Global gas industry in the 2050 net zero world

Gas has a key role to play in the energy transition, but only if it can decarbonise

6 minute read

Kateryna Filippenko

Research Director, Global Gas Markets

Kateryna Filippenko

Research Director, Global Gas Markets

Principal Analyst with a focus on the European gas market and the development of alternative scenarios.

Latest articles by Kateryna

-

Opinion

Biomethane price puzzle: why demand-side policy is the missing piece

-

Featured

Gas & LNG: region-by-region predictions for 2026

-

Opinion

Europe gas & LNG: 5 things to look for in 2026

-

Opinion

FuelEU Maritime: a catalyst for bio-LNG market growth

-

Opinion

Green gains: inside the rise of North American renewable natural gas

-

Opinion

Gastech 2024: Our top three takeaways

Massimo Di Odoardo

Vice President, Gas and LNG Research

Massimo Di Odoardo

Vice President, Gas and LNG Research

Massimo brings extensive knowledge of the entire gas industry value chain to his role leading gas and LNG consulting.

Latest articles by Massimo

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

LNG: why a resilient portfolio is increasingly key to success

-

The Edge

Ten takeaways from WoodMac’s LNG Conference

-

Opinion

Horizons Live: Strait talking | Webinar replay

-

The Edge

How power markets can adapt to energy crises

-

The Edge

Ceasefire in the Middle East

Prakash Sharma

Vice President, Head of Scenarios and Technologies

Prakash Sharma

Vice President, Head of Scenarios and Technologies

Prakash leads a team of analysts designing research for the energy transition.

Latest articles by Prakash

-

Opinion

Rising demand for nuclear fuels: security, supply and the AI power boom

-

The Edge

Will falling populations reshape energy demand?

-

Opinion

How is energy transition investment evolving in 2026?

-

The Edge

How the Iran war could change energy markets

-

Opinion

Energy transition outlook: Asia Pacific

-

Opinion

Energy transition outlook: Africa

The global gas market is facing a range of major unknowns. From the current market volatility to the long-term uncertainty of gas demand longevity and the impact of the energy transition.

Wood Mackenzie’s base case assumes that gas demand will be resilient for the next 20 years at least, while LNG demand will growth through to 2050 requiring substantial investments in new gas and LNG projects.

However, we predict that emissions will continue to grow until the late 2020s and global warming will reach 2.5 degrees or higher by the end of the century, far above the Paris agreement goals.

In our Energy Transition Outlook, we consider alternative scenarios. The most optimistic climate outcome – our 2050 net zero scenario – is one where global net zero is reached by 2050, and global warming is limited under 1.5 degrees by 2100, in line with the most ambitious goal of the Paris agreement.

In a recent report, Global gas in the 2050 net zero world, we used Wood Mackenzie’s proprietary Global Gas Model Next Generation to analyse the implications of this scenario on gas markets, trade flows and prices. A detailed dataset is now also available on our new Lens Gas and LNG platform where subscribers can compare key scenario outcomes against our base case.

Read on for an introduction to some of the key takeaways from this analysis and fill in the form to download an extract from the report.

There is more than one way to get to 2050 net zero

There are different ways to achieve net zero. The pace of technology development may differ from our assumptions, policies and market drivers may take a different shape, new factors may come into play. Other pathways could result in even lower gas demand compared to our net zero scenario.

For example, in their Net Zero Emissions scenario (NZE), the International Energy Agency (IEA) envisaged a scenario where gas plays a significantly smaller role compared to our 2050 Net Zero (WM NZ) scenario.

IEA NZE estimates gas demand to decline to 3,400 bcm in 2030 and to 920 bcm in 2050. We believe gas demand will remain strong at 3,800 bcm until 2030 and decline by around 34% to 2,500 bcm by 2050. There are three key reasons for the difference between the two outlooks.

Firstly, both scenarios see energy efficiency as the key to reaching net zero, but the IEA is significantly more aggressive about achieving energy efficiency improvements. IEA NZE expects final energy use to decline by 22% by 2050 despite an increase of 2 billion in world population and an assumption of universal access to energy by 2030, while we see the final energy consumption falling by under 5%.

