Is PetroChina really going green?

Asia’s largest oil and gas producer wants to be ‘near-zero’ emissions by 2050; but don’t expect radical change.

1 minute read

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

Latest articles by Gavin

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

Opinion

Why US Henry Hub natural gas prices are set to rise | Webinar replay

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

PetroChina has announced it is targeting ‘near-zero’ net emissions by 2050. The move is the first publicly confirmed (near) net-zero goal by an Asian national oil company, a recognition by one of the world’s largest producers that it must address carbon emissions and adapt to the energy transition. Specific spending targets have been released for low- and zero-carbon investments.

Almost inevitably, the announcement came with frustratingly little detail. To decipher what it means I spoke with Miaoru Huang, Senior Manager, China Gas Research, and Max Petrov, Principal Analyst, Corporate Research.

A serious move by PetroChina to reduce carbon emissions?

Miaoru: PetroChina is all about scale - the company produces 4.6 mmboe/d - so any effort to reduce emissions requires serious consideration. PetroChina has committed more than $33 billion of capex in 2020, after budget cuts. Diverting a proportion of this into new energy is an important step, even if small in percentage terms. New energy also provides PetroChina much needed growth opportunities.

This isn’t PetroChina’s first step in addressing the energy transition. Through its parent, CNPC, the company is already a member of the Oil and Gas Climate Initiative (OGCI). PetroChina may not be looking to emulate the full net-zero ambitions of some of the OGCI’s European members – and I expect it will only be addressing Scope 1 and 2 emissions - but it has placed itself ahead of many of its NOC peers.

Max: Let’s stick with scale. PetroChina is targeting US$0.4-0.7 billion per year between 2020-2025, rising to US$1.5 billion per year thereafter to invest in geothermal, solar, wind and hydrogen. Through to 2025, that’s only 1-2% of total spend.

Compare this with the European majors. Eni plans to spend over 20% of its total budget on renewables by 2023; for BP it will be 33% by 2030. I agree PetroChina has positioned itself amongst the leading NOCs on net emissions reductions, but others are showing greater ambition. With a notably more emissions-intensive portfolio, PETRONAS is seeking board approval for a net zero 2050 target. Both CNOOC Ltd and PETRONAS have announced more aggressive spend on renewables for 2020, closer to 5% or higher.

How can PetroChina achieve near-zero?

Max: Without more detail, it’s not clear! We assume that the company is targeting Scope 1 and 2 emissions, excluding the carbon footprint associated with end-user emissions (Scope 3). That means PetroChina is going to need to invest into clean energies significantly more than stated.

Gas will also have to play a critical role in decarbonisation. Oil declines fastest in PetroChina’s current production profile, reducing from around 57% in 2020 to only about a quarter by 2035. Gas production is broadly flat through to 2035, helping curb emissions. If the company can grow gas production at the expense of oil, near-zero looks in the bag. But this was the plan long before last week’s announcement.

If PetroChina sets its sights on reducing Scope 3 emissions, things get even more complicated. In such a scenario, the company would have to shrink its upstream operations, similar to announcements made by some European Majors. With an already mature portfolio, natural decline cuts PetroChina’s production levels by half by 2035. You could argue achieving near-zero never looked easier, but would the company and the government accept the trade off?

Miaoru: Don’t be too surprised by the lack of detail. This is standard for Chinese companies rather than any deliberate lack of transparency. Afterall, PetroChina is not a European Major and targets in China are often aspirational rather than firm commitments.

