Get in touch

-

Mark Thomtonmark.thomton@woodmac.com

+1 630 881 6885 -

Hla Myat Monhla.myatmon@woodmac.com

+65 8533 8860 -

Chris Bobachris.boba@woodmac.com

+44 7408 841129 -

Angélica Juárezangelica.juarez@woodmac.com

+5256 4171 1980

China leads global wind turbine manufacturers’ market share in 2023

Goldwind in the top spot for second year, followed by Envision and Vestas

3 minute read

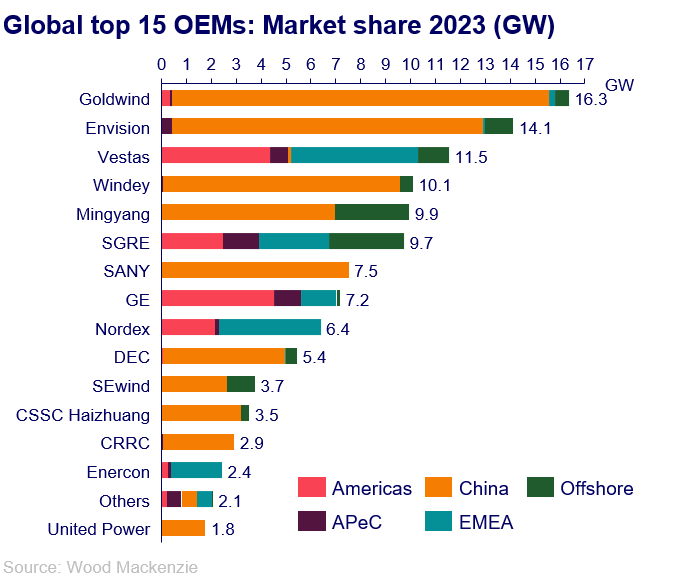

China accounted for 65% of global wind capacity in 2023, which pushed four Chinese wind turbine original equipment manufacturers (OEM) into the top five global rankings, a first for the sector. With a record of 16.3 gigawatts (GW) capacity installed, Goldwind maintained the leading position for the second consecutive year, according to latest analysis from Wood Mackenzie.

Envision closely followed with 14.1 GW, the company’s best year yet, and at third place, Vestas connected 11.5 GW, the only western OEM in the global top five. At fourth and fifth places, Windey and MingYang installed 10.1 GW and 9.9 GW, respectively. Overall, the market remained consolidated with 54% of the global wind markets held by the top five OEMs.

Note: Wood Mackenzie bases its analysis on grid connected capacity in all wind markets, apart from China and Vietnam.

Outside of China, Vestas was the market leader for the sixth consecutive year, with more than 10 GW installed. Siemens Gamesa (SGRE) overtook General Electric (GE) for the second position. SGRE capitalised on offshore success with 9.7 GW installed, while GE installed 7.2 GW globally, supported by the US onshore market. Nordex came in at fourth place with 6.4 GW and Enercon at fifth place with 2.4 GW. Overall, the top five western OEMs represented 93% of the global volumes outside of China.

Source: Wood Mackenzie

Note: Wood Mackenzie bases its analysis on grid connected capacity in all wind markets, apart from China and Vietnam.

Record levels driven by China’s wind power boom

“China’s first batch of massive renewable bases have a 2024 deadline on the horizon which has accelerated installations to an unprecedent pace of 74.7 GW. This combined with a mature supply chain and ambitious provincial targets are pushing wind deployment to an unprecedented level in China,” said Endri Lico, Principal Analyst at Wood Mackenzie.

Onshore capacity achieved new highs of 67.8 GW, while almost 7 GW of new offshore installations were in China, an increase of 41% YoY, which ultimately drove six Chinese OEMs into the global top 10 rankings.

The country’s record installations, backed by more than 100 GW of new wind turbine orders in 2023, has not shielded local OEMs from reducing profitability. Intense competition from 14 different Chinese OEMs in 2023 reduced turbine prices by 16% and 9% in onshore and offshore, respectively, throughout the year.

Western manufacturers pressured by market slowdown

In comparison, 2023 was a disappointing year for western OEMs. Companies across Europe and the Americas suffered financial losses in a stalling wind market that plateaued at 40 GW capacity installed, a 3% drop YoY, which is the lowest year since the COVID-19 pandemic.

“Western OEMs practiced commercial discipline, showing little appetite for price reduction to grow market share. 2023 saw some improvement in financial performance as some of the supply chain disruptions eased, but quality and reliability issues have emerged as another source of instability for western OEMs,” Lico said.

ENDS

Relevant news and commentary

- News: Record highs for global wind turbine order intake in 2023

- News: Government tenders to drive 102 GW of global renewable capacity in 2024

- Article: Offshore wind energy: what to look for in 2024

- Article: Onshore wind energy: what to look for in 2024

- Article: Western wind turbine manufacturers are prioritising profit over volume, opening the door for Chinese market share growth

- Article: Wind turbine technology evolution is diverging quickly between China and the rest of the world

- News: Global wind power outlook falls by 29 GW Q-o-Q

- News: US$ 27 billion investment required to mobilise global offshore wind supply chain (August 2023)