Secondly, the scenarios agree that electrification of buildings is the main route to decarbonise the residential sector, but IEA NZE expects gas to be fully substituted with electricity. We believe this is unrealistic to deliver, particularly in developing markets and considering challenges of retrofitting existing building stock.

And finally, IEA NZE expects gas demand in power to decline by over 90% by 2050, while we believe gas demand in power to be more resilient. We see gas paired with CCUS as a key provider of flexible dispatchable generation, while IEA NZE expects power sector to manage flexibility mostly through the re-design of the grid, more investment into transmission and distribution infrastructure and decentralised power and micro grids.

More on the IEA NZE can be accessed here.

Gas can help developing markets decarbonise and support renewables rollout

While oil and coal are going to be largely displaced from the mix with demand declining by 65% and 90% by 2050, we believe gas will decline by only 34% as it helps the world transition to a low carbon economy.

With electrification at the heart of achieving net zero, decarbonising the power grid will be key. Gas could be the cheapest and most feasible way to achieve this in developing Asian markets that are still reliant on coal, or when scaling up renewables is a challenge.

In other regions, growth in electricity demand, coupled with the increased roll out of intermittent renewable energy will require low-carbon dispatchable generation sources to support grid stability and provide flexibility. Gas paired with CCUS plays that role in our net zero analysis.

But in the industrial and residential sectors, electrification has limitations, especially in energy intensive industries requiring high-temperature heat. If gas can improve its carbon credentials, it will remain part of the energy mix in these sectors. Pairing gas with CCUS at scale provides the most cost-effective way to support industrial production while keeping carbon emissions in check.

And finally, growing demand for blue hydrogen in this scenario will support gas demand as a feedstock for low-carbon hydrogen.

