Get Ed Crooks' Energy Pulse in your inbox every week

Congress pushes back on restrictions to US wind

Five reasons why the US wind belt has upward momentum

1 minute read

Ed Crooks

Vice Chair Americas and host of Energy Gang podcast

Ed Crooks

Vice Chair Americas and host of Energy Gang podcast

Ed examines the forces shaping the energy industry globally.

Latest articles by Ed

-

Opinion

Is the competitive power market model broken?

-

Opinion

Is fusion power here at last?

-

Opinion

Battery storage proves its value in moderating Texas power price volatility

-

Opinion

Can the LA Olympics in 2028 be a catalyst for clean energy?

-

Opinion

Strong El Niño event will have wide-ranging impacts on energy

-

Opinion

Why is it so hard to build big energy projects?

David Brown

Director, Global Integrated Energy Research

David Brown

Director, Global Integrated Energy Research

David is a key author of our Energy Transition Outlook and Accelerated Energy Transition Scenarios.

Latest articles by David

-

Opinion

Congress pushes back on restrictions to US wind

-

Opinion

What the Middle East conflict means for the global power sector

-

Opinion

High oil prices could accelerate EV adoption

-

Featured

Autonomous electric vehicles: four things to look for in 2026

-

Opinion

Five things to watch at COP30

-

Opinion

Five things to watch at COP30

Five reasons why the US wind belt has upward momentum

On 12 May, 55 Congressional members sent a letter to the US Department of Defense (DoD) outlining concerns that new federal policies are delaying wind projects. With rapidly rising power demand and national concerns around energy affordability, the letter argues the government should expedite regulatory approvals for new wind projects. It was delivered to the DoD because it manages a certification process that determines timelines for new onshore wind projects.

The US wind sector has faced a series of setbacks since the second inauguration of President Donald Trump. In early March, the president told a group of technology executives to eschew wind and invest in fossil fuels. “Don’t worry about wind. Forget it. It’s worthless,” the president stressed.

Shortly thereafter, the administration announced that it would refund US$1 billion in offshore wind lease fees to TotalEnergies. In return, TotalEnergies would shift investment from wind to hydrocarbons, including an investment in the Rio Grande liquefied natural gas project.

This agreement has been touted by the Trump administration as a model for the future of US energy supply. In late April, Bluepoint Wind and Golden State Wind cancelled projects, pivoting to conventional energy sources.

But the administration’s strategy is facing stiff resistance from Capitol Hill. The letter from lawmakers earlier this week represents key markets for existing and new wind projects ranging from Texas, the Midwest, and Atlantic and Pacific coasts.

The determination of no hazard (DNH) is at the heart of the dispute. A DNH can dictate if a wind project goes ahead or not. It certifies that a project complies with guidelines for sensitive military installations, commercial radar systems and airport flight paths. The certification is issued by the Federal Aviation Administration (FAA), in coordination with the DoD clearinghouse process.

The DNH process has slowed to a trickle under the Trump administration. Obtaining both final FAA determinations and DoD mitigation agreements has become especially challenging. According to Wood Mackenzie’s analysis, the regulatory slowdown could delay at least 60 new wind projects in the US.

Wood Mackenzie view

For renewable power, the US has some of the world’s best wind resources. The country has an onshore ‘wind belt’ through Texas and the Dakotas. In the Northeast, shallow seabeds located near large electricity markets are prime real estate for offshore wind turbines. Right now, the US generates around 12% of its electricity from wind. It is the country’s fourth-largest source of electricity.

The Trump administration has made developing renewable projects much harder, including for US wind. The One Big Beautiful Bill Act reduced zero-carbon investment incentives across the board. Liberation Day tariffs then introduced new economic risks, while supply-chain investigations have created compliance headaches.

In our latest base case forecast, we expect around 48 GW of new wind capacity across both onshore and offshore wind technologies between 2026 and 2032. According to Diego Espinosa, a senior analyst with Wood Mackenzie’s Wind team, around 16 GW of onshore wind projects have been safe-harboured against the sunset of federal tax credits.

Including onshore wind projects under advanced development, permitting and contracting, safe-harboured capacity could jump another 7 GW, to 23 GW. For offshore projects, 6 GW of projects are safe-harboured and are already under construction, Espinosa notes.

While current sentiment remains cautious, wind is not in its final chapter. The US outlook for load growth, leadership in the global AI race and regulatory reform point to a dynamic picture for the US power sector.

Wood Mackenzie believes there are five key reasons that the US energy sector requires an ‘all of the above’ approach to resources, including a gigawatt-sized role for wind power.

- The federal government’s tone towards wind is changing. “The DoE does not want to decide which generation technology should or should not be deployed. Companies and communities should deploy whatever is right for them locally.” This quote is from Carl Coe, chief of staff at the Department of Energy (DoE), who shared his perspective at Wood Mackenzie’s North America Power and Renewables Conference in late April. Coe’s sentiment reflects a pragmatic reality: that the US will need every gigawatt of power in the near term to maintain affordable energy prices and meet load growth.

