Why upstream needs to be more ambitious to cut emissions

Tougher policy will help but much is in the industry’s gift

1 minute read

Simon Flowers

Chairman, Chief Analyst

Simon Flowers

Chairman, Chief Analyst

Simon is our Chief Analyst; he provides thought leadership on the trends and innovations shaping the energy industry.

Latest articles by Simon

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

What is the oil and gas industry doing to cut carbon emissions? The biggest challenge to achieve net zero ambitions is Scope 3, the 85% of global emissions generated from combustion in the power, industrial, heating and transportation sectors. The restrained commitments seen so far, beyond a handful of companies, reflects differences of opinion as to whether the responsibility for Scope 3 lies with producers or consumers.

Upstream, in contrast, is clear cut – it’s in the industry’s gift. Dozens of companies have already committed to reduce Scope 1 and 2 – that is, 1.6 BtCO2e a year of emissions from oil and gas production, or 8% of the global total. I chatted to Jessica Brewer, Principal Analyst Upstream, about what action is needed.

What’s the motivation to cut emissions?

Ultimately, the social licence to operate is at risk. It’s already getting harder to access finance, and stakeholder pressure is intensifying. LNG is the canary in the mine. A number of LNG buyers in the last year have started to insist sellers include detailed reporting of emissions, from wellhead to berth, for LNG cargoes. It’s a trend that will become prevalent in LNG, and we expect all oil and gas operators will have to go down this path to make their production marketable.