New investment in gas and LNG supply will still be required

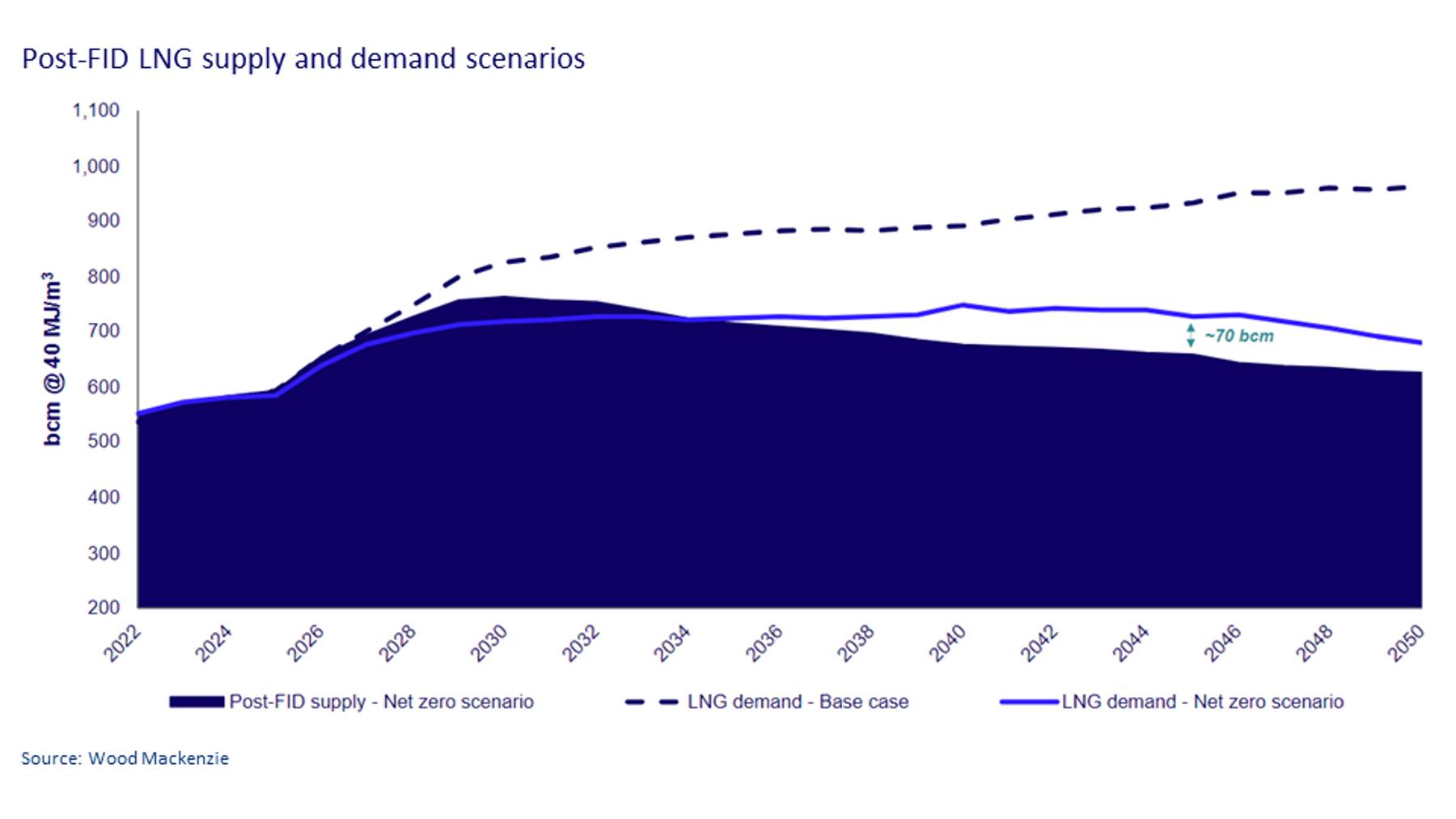

While global gas demand peaks in the late 2020s in the net zero scenario, global LNG demand remains stable through the 2030s and most of the 2040s as growth in Asia offsets decline elsewhere. Gas demand will grow strongly in emerging Asian markets in the face of increasing population, economic growth, urbanization and switching away from coal. This, coupled with limited domestic gas supply, boosts their LNG imports in this scenario.

The recent wave of LNG investments will bring a surge of supply in the next couple of years, but longer term, new projects will need to be developed– we estimate about 70 bcm of pre-FID supply will be required by 2045 in the net zero scenario (217 bcm in our base case). Competition will intensify. Buyers will be looking for suppliers who are able to deliver low-cost LNG, offer flexibility of contract terms, be relatively close to the demand centers and can minimize their carbon footprint. We predict prices will need to stay at a level sufficient to encourage these new developments.

{kind=link}

{kind=link}

It’s time for the industry to adapt

The opportunity for new gas and LNG projects is still there. But to be able to seize it and to fit into the low-carbon world, the industry will have to adapt.

Gas production must decarbonise to stay relevant. The industry urgently needs to tackle its methane footprint, embrace new technologies such as CCUS and manage emissions along the full value chain, including scopes 1,2 and 3. Some of this we can already see now. For example, projects like Papua LNG and Ruwais LNG are reducing emissions at LNG plants by using electric drive trains. The under construction plants in Qatar and Malaysia are implementing CCS to reduce both upstream and plant emissions by capturing and storing reservoir CO2. Other examples include methane leakage detection programmes or the use of renewables to replace gas in power production.

But as market space inevitably shrinks, some infrastructure projects may go underutilised, and the competitiveness of supply projects will likely be assessed very differently in a net zero world. Only those with business models focused on minimizing carbon footprint will be able to thrive.

Gas players need to be ready to embrace cross-sectoral integration and the new opportunities it offers. Low-cost gas resource holders will increasingly consider alternative gas monetization routes such as developing blue ammonia by producing low-carbon hydrogen through gas reforming with carbon capture, instead of traditional gas exports.

Company strategies, policies and investor attitudes need to adapt to a world where carbon reduction and trade take center stage, leading to a different set of trade flows and commercial relationships. The global gas and LNG market would look very different under a net zero scenario.

Fill in the form at the top of the page to download an extract of our report for more on this scenario analysis.

Lens Gas & LNG

The single source for exploring industry data alongside leading expertise, analyses, and modelling insights.

Find out more