Not made in China: the US$6 trillion cost of shifting the world’s clean-tech manufacturing hub

How can we balance the increased cost of diversifying energy transition critical supply chains against the economic and strategic risk of being wholly reliant on China? Pragmatically, how can the world’s biggest economies work together to achieve a successful energy transition?

4 minute read

Global supply chain issues compounded with Russia’s war on Ukraine and the painful dragging economic pressures from inflation and interest rate surges has raised these questions in policymakers’ minds.

China dominates clean tech

For a country to dominate in a technology space, one could simplify requirements into 1) the ability to produce high quality products; 2) at the scale the market needs; 3) at the most competitive prices. China has largely achieved this and in just over a decade.

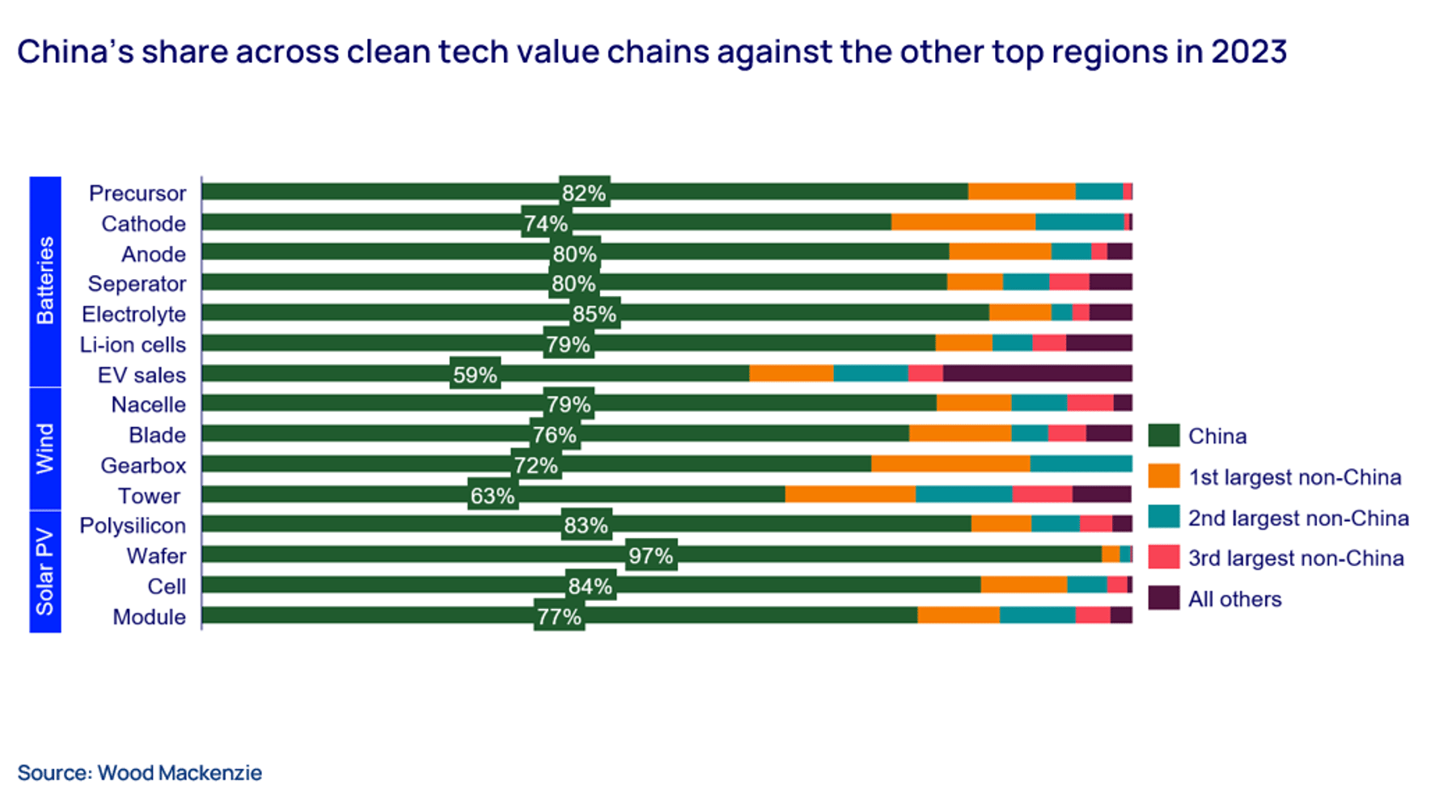

Firstly, it clearly dominates manufacturing capacity and capability across all key technologies, from a 60% share in wind foundations to a 97% share in solar PV wafers. We’ve added EV sales (which sits outside manufacturing but demonstrates dominance beyond manufacturing in a key asset class) for good measure.

Secondly, China-based manufacturers have achieved the lowest costs across these technologies; pricing at levels that are unapproachable for the major competing markets.

China is not just winning on technology costs. A decade ago, low-cost China products were commonly brushed off as mass produced and low quality. Not anymore. Performance data from operations show that best-in-class turbines, PV modules and battery cells are coming out of China, performing as well as the western incumbents.

How did China come to dominate?

In 2008, when the financial crisis hit, China introduced a goliath US$600 billion (RMB 4 trillion) stimulus package. Recognising the threat and opportunity posed by climate change, the package included generous subsidies for the clean-tech industry, such as solar manufacturing.

It also welcomed global leading manufacturers like GE, Siemens and Vestas, plus solar tech companies, to enter into major JVs in China through technology sharing and localisation agreements, to access the domestic market. This enabled key renewables industries to leapfrog the European and US market leaders at the time.

