Energy transition outlook: Net zero scenario

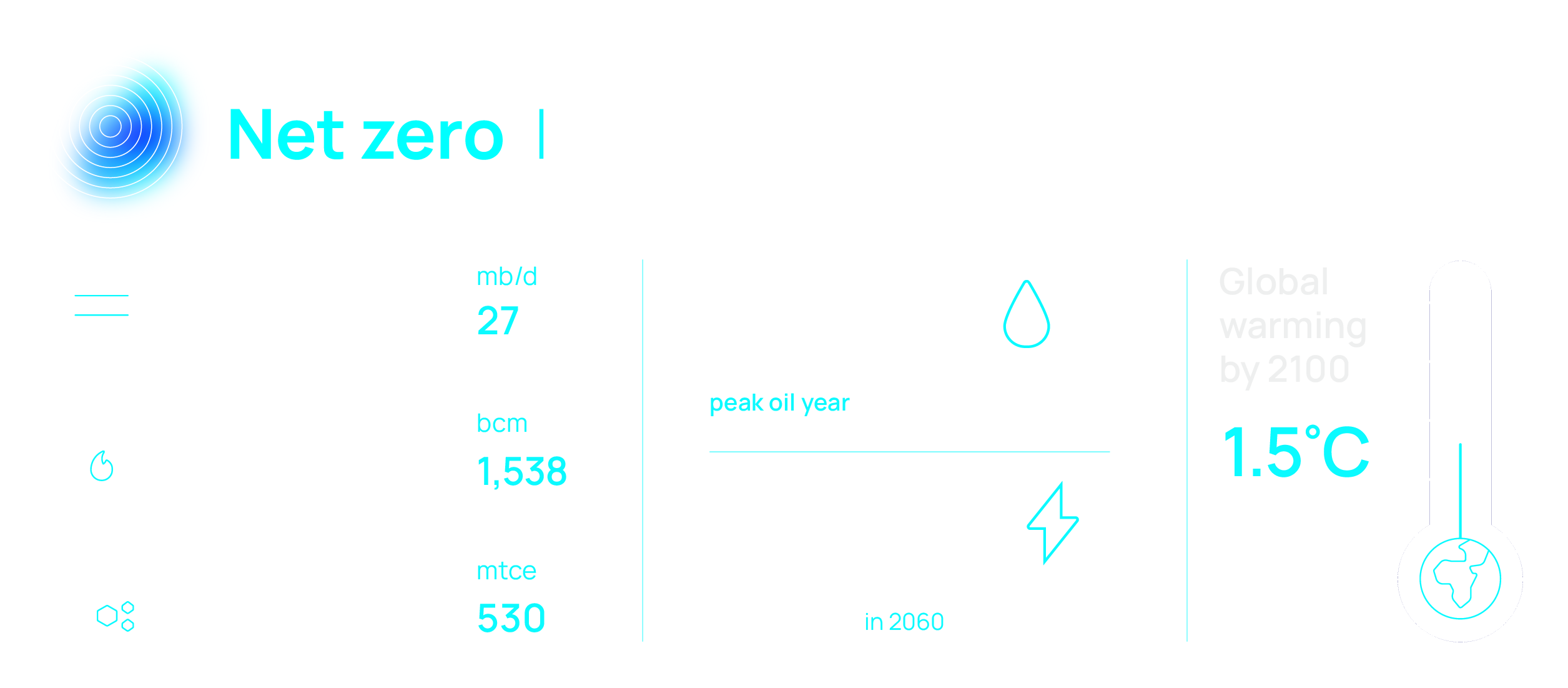

Global warming target of 1.5°C achieved by 2100.

Download executive summary

This pathway represents a wholesale rewiring of the global energy system. Renewables dominate while advanced technologies displace remaining fossil emissions.

The most ambitious Paris Agreement goals are met. Developed economies reach net zero by 2050 and emerging markets follow.