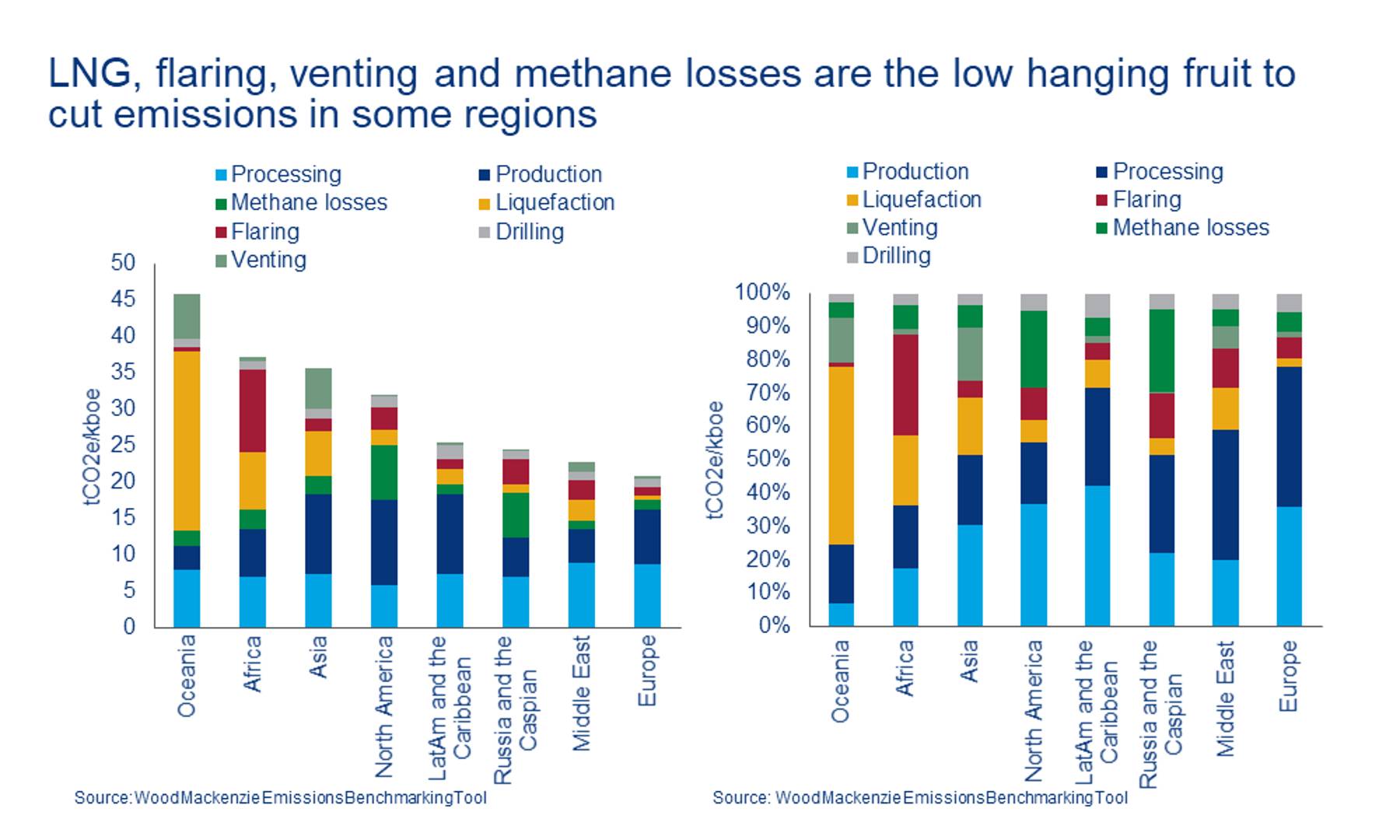

What are the big sources of upstream emissions? Most are produced by combustion of fuel to power operations – drilling, production and processing (58%) and liquefaction (12%).

What are the big sources of upstream emissions?

Most are produced by combustion of fuel to power operations – drilling, production and processing (58%) and liquefaction (12%). The rest are non-combustion emissions from methane losses (14%), mainly leaks from operations; flaring gas (12%) that cannot be monetised or re-injected; and venting CO2 into the atmosphere (4%).

A great deal of energy is required to extract and process oil and gas – power needed to drill wells, so well depth and length are factors; artificial recovery for certain types of reservoirs, mature fields or heavy oil; and the quality of hydrocarbons – oil sands require a lot of processing before they can be sold into the market, as does LNG.

Do emissions vary by region?

Yes. Oceania (Australia) has the highest carbon intensity. The region is dominated by big LNG projects that are remote from infrastructure and use mainly gas generators for liquefaction. Africa, next highest ranked, has high rates of gas flaring because there is no local gas market in some countries. Asia has a number of fields that vent CO2, while North America and Russia score poorly in part due to methane losses from dispersed operations, ageing upstream infrastructure and, in places, limited takeaway capacity.

Europe’s low emissions intensity reflects strong governance and regulation as well as producing basins integrated into the wider energy economy. Gas is sold into big, liquid markets, while some production facilities are connected directly to the national power grid.

Is the industry doing much to cut emissions? We are seeing positive reaction to stakeholder pressure.

Is the industry doing much to cut emissions?

We are seeing positive reaction to stakeholder pressure. More than 30 oil and gas companies, Majors, NOCs and Independents have either set net zero targets or aim for partial reduction of intensity or emissions. Some have linked executive compensation to emissions reduction.

But companies can be far more ambitious to reduce Scope 1 and 2 emissions – eliminating routine flaring, minimising methane emissions through enhanced LDAR (leak detection and repair) and using wind and solar to electrify oil and gas production operations.

Are there good examples of best practice?

The big bang will be electrifying all operations using renewables. Few producing countries can replicate Norway’s success, with the one-third of production already ‘electrified’ tied into its low-carbon national power grid. The share will exceed 50% in 2023.

A few specific projects show the way forward. Equinor will connect remote fields in Norway to a purpose-built offshore wind farm. Santos’ Darwin LNG project uses a battery to provide reserve power for the gas turbine. The industry needs more innovative ideas like these.

A lot of hope is vested in CCS, which has huge potential but is still at the early stages of commercialisation. A major new project in Canada, where the five biggest oil sands producers will collaborate on CCS to achieve net zero Scope 1 and 2 emissions by 2050, is a great example of an industry-wide, industrial-scale solution.

Will policy target upstream producers?

Governments will be key. So far, most producers have had a free ride. Norway and Canada are the only fiscal regimes with a carbon tax on upstream production, though all EU countries plus Norway and the UK are subject to an emissions trading scheme.

The value at risk is potentially material. We estimate that a global carbon price of US$100/tonne would wipe out 10% to 20% of the upstream portfolio value of the top emitting upstream players, leading Majors and NOCs. For those with high carbon-intensive production the hit could be much greater.

We expect carbon pricing and regulation to tighten. Our analysis shows the risk from policy change is greatest for producers operating in developed countries. Less economically developed nations are more likely to rely on oil and gas revenue. There’s an obvious dilemma for these countries, and the possibility that a ‘carbon chasm’ opens up between OECD and petro-dependent nations.

{kind=link}