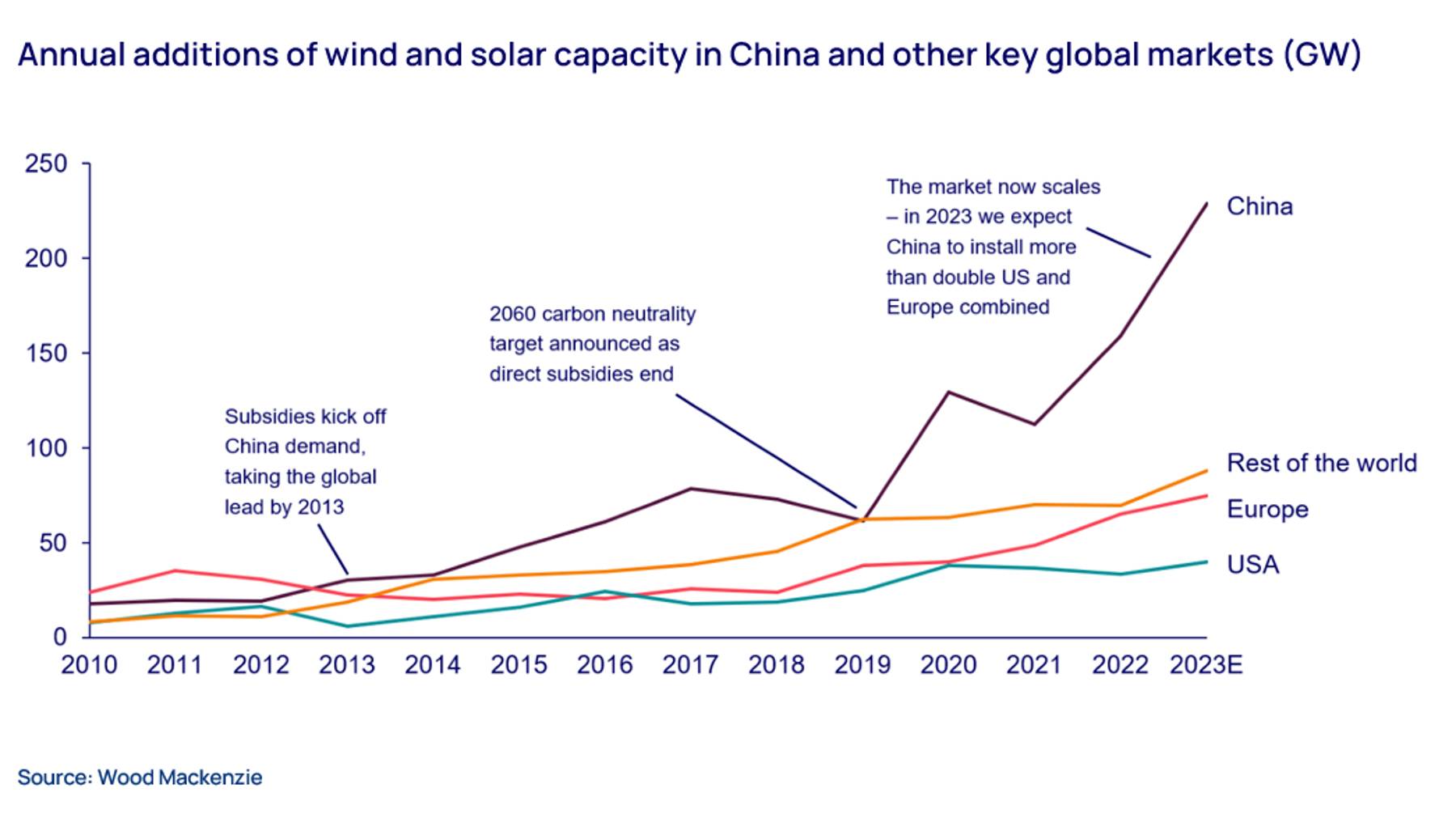

By 2013, China led global renewables installations

With such high internal market demand across wind, solar, energy storage and EVs, market pull policy has been withdrawn, with FiT subsidies ceasing in 2021. This coincided with China’s announcement that it would commit to peak emissions by 2030 and reach net zero by 2060, giving long term certainty to its mission: move to an electrified economy and away from energy security risk fossil fuels.

Whilst other markets are moderating renewables targets, Wood Mackenzie estimates China has installed 230 GW of wind and solar in 2023, more than double the US and Europe combined, with a capital investment value of US$140 billion.

What has been done to mitigate the risk of China’s dominance?

Policymakers in the US and Europe are now responding to the threat of China’s dominance in clean tech with an elevated priority.

The most recent, aggressive, and long term is the Inflation reduction act (IRA), passed into US law in 2022. It has introduced multiple policies and potential funding of US$41 billion to directly incentivise the re-shoring of manufacturing capacity, whilst penalising China imports with tariffs.

Europe’s response last year was the Net Zero Industry Act. It also introduces local content requirements to push back on single market imports.

Other notable and growing clean tech markets that have introduced local content policies include Brazil, India and Japan.

Note that China’s biggest clean tech manufacturers are now positioning facilities across key growth markets as a mitigation to these policies.