- Wind has some of the strongest economic returns compared to other zero-carbon technologies, according to Wood Mackenzie’s Lens Power. While economic returns vary across states and power market zones, wind tends to beat utility-scale solar, battery storage and natural gas on an unsubsidised basis, including energy and capacity revenue. Adding a production tax credit gives onshore wind a further financial leg up on other renewable power technologies. The long-term economic returns from wind will outlast the policy ups and downs we have seen across the Biden and Trump administrations.

- US states still support wind. All told, at least 25 states still have pro-wind policies. For example, Massachusetts’ 2026 executive order established a state-level fund for wind projects impacted by lower federal tax credits. New York has maintained its statutory 9-GW target for offshore wind by 2030. MISO’s enhanced reliability framework should favour wind over time. Wind developers need to double-down on community engagement to explain the economic benefits, power reliability and project-completion timelines from new wind projects.

- The build-out of power transmission infrastructure is advancing. Regional transmission organisations that have high wind potential – ERCOT, MISO and PJM – are planning over US$60 billion in new transmission infrastructure. New wind infrastructure lowered onshore wind curtailment by 50% from 2024 to 2025 in SPP. Infrastructure reform can help get more out of existing assets and connect new wind assets over time, a priority in a high load-growth era.

- Interconnection timelines are improving via FERC Order 2023 and ISO reforms. From 2023 to 2025, projects withdrawing from the queue increased by 150%, driven by MISO – a sign that the best projects are moving ahead. Conversely, the number of projects that received an interconnection service agreement increased by over 40% from 2023 to 2025, driven by ERCOT and PJM. Wind projects with committed capital are in prime position to take advantage of regulatory reform.

In brief

Saudi Aramco reported record earnings: driven by geopolitical volatility, Aramco reported Q1 profits of US$33.6 billion, up 26%. With the Strait of Hormuz closed, the company turned to its East-West Pipeline, which, at times, reached maximum capacity of 7.0 mb/d. Aramco’s export profile has defied trends among other Gulf oil exporters, which have had to shut-in production during the US-led naval blockade. Read more in our Corporate Strategy and Analytics Service.

US gas tax holiday: against the backdrop of rising gasoline prices and inflation, President Trump and Energy Secretary Chris Wright have proposed suspending federal fuel taxes. Lowering fuel taxes will help consumers at the pump, according to external studies on the topic. But Congress has to approve any changes to federal taxes; the last time it adjusted these levels was 1993. Potentially lower federal fuel taxes may be offset by other factors. Crude oil prices could go higher in a prolonged Middle East conflict. Consumers would still be subject to state taxes on gasoline or diesel, even if President Trump’s proposal becomes reality.

Geothermal is hot: Fervo, a company that is planning to produce power from geothermal technology, went public on Nasdaq on 13 May. On the first day of trading, it raised US$1.9 billion and reached a market cap of around US$8 billion. Investor appetite reflected demand for carbon-free baseload power for AI and bullish power prices. However, Fervo’s S-1 filing highlighted capex spending requirements, reliance on federal tax credits and power transmission constraints as key risks. The company’s stock debut is part of a wider trend of emerging technology companies going public without existing revenue streams, such as X-Energy and Oklo. Investors are hoping that Fervo will retain the heat.

New nuclear momentum continues: the US Department of Energy has awarded US$94 million to advance small modular reactors (SMRs) technologies. These awards cover a comprehensive range of activities, including advanced design engineering, supply chains and siting and licensing processes. So far, the second Trump administration has awarded around US$900 million to the emerging nuclear power sector. Read more in our next-generation nuclear update.

Other views

Can US success in tight oil and shale gas go global? – Simon Flowers

Mined over matter: Are mines at risk of running out of diesel? – Julian Kettle

The Ripple Effect: How conflict is impacting global metals & mining – Tony Knuston

US utility-scale solar market update: Q1 2026 – Kaitlin Fung

Quote of the week

China’s President Xi Jinping hosted US President Donald Trump on an official state visit in Beijing this week. In a statement published by the Ministry of Foreign Affairs for the People’s Republic of China, President Xi emphasised the need for geopolitical cooperation for the world’s two superpowers.

However, the statement also included a word of caution: “‘Taiwan independence’ and cross-Strait peace are as irreconcilable as fire and water.

“Safeguarding peace and stability across the Taiwan Strait is the biggest common denominator between China and the U.S. The U.S. side must exercise extra caution in handling the Taiwan question.”