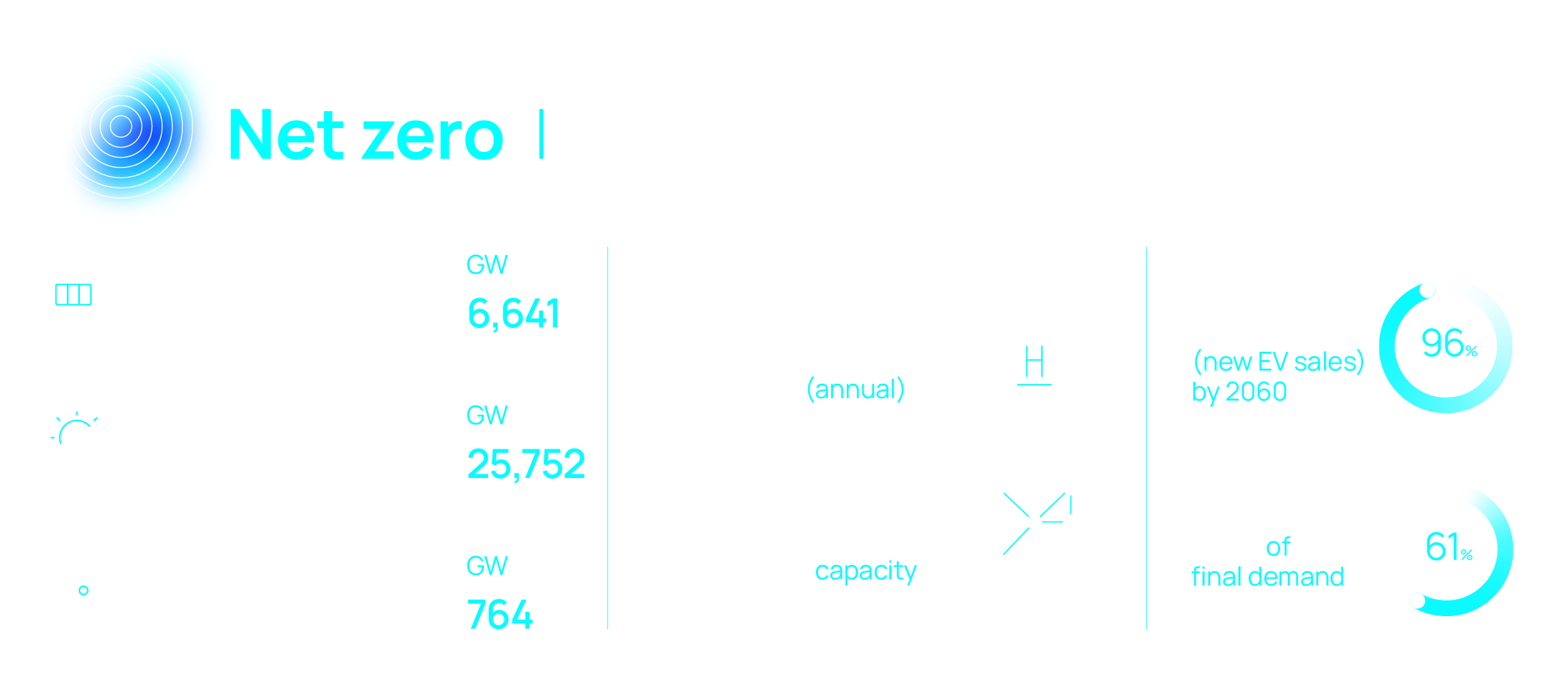

Fossil fuels become redundant

Efficiencies lower global energy demand. Policy and pricing make cleaner alternatives the default choice over oil and gas.

Renewables rule

Clean energy runs the core supply, with other generation used only for balance.

Hydrogen, CCUS and bioenergy earn their place

Where electrification is challenging, full-scale adoption of bioenergy, carbon capture and hydrogen displace remaining emissions.

Capital shifts decisively into clean energy

Clear policy signals unlock investment across the value chain.

Global cooperation not optional

Alignment on scaling finance and new technology development critical to meeting targets.

Ambitious policy powers the transition

No more soft targets. Carbon pricing, ICE bans and accelerated coal exits drive the transition.

