Get in touch

-

Mark Thomtonmark.thomton@woodmac.com

+1 630 881 6885 -

Hla Myat Monhla.myatmon@woodmac.com

+65 8533 8860 -

Chris Bobachris.boba@woodmac.com

+44 7408 841129 -

Angélica Juárezangelica.juarez@woodmac.com

+5256 4171 1980

Top three western wind turbine OEMs to control 60% of market by 2028

Goldwind will climb rankings to second place in 2020

1 minute read

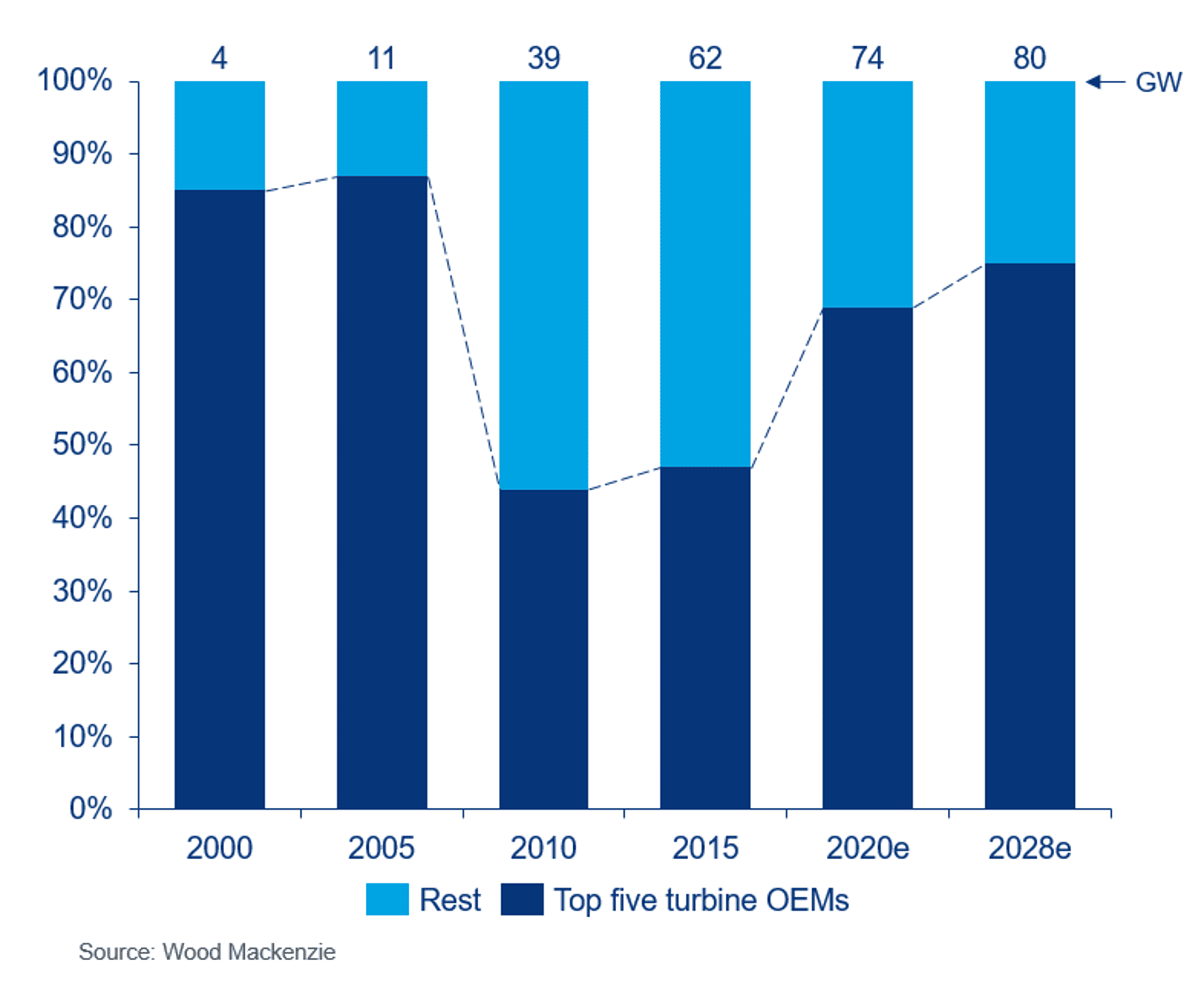

Market share consolidation by global wind turbine original equipment manufacturers (OEMs) is set to intensify.