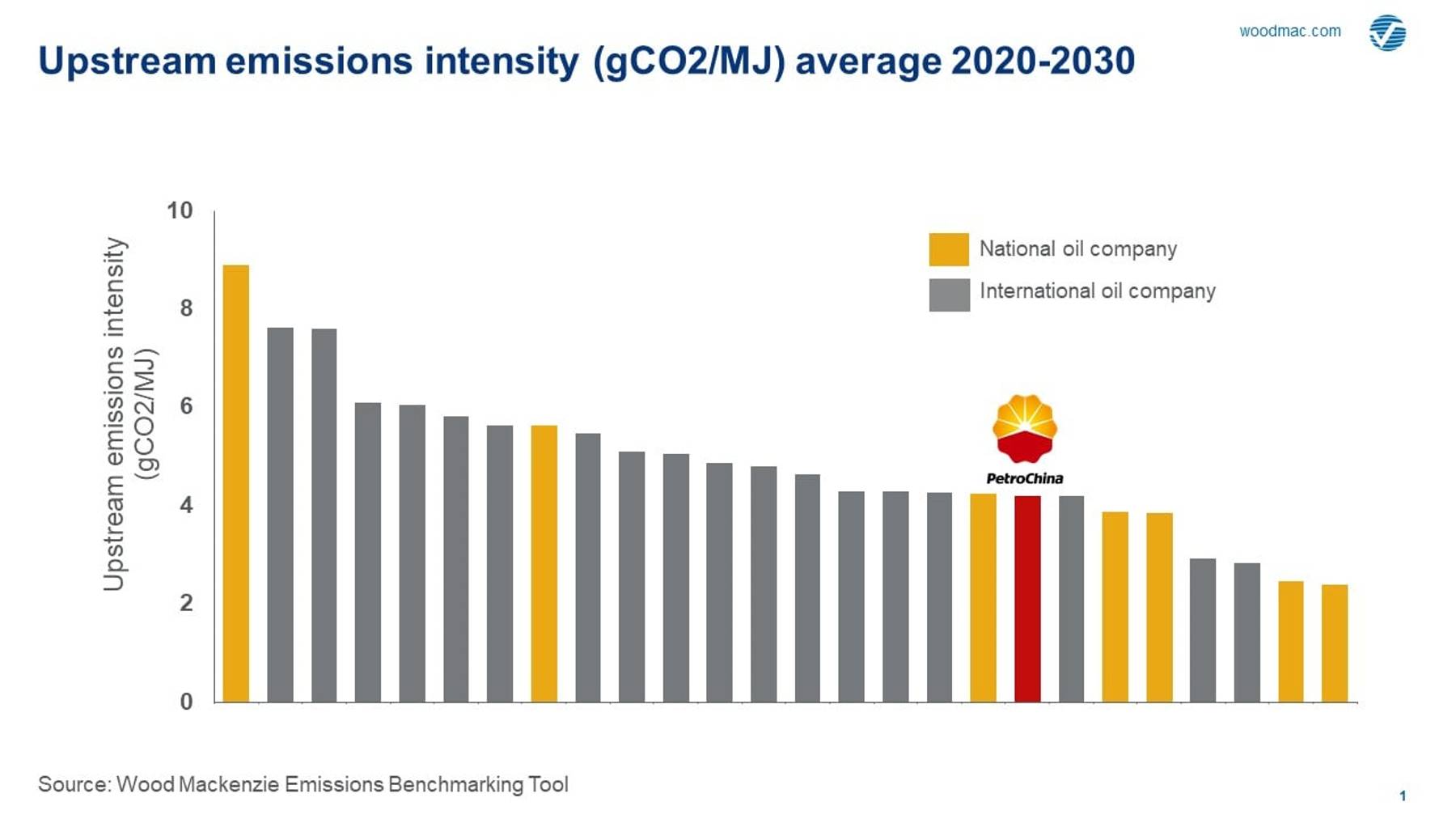

Looking at the current portfolio, PetroChina’s carbon emissions intensity is noticeably lower than many of its IOC and NOC peers. Production is predominantly onshore, with limited exposure to deepwater and LNG (though the latter is rising). Yes, this makes near-zero look more straightforward, but a ‘do nothing’ approach to reducing emissions isn’t on the cards. With President Xi’s push to expand domestic output and to grow overseas, PetroChina must look to boost output.

{kind=link}

How critical is gas to achieving PetroChina’s targets?

Max: Essential. PetroChina needs to continue to increase the share of gas – particularly domestic production – to meet growing demand. Tight gas and shale gas are critical. Yes, more capital will be allocated to new energies, but note the vague reference to this depending on progress in these sectors. Over the next five years at least, domestic gas will dominate.

Miaoru: I agree that gas is key, but I don’t fully discount the potential for investment in low-carbon and new energy options. During PetroChina’s recent H1 results call, management put major emphasis on its gas end-user business. The recent creation of PipeChina and the need to compete with city gas distributors will encourage PetroChina to invest more into integrated energy solutions, including new energy.

Read more: China unveils the extent of its gas ambitions

Can we expect more from China on climate change leadership?

Miaoru: The announcement gives an indication around China’s thinking on the energy transition and its broader role in climate change leadership. China worked hard to position itself as a driving force behind the 2016 Paris Agreement. Soft power matters. The leadership’s more recent re-focus on energy security has rolled back some of these efforts. China is stressing ‘clean coal’ as a dominant fuel while developing technologies and manufacturing capacity for low-carbon energy. But if China wants to drive the agenda in the future, its NOCs will also need to be climate leaders.

Max: I expect significant change in China’s policy only to the extent that the leadership will use next year’s 14th five-year plan to bolster existing policy initiatives and financial incentives for renewables and anti-pollution measures. Employment, education and the environment are the three main pillars of the next plan. Given current economic and geopolitical uncertainty, stability is critical.

What’s the bottom line - game changer or greenwashing?

Max: Some will label this greenwashing. I just don’t see PetroChina ready to embark on the kind of transformation that the likes of BP and Eni have announced. The company’s mandate remains firmly in oil and gas; E&P will continue to dominate the portfolio. Is PetroChina ready to transform its existing profitable businesses? Highly unlikely. But a lot can change in 30 years.

Miaoru: All oil and gas companies are facing pressure to reduce carbon emissions. And with its already low-carbon portfolio, lower emissions trajectory and future investment in gas, PetroChina was already on this path. Little may radically change in the short term. But this is China, any shift in gear by the government on carbon and things could move fast.

You might be interested in: PetroChina sets sights on carbon neutrality

APAC Energy Buzz is a blog by Wood Mackenzie Asia Pacific Vice Chair, Gavin Thompson. In his blog, Gavin shares the sights and sounds of what’s trending in the region and what’s weighing on business leaders’ minds.