Will India set a net zero target?

COP26 is putting rising pressure on the world’s third largest carbon emitter

1 minute read

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

Latest articles by Gavin

-

Opinion

Is Nigeria’s deepwater roaring back?

-

Opinion

Why US Henry Hub natural gas prices are set to rise | Webinar replay

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

-

Opinion

Horizons Live: Strait talking | Webinar replay

When India’s power minister RK Singh described net zero targets as “pie in the sky” at the IEA-COP26 Net Zero Summit in March, he was specifically taking aim at the developed world. For all the commitments to achieving net zero emissions by 2050 from the world’s richest countries, Minister Singh openly questioned actual levels of activity under way to achieve this.

But the other clear message from India was that it is unreasonable for developing countries to be expected to make the same kind of commitments to net zero emissions, at least not by 2050. For India (and many others), this is the crux of action on global warming: why should developing economies that contributed little to historic emissions now be expected to do the same as the developed world to tackle carbon?

Of course, the ‘you caused it, you clean it up’ argument on emissions has been put forward by emerging economies for many years, and not without justification. But for India, as the world’s third-largest carbon emitter after China and the US, this increasingly looks like a difficult position to maintain.

As COP26 approaches, pressure on India to commit to net zero is increasing. Global action on climate change is firmly at the top of the political agenda. Richer nations are queuing up to commit to doing more: the Biden administration’s ambitious target to reduce emissions by 50-52% below 2005 levels by 2030 followed a raft of enhanced 2030-35 targets from the EU, the UK and Japan. With each more ambitious emissions reduction proposal, pressure rachets up on those countries yet to announce targets.

But the greatest pressure on India may yet come from China. Despite still being classified as a developing economy, China set its 2060 net zero target last September and followed this with a more ambitious 2030 emissions intensity reduction target (-65% on 2005).