After a decade of fragmentation, the top five global turbine OEMs are strengthening their hold on the industry. By 2028, they are expected to control three quarters of the sector.

The leading three western turbine OEMs will increase their market share from 47% - or 32GW - in 2019 to more than 60% - or 48GW - by 2028, according to new research from Wood Mackenzie.

"Vestas, SGRE and GE will draw upon strategic relationships with major asset owners to execute large-scale projects while also investing in new products and technologies. Vestas, the clear leader in this space, will see its market share elevated to an average of 20% over the next five years.

“SGRE will surpass 100GW of cumulative installed capacity by the end of 2019, becoming the second turbine OEM after Vestas to reach this milestone.

“Vestas reinforces its leading position by being the first turbine OEM to install more than 10GW of annual capacity during 2019. Vestas, SGRE, GE and Goldwind will each install around 10GW in 2020 due to surge in US and China market activity.

“Goldwind’s leading position in China, combined with large projects in Australia and Canada, will see the company take the number two spot for the very first time in 2020.

"The appetite to invest and churn out new products and technologies to lower Levelised Cost of Energy (LCOE) compared to peers will aid in developing an improved commercial position. Regional players, however, will face an uphill battle to compete, as seen from recent troubles at Senvion and Suzlon," said Shashi Barla, Wood Mackenzie Principal Analyst.

As Mr. Barla notes, regional pioneers Senvion and Suzlon are struggling. Suzlon's failed attempts to find a bailout partner have pushed the company into deeper trouble. Senvion offloaded some European assets – namely its blade manufacturing facility in Portugal and its global intellectual property - to SGRE, while other business units are still scouting for investors.

The outlook isn't all bad for regional players, however. Nordex and Enercon are expected to strengthen their presence with increasing investments in new wind turbine technologies. The former is expected to install a record 5.5GW of average annual capacity in 2020 and 2021, a substantial increase of 40% when compared with 2019.

Turbine OEMs only focussed on the onshore wind segment will compete in a flat - 60GW average - global market for the next decade. However, the offshore industry is expected to see a flurry of activity over the outlook period.

"SGRE continues to be an undisputed offshore market leader, with more than 15GW of backlogged orders.

“GE has made an enormous splash in this space, with a combined 4.8GW of orders signed this year in the UK and the US.

"MHI Vestas' robust positioning will elevate its global rank to be within the top ten OEMs by 2023 and number five globally by 2027-2028, representing the only pure-play offshore player within the top five. The company already secured contracts in seven countries totalling more than 7GW.

"MingYang has become rising star in the Chinese offshore sector, with more than 4.5GW of orders signed in the past year. A closer relationship in Guangdong province, the largest offshore market in China, will sustain MingYang’s positioning in the long-term," added Mr. Barla.

Feed-in-tariff (FiT) phase-out in China is expected to trigger a surge in order volume to a combined 56GW in 2019 and 2020.

“Ten of the top 15 turbine OEMs in 2020 will be Chinese, capitalising on a domestic demand surge.

“This rush will provide ample room for tier II players, including CRRC and Windey, to explore turbine supply opportunities, as several larger players may be capacity-constrained.

“Chinese giant Goldwind is the country’s most successful OEM in international markets, with over 50% of Chinese OEM exports attributed to the company. Goldwind is expanding its nacelle manufacturing capacity to 14GW by 2020, of which 3.5GW is earmarked for exports.

“After grappling with product quality concerns for many years, DEC has focused on direct-drive technology and secured over 4GW of orders for a planned 2020-2021 execution,” said Mr. Barla.

{kind=link}