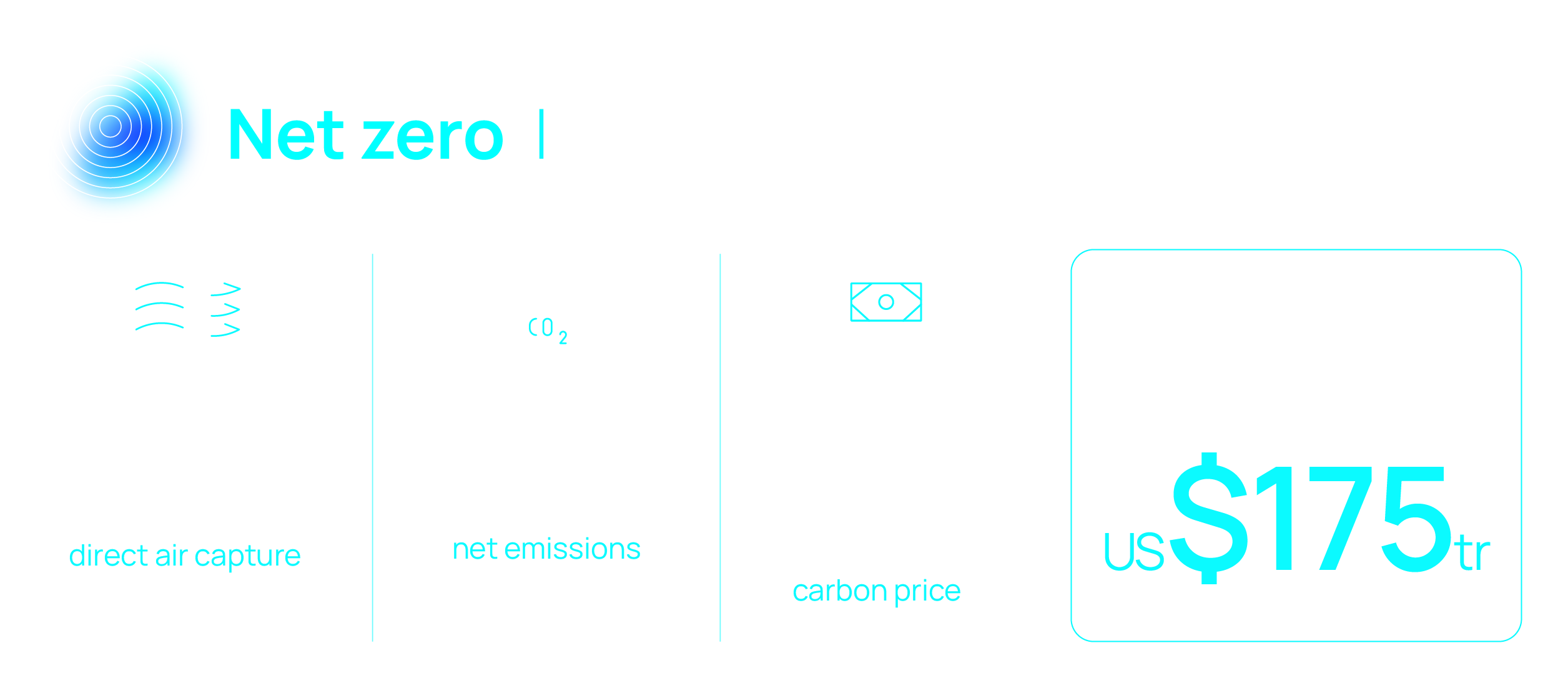

Globally, net emissions peak in 2025 and reach -7.8 Gt CO2e by 2060.

Achieving the ultimate end goal of net zero scenario requires cumulative capex spend of US$175 trillion to 2060.

Our energy transition outlook executive summary includes more analysis of these themes and the evolution of the energy and natural resources landscape across all four energy transition scenarios.

Fill in the form at the top of the page to get your complimentary copy.

Our assessment of the most likely outcome, corresponding to 2.6˚C warming, under evolution of current policy and technology trends.

Learn moreOur view of how countries' existing long term emissions targets are achieved, roughly in line with a 2˚C warming trajectory.

Learn moreA five-year delay in decarbonisation efforts due to geopolitical volatility and policy direction, with a 3.1 °C pathway.

Learn more