Where do polyolefins and olefins fit into the 2019 petrochemicals story?

5 key petrochemicals issues to focus on in 2019

1 minute read

In the 1967 film 'The Graduate', a bold prediction was made: “There is a great future in plastics." Since then, global consumption of plastics and new applications have been the main demand drivers of the petrochemical industry.

Even in 2018, plastics continued to take centre stage for the world’s petrochemical industry. Global demand growth rates exceeded global GDP growth, we saw double-digit demand growth rates in China despite a waste import ban, there was another year of peak profitability across most regional petrochemical-to-plastic value chains and consumers and governments declared war on single-use plastics. Additionally, despite engaging in a trade war with China, the U.S. began implementing a large wave of export-oriented petrochemicals and plastics investments.

The dynamic market events of 2018 will be further enhanced by the following key themes concerning the petrochemical industry in 2019.

1. Peak crude oil transportation demand

Transportation demand, via gasoline, diesel and other distillates, represents the majority of end-use applications for crude oil. As a result, most existing oil refineries are configured to maximise transportation fuels.

The majority of oil companies and analysts, including Wood Mackenzie, believe that transportation demand for crude oil will peak globally in the late-2020s due to improved internal combustion engine efficiency standards, increased use of electric vehicles, and consumer preferences. As a result, many oil production and refining companies are emphasising chemicals - particularly olefins and aromatics - as a key target area for future crude oil long-term demand growth.

Dedicated crude-oil-to-chemicals technologies are being developed by Saudi Aramco, Sabic and ExxonMobil. Many traditional oil refineries will consider retrofitting to maximise production of chemical feedstocks rather than transportation fuels. Other major strategic moves will take the form of mergers, acquisitions, and joint ventures to more tightly connect companies that have crude oil/refined product supply with chemical markets and demand e.g. Saudi Aramco becoming one of the 5 largest chemical companies after acquiring Sabic.

These trends will force national oil companies (NOCs) and international oil companies (IOCs) to greatly increase participation in petrochemical markets.

2. China's drive towards self-sufficiency for basic chemicals and polymers

China has traditionally been the world's largest importer of most petrochemical and plastic raw materials, which has driven its rapid growth in finished goods manufacturing over the past fifteen years. China is massively investing in propylene and primary derivatives to become self-sufficient in this value chain, just like they have already done for polystyrene and PVC chains.

China is currently only around 55% self-sufficient in the ethylene value chain and continues to be the largest importing country in the world for ethylene, polyethylene, ethylene glycol, and other ethylene derivatives. However, China will begin to measurably increase its self-sufficiency in the ethylene value chain through more domestic capacity in this sector beyond the traditionally state-controlled companies of Sinopec, Petrochina, and CNOOC by encouraging further private Chinese and Western investments. The majority of new refinery/paraxylene projects will be implemented by private Chinese companies. These crude-to-chemicals projects often include ethylene complexes as well. Several Chinese steam crackers will also be built by private companies based on imported ethane and/or LPG.

Even with an ethylene self-sufficiency rising above 60%, China will still be extremely dependent on imports for this value chain. There will be a race to fulfill this need among new domestic Chinese capacity additions, other Asia capacity additions (e.g. Korea, Indonesia, Malaysia), Middle East capacity additions, Russia capacity additions, and North America capacity additions. Therefore, competition for importing ethylene and ethylene derivatives into China will likely become tougher.

