Energy transition outlook: Middle East

The latest outlook highlights uneven progress for Middle East decarbonisation – and a US$5.3 trillion investment opportunity between now and 2060

2 minute read

Jom Madan

Principal Analyst, Scenarios & Technologies

Jom Madan

Principal Analyst, Scenarios & Technologies

Jom works on scenario modelling for country and global-level energy mixes across all major energy commodities

Latest articles by Jom

-

Opinion

Energy transition outlook: Americas

-

Opinion

How is energy transition investment evolving in 2026?

-

The Edge

How the Iran war could change energy markets

-

Opinion

Energy transition outlook: Asia Pacific

-

Opinion

Energy transition outlook: Middle East

-

Opinion

Energy evolution: navigating the path to a sustainable future

Prakash Sharma

Vice President, Head of Scenarios and Technologies

Prakash Sharma

Vice President, Head of Scenarios and Technologies

Prakash leads a team of analysts designing research for the energy transition.

Latest articles by Prakash

-

The Edge

Will falling populations reshape energy demand?

-

Opinion

How is energy transition investment evolving in 2026?

-

The Edge

How the Iran war could change energy markets

-

Opinion

Energy transition outlook: Asia Pacific

-

Opinion

Energy transition outlook: Africa

-

Opinion

Energy transition outlook: Middle East

The Middle East’s energy transition is uneven, with power generation advancing rapidly through utility-scale solar and storage to meet the needs of data centres and other end users. Hydrogen ambitions are pivoting from exports to low-carbon manufacturing. Oil and gas remain central to economic growth, with producers expanding capacity despite ambitious climate targets. Progress is driven primarily by economics and export competitiveness rather than policy commitments, with deeper decarbonisation depending on market signals.

The 2025-26 update of our Energy Transition Outlook (ETO) explores the ins and outs of a US$5.3 trillion investment opportunity between now and 2060 and explains how the energy and resources industry might evolve to achieve a sustainable and resilient future.

The ETO draws on Wood Mackenzie Lens Energy Transition Scenarios to map four different routes through the global energy transition, each with increasing levels of ambition. Our regional updates drill down into the detail at country level, out to 2060.

Fill in the form at the top of the page to receive a complimentary extract from the Middle East report and read on for an introduction to some of the key themes.