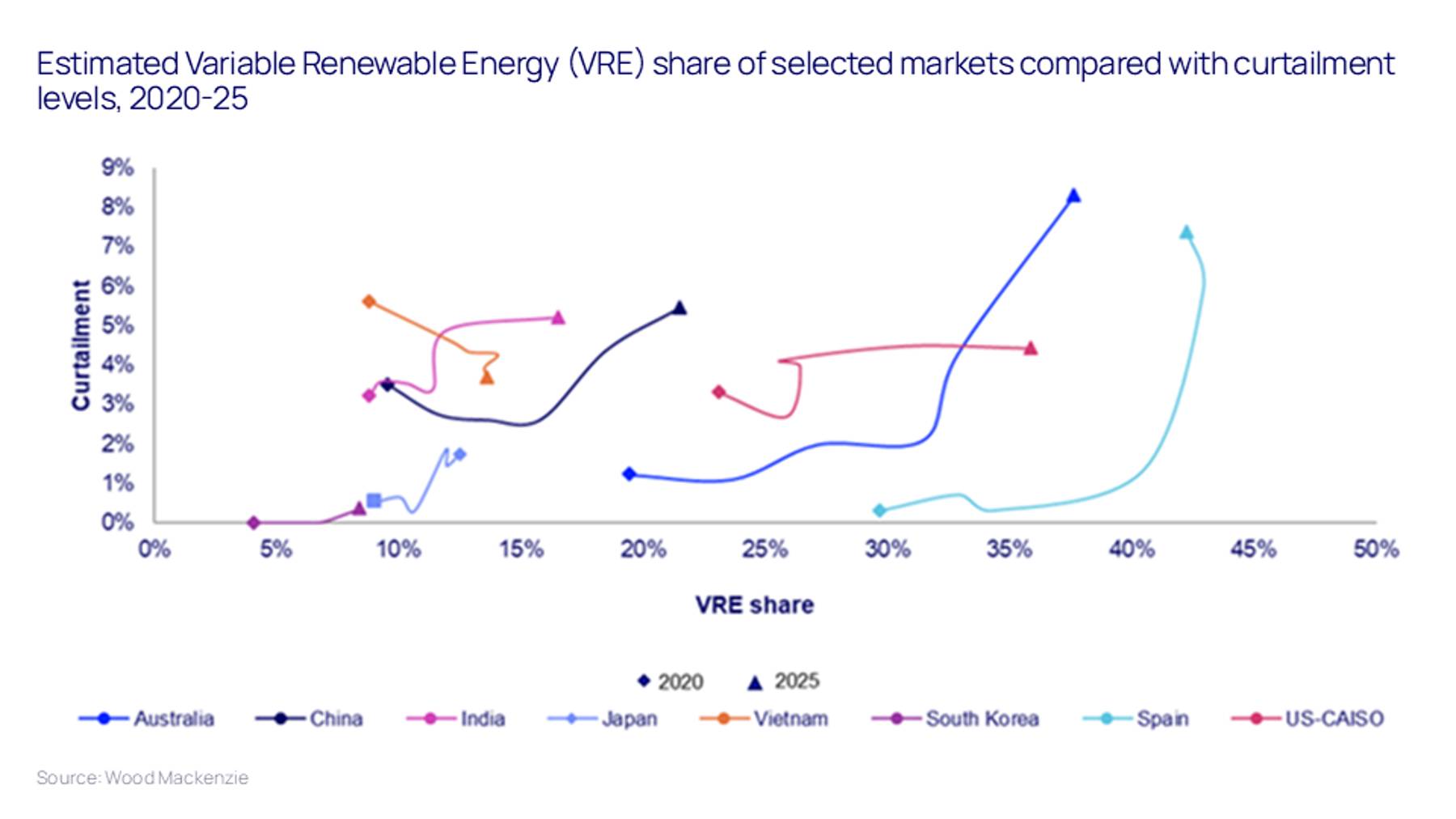

Chart of the week

This chart hails from our Asia Pacific power team. Renewable curtailment in Asia Pacific: solving for flexibility assesses why renewables are not reaching their full potential. The report also breaks down what can be done to get more out of renewables in the future.

The primary constraint across Asia Pacific is low grid flexibility. This is driven by outdated infrastructure, heavy reliance on coal and a stark lag in energy storage and grid expansion relative to rapid renewable deployment. Consequently, China, India and Japan face persistent structural curtailment risks due to slow grid expansion.

Over the next five years, curtailment will dominate the region, creating a sharp divide between developed and developing markets. Advanced markets like Australia, Japan and China are successfully leveraging mature ancillary services and competitive pricing to commercialise storage solutions. In contrast, nascent markets, such as India and South Korea, must urgently implement regulatory, market and technical reforms to unlock necessary revenue streams and contain renewable waste.

{kind=link}

Get The Inside Track

Ed Crooks’ Energy Pulse is featured in our weekly newsletter, the Inside Track, alongside more news and views from our global energy and natural resources experts. Sign up today via the form at the top of the page to ensure you don’t miss a thing.