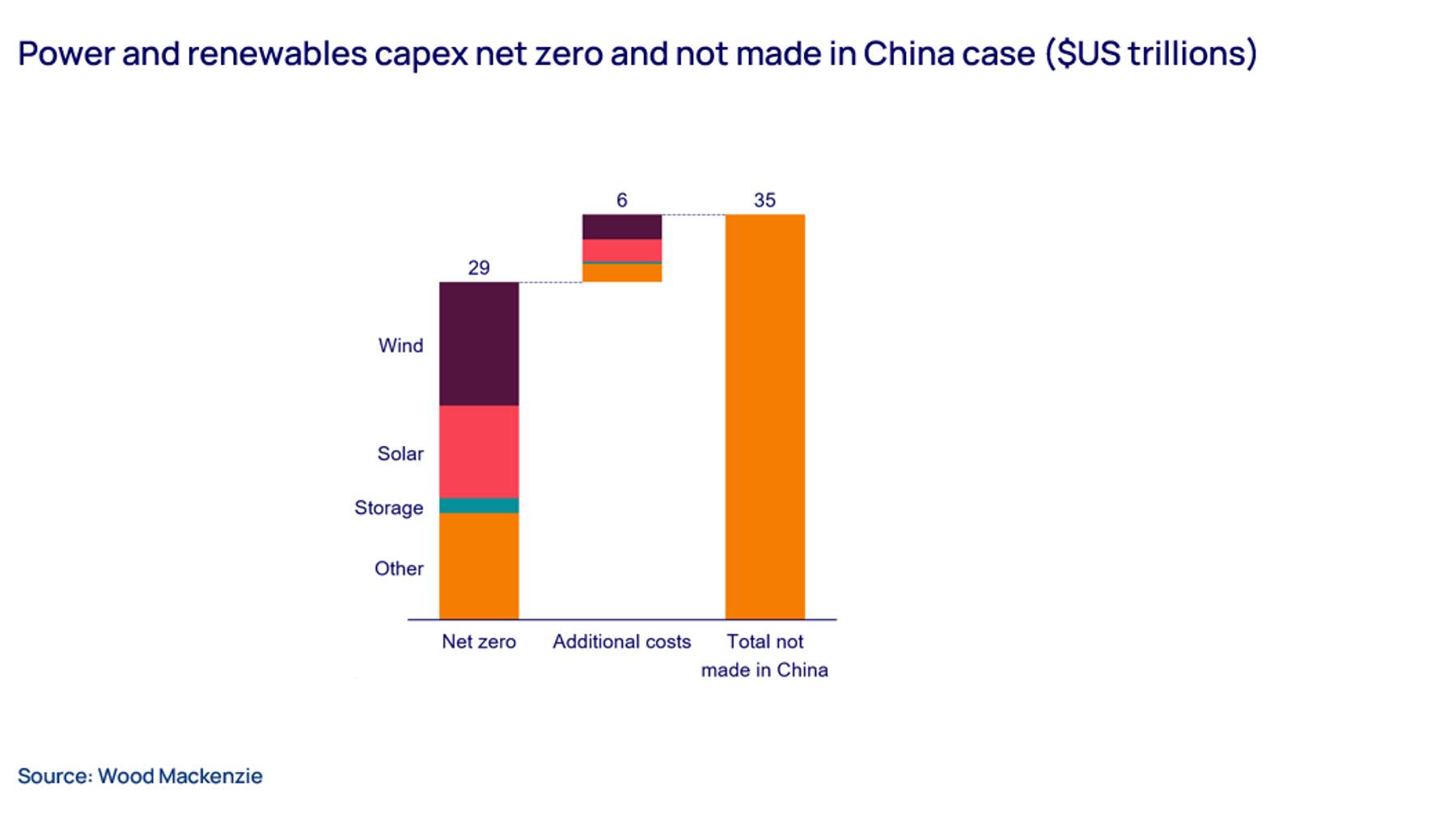

How much would the energy transition cost without China?

Currently the capital expenditure required for the energy transition across power and renewables for Wood Mackenzie’s net zero case is $US29 trillion between 2023 and 2050.

Consider the following scenario: the world’s markets embark on a project to rapidly rid China manufactured clean tech products from their market demand. The costs reflected in an increase across all clean-tech and other supporting power generation technology results in a 20% increase on overall capital expenditure on this key equipment alone.

That’s an increase of $US6 trillion in a ‘not made in China’ scenario.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Is the world prepared to pay for an energy transition not made in China or to miss climate targets?

The simple answer is no. The clean-tech world has achieved unimaginable scale and cost reduction in just over a decade. Solar costs have reduced 85%; a similar trend in batteries at 87%, and wind at 43%.

China’s clean-tech manufacturing capacity expansion has been at the heart of this story. Without China at the table, aggressive cost reductions we have become accustomed to are over.

Moreover, the length of time it would take to catch up to China’s production scale would push back a transition which is already running far behind schedule.

We expect a compromise to unfold, with a more palatable level of cost increases to develop. This compromise will provide opportunities for the world’s economies to capitalise on the growth opportunities alongside China.

A successful net zero global economy will only be possible through international collaboration

Success will only be possible through international collaboration, pragmatism, and innovation between the US, Europe, China and others. This will be essential to achieve the scale required at an optimum cost and value for all.