Domestic resources shape Middle East countries’ energy transition ambitions

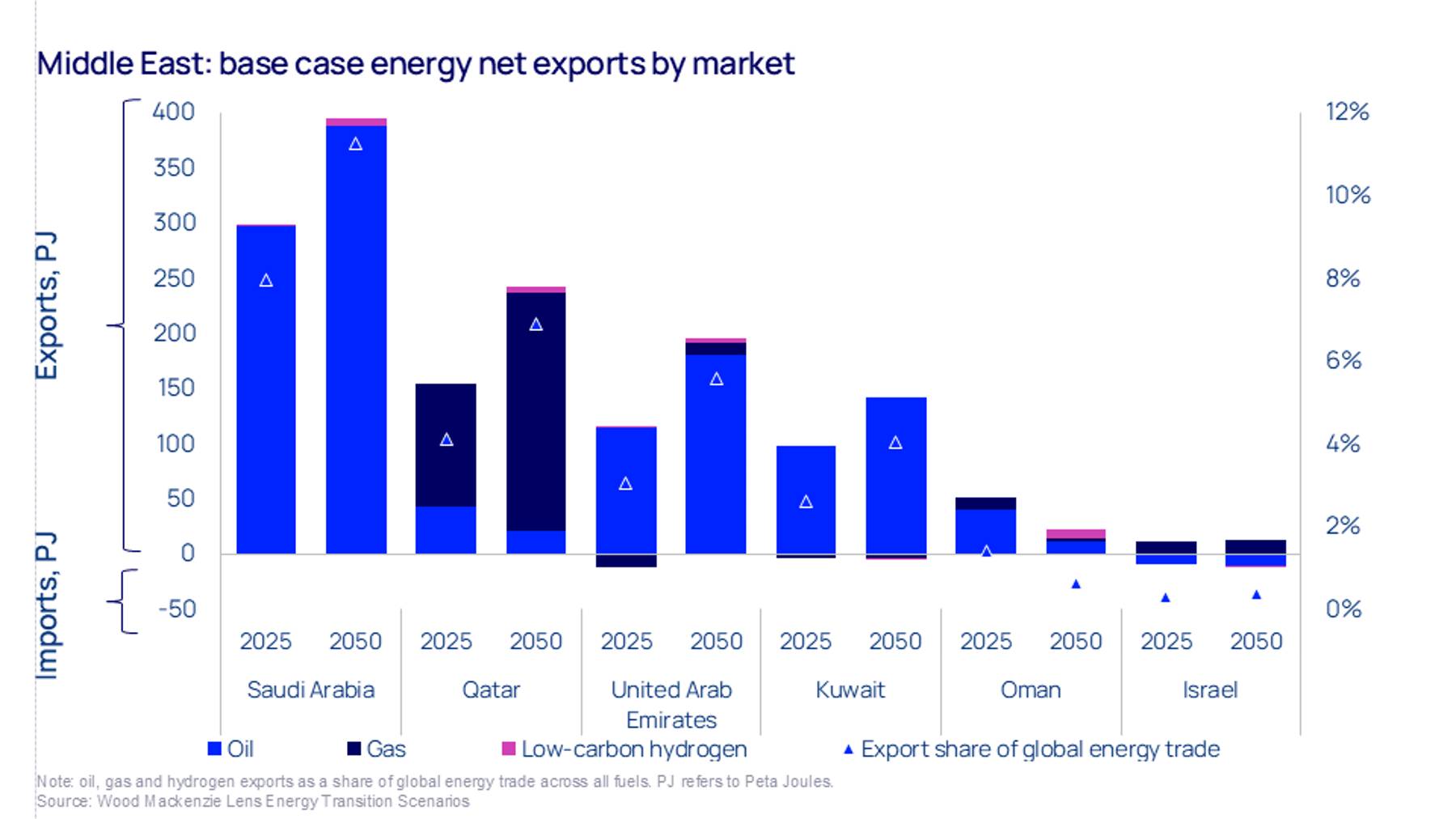

Middle Eastern countries’ emission reduction ambitions depend on two factors: their reliance on hydrocarbon revenue and how their resources compare with those of other producers. Producers with large, low-cost reserves face little pressure to transition quickly, while those with declining reserves or higher costs see the shift as a strategic necessity.

Oman and Qatar illustrate this contrast. With its oil and gas reserves in decline, Oman is pushing hard into hydrogen, setting some of the region’s most ambitious targets and building supporting infrastructure. Qatar, with massive gas reserves and a major liquefied natural gas (LNG) expansion underway, is the polar opposite. It faces less immediate pressure to move away from hydrocarbons, given the resilience of gas demand, even under accelerated climate scenarios.

{kind=link}

Middle East energy transition targets hinge on technologies scaling in tandem

Middle Eastern governments’ ambitious clean energy plans span emissions cuts, renewable deployment, carbon capture and hydrogen. The targets were designed in concert, with clean energy goals partly depending on the commercialisation of low-carbon exports. As the energy transition loses momentum, however, that interdependence is becoming a liability.

Hydrogen was supposed to underpin both the region’s renewable expansion and early carbon capture deployment. Ultra-cheap solar and abundant gas supported the belief that the Gulf could produce green and blue hydrogen competitively, with Europe and parts of Asia likely to take the volumes as they decarbonised heavy industry.

That assumption is now under strain, with project costs rising far beyond early estimates. More importantly, the issue of long-distance transport remains unresolved. Without a credible pathway to transport hydrogen at scale, export-oriented strategies lose coherence.

Could localising heavy industry revive stalled Middle East hydrogen plans?

Some governments are attempting to adapt to hydrogen’s constraints rather than abandon the broader strategy. Oman has moved furthest towards a model that avoids hydrogen shipping altogether. Rather than export hydrogen directly, it is courting energy-intensive industries, particular steelmaking, to locate production near its hydrogen hubs.

Oman’s approach raises its own geopolitical and economic sensitivities. Europe is the most likely end market for low-carbon iron, yet policymakers remain wary of eroding domestic industrial capacity. While importing semi-finished iron is politically more acceptable than relocating entire integrated mills, it still raises concerns over competitiveness and employment.

The Middle East’s clean energy strategy was always contingent on hydrogen playing a central role. Unless producers can establish credible offtake pathways, either by embedding industry locally or securing long-term agreements abroad, they will struggle to deliver renewable buildout, carbon capture plans and emission reduction targets.

Countries are also keen to lure data centres to the region to capitalise on its low-cost power. Governments have further moved to entice solar photovoltaic producers, especially Chinese firms, to the region. The Middle East is growing into a vertically integrated solar manufacturing supply chain hub, with production capacity expected to reach around 44 GW by 2028.

Learn more about Middle East energy transition scenarios

The updated Energy Transition Outlook for the Middle East 2025-26 sets out the commodity and power outlooks in our base-case, as well as three energy transition scenarios: delayed transition, country pledges and net zero.

The report includes:

- Regional overview and spotlights on six major markets out to 2060: Saudi Arabia, Oman, Qatar, the United Arab Emirates, Kuwait and Israel.

- A status update on current emissions trajectories

- An assessment of how each country’s transition is being led by its export ambitions.

- Commodity and market outlooks under our base case and three energy transition scenarios.

- An exploration of the increase in industry localisation, which could prove a viable way of reviving stalled hydrogen plans and scaling up domestic manufacturing.