How will the oil price crash affect the ethylene cost curve?

Changing oil price dynamics add an extra dimension to ethylene’s overcapacity outlook

1 minute read

The oil price saw its biggest fall in 30 years earlier this month. Brent crude oil dropped close to US$30/bbl, having spent most of this year at around US$60/bbl. This dramatic drop could have significant near-term and longer-term repercussions for global petrochemicals.

Ethylene holds a prestige position in the petrochemicals world. As the biggest commodity by both volume and value, it’s a key driver of the industry's growth, profitability and investment. Nonetheless, it is very much subject to supply-side forces from further up the energy value chain in upstream, refining, NGLs and coal – as well as the global macroeconomic forces that shape the consumption of its thermoplastic derivatives.

So, what could the oil price crash mean for ethylene?

This article includes highlights from the insight ‘The global ethylene cost curve in a $30/bbl world’. To read the insight in full, fill in the form for your complimentary copy.

Ethylene: overcapacity and uncertainty mean cost is critical

Our base case ethylene market outlook to 2025 can be summarised in one word – overcapacity. China, in particular, is poised for meteoric expansion over the next five years. The uncertainty caused by the coronavirus outbreak could exacerbate the overcapacity situation if demand growth underperforms our base case outlook.

Cost of production is critical for producers striving to remain competitive in this environment. And we expect the recent oil price drop to dramatically alter the shape of the global ethylene cash cost curve. Near-term, this could affect regional market and asset competitiveness. Longer-term, if low oil prices were to be sustained, it could alter structural investment in the ethylene industry.

What would a US$30/bbl oil price world mean for ethylene?

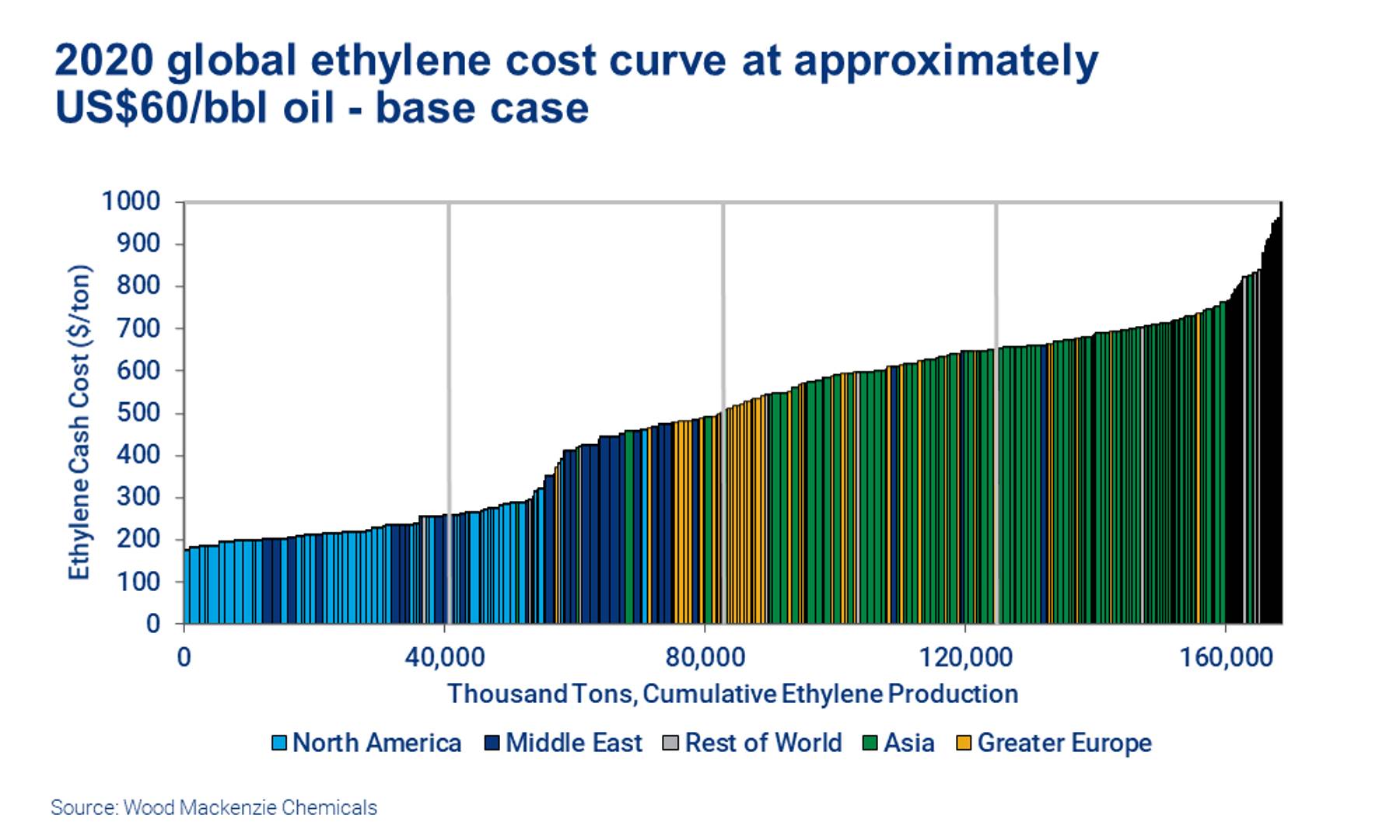

We have generated two ethylene cost curves to highlight the changes from an approximately US$60/bbl oil price environment to a US$30/bbl oil price world. The analysis is based on approximately 300 assets around the world, using our global ethylene asset cost tool.

You can see the US$60/bbl oil price chart below. To see the chart for our US$30/bbl oil scenario case, fill in the form for a complimentary copy of the full insight.

{kind=link}

Our research shows that a US$30/bbl oil price could have monumental impact. We’ve broken this down by quartile of global ethylene supply.

First quartile: losing its advantage

The first quartile of global ethylene supply is dominated by assets in North America and the Middle East, and largely tied to ethane feedstock.

In North America, ethane prices are already low and, to an extent, decoupled from the absolute oil price level – there’s little room for a further price drop. Similarly, pricing in the Middle East is generally set domestically at a fixed, low level.

The net effect is that this quartile is largely unchanged by a lower oil price. However, the advantage over the rest of the cost curve is significantly reduced.

Second quartile: a much more competitive position

The second quartile of global ethylene supply marks the general transition from gas-based production of ethylene to liquids/mixed feedstock. It’s primarily comprised of North American and Middle Eastern supply, but also supply from globally-competitive mixed feedstock steam crackers.

Global pricing of these heavier feedstocks tends to have a strong correlation with the prevailing crude oil price. A lower oil price environment would dramatically alter the shape of this supply, putting this quartile in a much more competitive position than in the base case view.

Third and fourth quartiles: a mixed picture

How would a lower oil price environment affect the third quartile supply – largely Greater European and Asian plants geared towards mixed feedstock/heavier cracking? And the fourth quartile – which includes coal-to-olefins (CTO) and methanol-to-olefins (MTO)?

The rapidly-evolving oil price dynamic has the potential to change regional and company fortunes considerably. To read about the impact across all four supply quartiles, fill in the form at the top of this page to access this complimentary insight in full.

Ethylene services: unique insight

Gain essential insight into supply/demand, capacity developments and price forecasts to understand today’s markets and tomorrow’s trends.