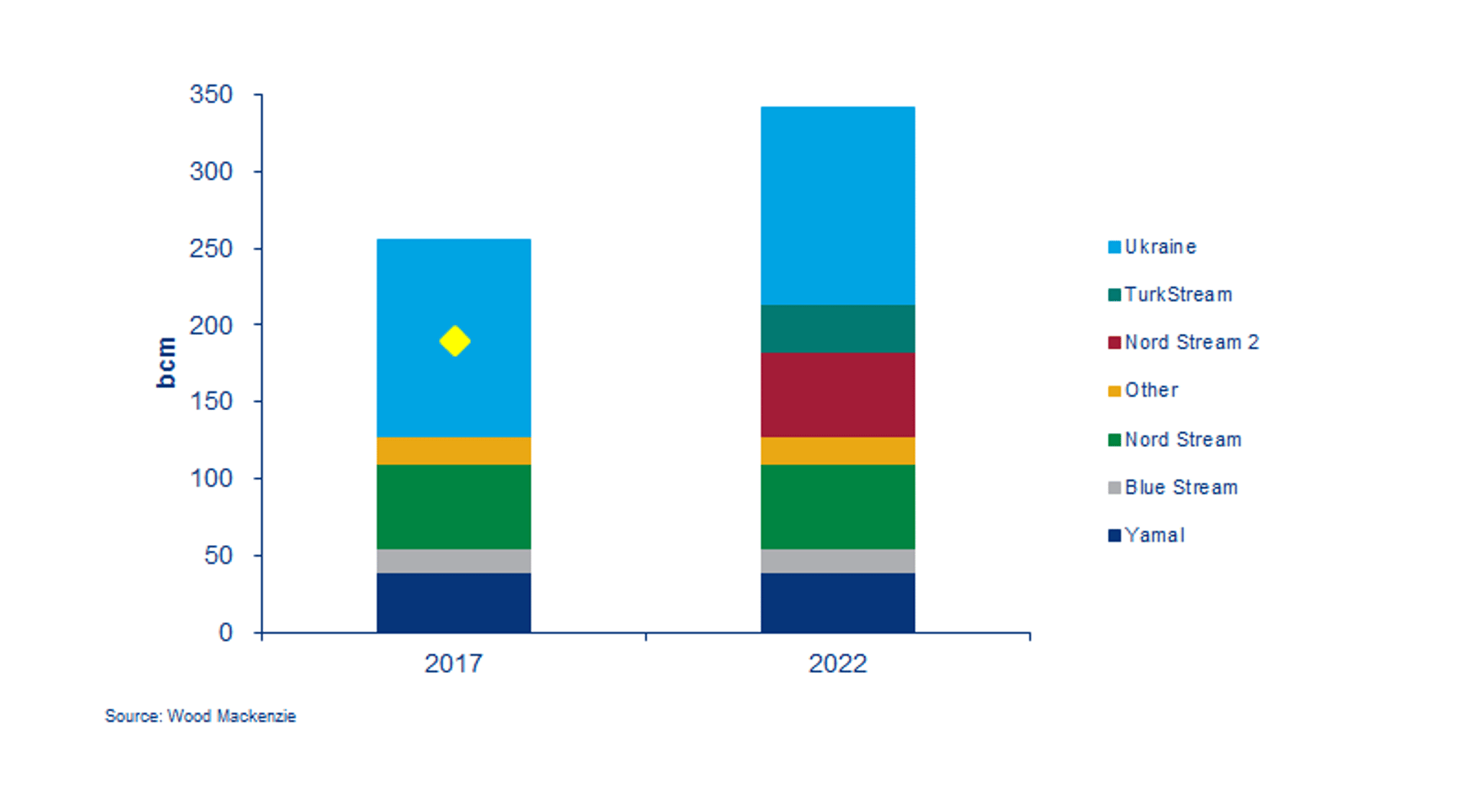

On the face of it, Russia is well positioned to further increase flows to Europe, given it has existing pipeline export capacity of 257 bcm per annum. And it has started construction of two major pipelines: Nord Stream 2 and TurkStream.

These two links could see Russia's pipeline export capacity to Europe reach 343 bcm per annum. But effectively, capacity to Europe will be much less, perhaps even as low as 235 bcm per annum.

Why is there such a gap between nameplate and effective capacity?

The difficulties start at Baumgarten. Because both Nord Stream 2 and Turkstream are designed to converge at the Austrian hub, there will be limited pipeline capacity at Baumgarten to deliver additional gas through Ukraine, even if Russia wanted to.

These capacity constraints will have an impact on all the export routes Russia uses to access European markets. While Russia currently has 257 bcm per annum of nameplate export capacity to Europe, effective capacity is around 220 bcm per annum assuming full use on the most direct routes. 128 bcm per annum of that is Ukraine transit capacity. Nord Stream 2 and TurkStream add 87 bcm per annum of capacity but these links will make use of existing European infrastructure, which then limits the volume of gas that can transit Ukraine to 20 bcm per annum. Consequently, overall Russian export capacity to Europe will only increase to 235 bcm per annum.”

Arguably, additional pipeline capacity could be built to overcome these bottlenecks. A new pipeline in Germany could better link Nord Stream 2 to northwest Europe, instead of directing the majority to Slovakia. Alternatively, Russia could choose to build additional pipeline strings on the Nord Stream or TurkStream routes to enable full diversification from Ukraine.

-

257 bcm per annum

Russia's existing nameplate pipeline capacity

-

220 bcm per annum

Russia's effective capacity

-

343 bcm per annum

Potential capacity including two new major pipelines

-

235 bcm per annum

Effective capacity may increase to this level

{kind=link}

{kind=link}

What does this mean for Europe?

For some time, northwest Europe has been regarded as the “sink” of the global LNG market. This might well be the case over the next two years as global LNG supply growth exceeds LNG demand growth in Asia, requiring Europe to absorb the excess supply.

But beyond 2020, northwest Europe will need to compete in the global market to secure LNG imports – and at a time when the flexibility of Russian gas imports will be limited.