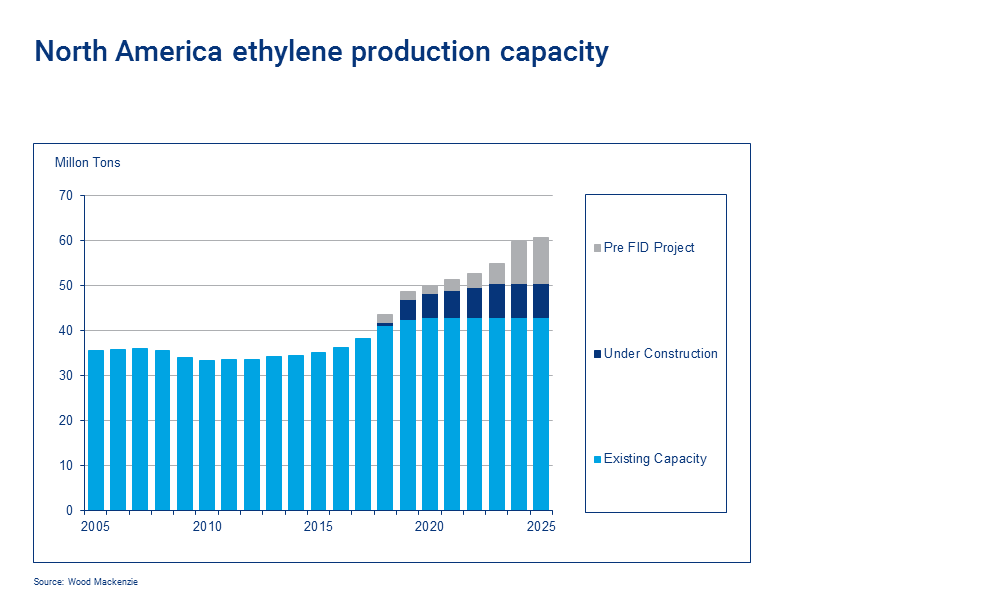

3. Second wave of investments in North America

North America's shale gas developments have accelerated a huge wave of new ethane-based ethylene/PE/MEG export-oriented facilities starting up in the 2017-2019 period. A second wave will reach FID in 2019/2020, with commercial production expected in the first half of the 2020s.

However, North American ethane prices rose to unexpectedly high levels in 2018 due to inadequate infrastructure to bring ethane from shale gas fields to steam crackers, and a surge in demand from the first wave of new ethylene facilities. This recent spike in ethane prices will give pause to those considering a second wave of investments in North America. However, there is plenty of cost-advantaged ethane supply in North America to support a second wave of export-oriented ethylene and derivative facilities that will become available after further ethane midstream infrastructure investments are completed.

Significantly more NGL exports will also occur from the U.S., as evidenced by increased volumes of associated liquids anticipated from the Permian Basin and the construction of several new export terminals. Many of these new NGL exports will be targeted to feed China's propylene (new PDH units) and ethylene (new ethane and LPG crackers) assets. However, as long as the current trade war continues between the U.S. and China, many new China chemical project decisions and government approvals based on imported ethane and propane will be delayed.

4. Recycling of plastics

Improper waste disposal of plastic goods in the world's oceans has resulted in a backlash against single-use plastics from consumers, governments, and brand owners.

This backlash has taken the form of bans or levies on certain plastic products (e.g. straws and bags), initiatives to recycle more plastics (e.g. investments in recycling infrastructure system and development of chemical recycling technologies), and improvements to waste management systems, particularly in developing countries that often dispose of most waste including plastics directly into waterways.

These initiatives are being, and will continue to be, implemented by changes to consumer behavior, government legislation, industry trade association responses, and major brand owner requirements for the sustainability of their products and packaging.

Olefins and polyolefins represent the greatest share of existing plastic packaging. Plastic companies will, therefore, strive to make their products more recyclable, look for ways to incorporate recycled materials into their business and/or production processes, and to ultimately prepare for longer-term demand destruction of particular plastic single-use segments.

5. Consumption growth in the developing world

Like most raw materials, petrochemical demand growth is fastest within developing economies. Economies with rapidly developing finished product manufacturing industries and a rapidly growing middle classes seeking higher standards of living are leading demand growth for petrochemicals.

China is evolving from a manufacturing and export economy to an economy with a rapidly growing middle class. As such, we expect China's demand growth for petrochemicals and plastics to maintain a similar pace - as has been witnessed for the past decade. There are still rapidly growing manufacturing industries and/or middle classes in India, Southeast Asia (Vietnam, Indonesia, etc.) and Africa, which will also see rapid demand growth for petrochemicals for the next 20+ years.

Plastics are also assisting with the global energy transition towards cleaner and renewable fuels. Some examples include plastic piping used to transport natural gas within electric power plants, plastic piping used to recycle water from shale gas wells, plastic structures used in solar panels and wind turbines, and plastic components used in electric vehicles.