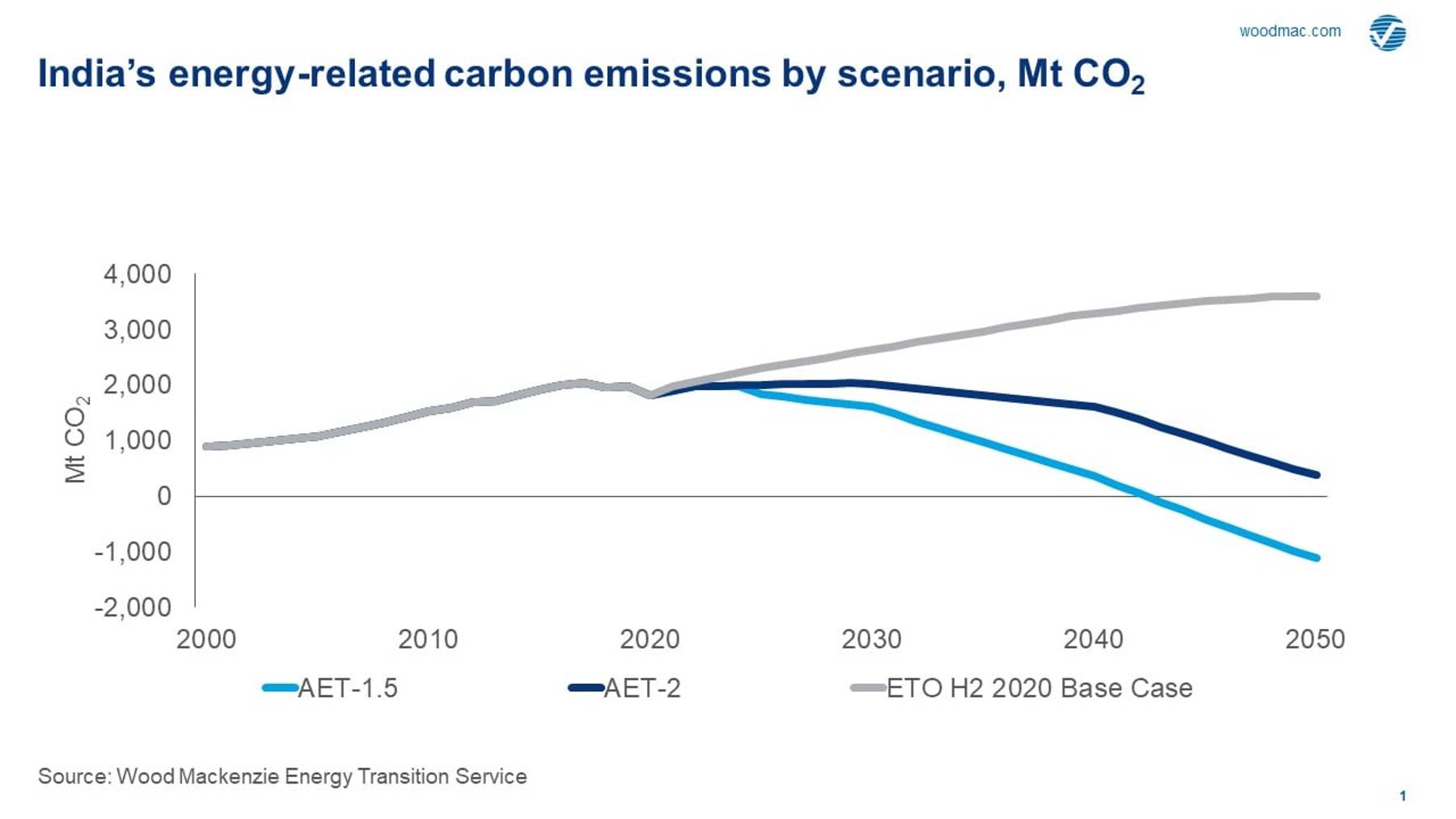

India’s leaders will respond by pointing to the country’s per capita carbon emissions remaining among the lowest globally. This is not in dispute, but more importantly the overall pace of India’s emissions growth and rising share of global output is bringing it into the spotlight. In our base case, India is the global outlier on carbon, with energy-related emissions only peaking by 2049 and rising over 200% versus 2005 levels by 2050. By comparison, China’s emissions peak two decades earlier, though emissions are more than three times India’s 2049 peak at this point.

In this, China is arguably setting its strategic rival a direct challenge around both action on climate change and regional leadership. China will expect to play a major role at COP26 in Glasgow this November. Without a net zero target in place, can India realistically expect to do the same?

India’s lack of a net zero target – the case for the defence

In his speech to the IEA Net Zero Summit, Minister Singh effectively made the case for the defence, arguing that on a emission intensity basis – specifically emission reductions based on GDP per capita - India is arguably the only major economy on track to meet or even exceed the Paris targets, in part due to its rapid expansion of renewable power. This is implicit in India’s NDC targets of reducing emissions intensity by 33-35% compared to 2005 levels by 2030, which Minister Singh argued was more important than a long-term net zero target without real substance.

India’s position is that for any 2050 net zero commitments to have real impact, action on emissions must get under way sooner rather than later. Vague promises to reduce emissions in the distant future are not enough. This means making difficult choices now, identifying future investments and prioritising long-term goals by setting short-term action in motion. And on this, India argues that developed nations are simply not doing enough.

India’s incredibly low carbon emissions on both a net per capita and per unit of GDP basis must also feature in this consideration. Rising emissions also give India considerably less time to reach a net zero 2050 target than most other major economies, something the government has been keen to point out.

But this in large part also explains India’s dilemma. As a developing economy ravaged by the pandemic, India’s priorities today are not driven by climate change. Far more urgent for India’s leaders and wider population are domestic concerns over employment, healthcare and the expansion of basic services such as electricity. For the average Indian citizen, a 2050 net zero target is effectively meaningless.

{kind=link}

What an Indian net zero target might look like (and how to achieve it)

India is a truly unique country, and so its path to decarbonisation – and correspondingly its future net zero commitments – will look different to others. With a young and rising population, sustained economic growth is the foundation of government policy. Delivering on future net zero targets will need to live with this. Arguably, a 2060 net zero target similar to China looks more feasible than a 2050 commitment.

Yet in our AET-2 scenario, consistent with a 2 degree celsius world, India achieves net zero only by 2070, despite increased levels of investment in renewables and more aggressive action on coal. This still requires concerted effort to achieve, given over half of all capacity and 70% of electricity generation currently comes from coal – with low cost domestic coal helping to meet domestic power demand and support energy security.

Renewable power is essential to any decarbonisation target for India. The country has hugely ambitious plans for both solar and wind, and while achieving its target of 450 GW of installed renewable capacity by the end of the decade has been dented by the pandemic, investment continues to gather pace. In our AET-2 scenario, renewables climb to 52% of the generation mix by 2030 and 70% by 2050 as the transition accelerates. In our AET-1.5 scenario, India hits net zero by 2050, but the ask is significantly more difficult: renewables penetration has to increase further alongside adoption of other technologies such as advanced nuclear, hydrogen and carbon removal.

The carrot and stick approach to encouraging India towards a net zero target

There is a clear and compelling argument for richer countries to actively support developing economies in their efforts towards decarbonisation. In applying pressure on India to commit to a net zero target, the US, Europe and others must also consider significant direct financial and technology support to help with the country’s decarbonisation pathway. Helping to bring down the costs of new technology to mitigate the impact of the transition on India’s population will be crucial.

But India’s government must also buy into the huge potential that low carbon energy can bring to its wider economic goals. By avoiding massive near- to mid-term investment in new carbon-intensive capital stock that risks becoming obsolete and instead pushing investment towards new energy could prove compelling if delivered efficiently. India’s rising dependence on imported oil and gas and consequent savings by avoiding this are another compelling reason: current high prices should help the case.

India must also consider how it sets and implements future net zero targets. Differences in efforts to tackle decarbonisation at the state level are already becoming apparent, with states such as Kerala displaying rising ambition while more heavily industrialised states in the north continue to focus on hydrocarbons. Unleashing India’s sky-high levels of innovation and entrepreneurialism may be half the battle; avoiding the country’s infamously centralised bureaucracy could be the other.

If you would like to know more about India’s possible pathways to net zero 2050, please let me know.

APAC Energy Buzz is a weekly blog by Wood Mackenzie Asia Pacific Vice Chair, Gavin Thompson. In his blog, Gavin shares the sights and sounds of what’s trending in the region and what’s weighing on business leaders’ minds.