Discuss your challenges with our solutions experts

US distributed solar companies navigate economic headwinds

Innovation, product diversity and partnerships are driving resilience for publicly-traded distributed solar companies

3 minute read

Amanda Colombo

Research Analyst, US Solar

Amanda Colombo

Research Analyst, US Solar

Amanda’s areas of focus include commercial solar policy and public company financial landscape analyses.

View Amanda Colombo's full profileMacroeconomic headwinds in the US continue to affect the residential and commercial solar sectors in the near-term. Many publicly-traded US distributed solar companies are overcoming economic hardships through innovation and collaboration.

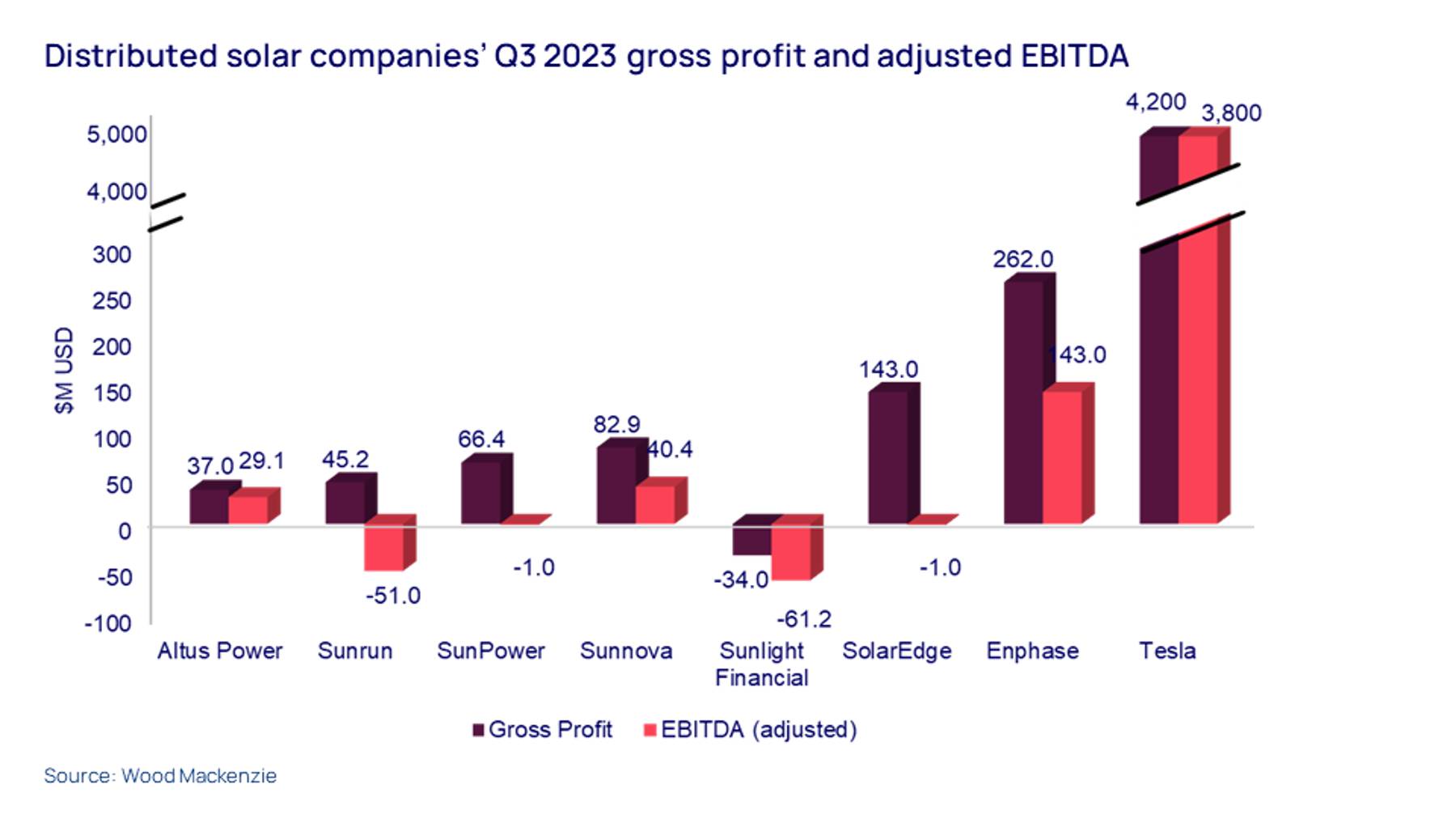

Wood Mackenzie’s Distributed solar public company rundown – from our US Distributed Solar Service – digs into the financial performance of eight publicly-traded distributed solar companies in the first three quarters of 2023, along with their strategies for remaining viable in a challenging environment. Read on for some key highlights.

US distributed solar companies are preparing for the future amid economic headwinds

High interest rates continue to affect distributed solar companies, especially in the residential segment. While residential solar loans are more sensitive to interest rate increases than third-party ownership (TPO) products, high interest rates still impact TPO products and have resulted in price increases. Sunnova and Sunrun, for example, are well-positioned to take advantage of the ITC adders and the industry-wide shift to TPO with their established TPO offerings. But these companies have still been impacted by interest rates and saw declines in adjusted EBITDA in Q3 2023 compared to the previous year. With the expectation of interest rate cuts in 2024, we anticipate that companies will eventually bounce back, but this may not be reflected in installation volumes or financial results until 2025.

Despite declining gross profit and market capitalization figures, some companies are enduring this difficult financial year better than others. In the commercial space, Altus Power continues to acquire both assets and platforms. In the past few months, the company has made multiple acquisitions, including Unico Solar and its solar development platform, as well as portfolios of projects in the Southeast and West. These acquisitions will help Altus expand its presence in these regions of the US and increase its overall market share in the Northeastern community solar space.

Product and partnership diversification are critical drivers of resilience in the solar industry, but impacts vary by market segment

Distributed solar companies have found creative ways to succeed. Those that have diversified – either through products or partnerships – have overall had a more favorable 2023 than those that did not. This diversification helped offset the impact of high interest rates and changing market conditions.

The eight publicly-traded distributed solar companies analyzed in this report vary in micro industries. Some are manufacturers, some are in the residential space and others are in the commercial development space. Based on their financial metrics throughout 2023, high interest rates have particularly affected those operating in the residential segment. Although Tesla’s gross profit and adjusted EBITDA far exceed the other companies that we analyzed, Tesla’s financial metrics also reflect its electric vehicle (EV) business.

{kind=link}

The stories for residential and commercial solar companies vary significantly depending on size, financial backing and operational footprint. Consumer behavior substantially impacts the residential solar market, but financiers do continue to see success in some states with high retail rates, even as increased interest rates persist. The main challenges impacting the commercial segment include interconnection and equipment delays, but this varies by state and developer relationships.

Both residential and commercial solar developers are poised to take advantage of the ITC adders. Even with a lack of clarification for the domestic content adder, developers are eager to leverage the energy communities and LMI adders in the near-term. We expect these ITC adders to contribute meaningfully to these companies’ financial metrics in the future but many companies are still taking conservative approaches to incorporating the benefits into their projections.

Companies that focus on diversifying both products and partnerships will be more successful in the long-term, even if the impacts are not immediately reflected in financial results. Industry partnerships have always been a competitive advantage and are more important than ever before in this high interest rate environment. As we expect interest rates to ease in the near future, companies should be able to bounce back with more resiliency.

Visit the store to access the Distributed solar public company rundown report in full.