Can the rest of the world repel China’s magnetic pull over rare earth metals?

Relentless supply chain investment has been by design, not accident

1 minute read

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

Latest articles by Gavin

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

Opinion

Why US Henry Hub natural gas prices are set to rise | Webinar replay

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

China’s dominance of energy transition raw materials and manufacturing is well understood. Beijing has spent billions increasing its production of the five essential energy transition metals - copper, aluminium, nickel, cobalt, and lithium – and clean energy hardware. Today, China accounts for over 30% of global cobalt and lithium supply, while around half of all wind turbines and two-thirds of the world’s solar panels are manufactured in China.

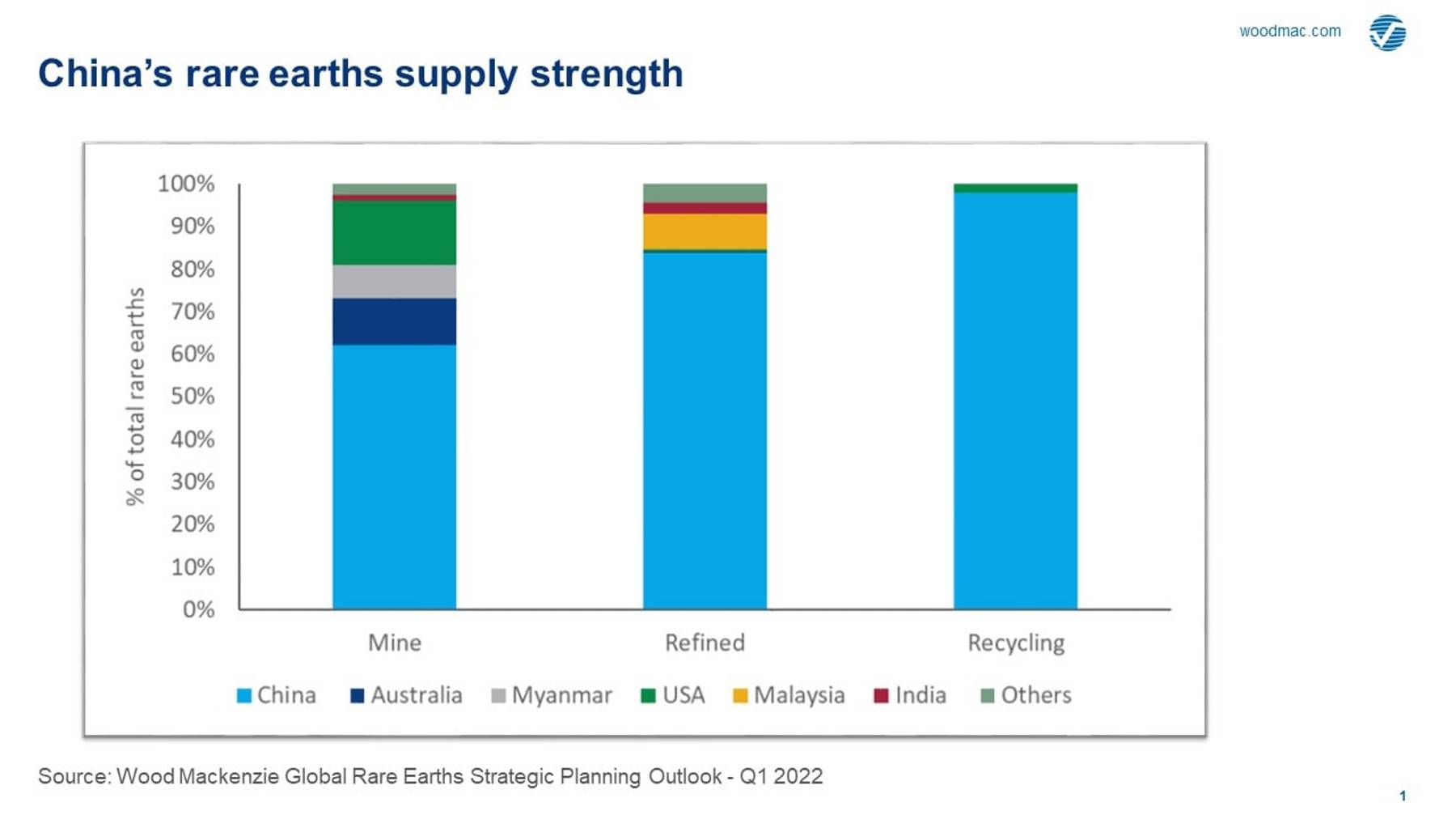

Impressive, but not a patch on what the country has achieved with rare earth metals. Critical to the production of high-strength permanent magnets that are indispensable in many energy transition technologies, China accounts for 62% of global rare earth supply and 84% of rare earth processing capacity. Secondary production of rare earths from recycled sources is almost entirely derived from China.

And it doesn’t stop there. Around 95% of high-strength rare earth permanent magnets are manufactured in China. By investing across complex supply chains, Chinese companies have integrated rare earth mining, processing, metal production and magnet manufacturing, allowing China to then dominate high value-add sectors including drivetrains for electric vehicles and generators for wind turbines.

Which rare earth metals are needed for the energy transition? How has China’s position been achieved? And can the rest of the world realistically expect to compete? I spoke to David Merriman, director of rare earth metals research, to get the hard facts.

In the energy transition, not all rare earths are created equal

Despite their moniker, rare earth elements are relatively plentiful – cerium, for example, is as abundant as copper. In addition, of the 16 rare earth elements, not all are needed in equipment to produce or use low carbon energy. For this, it is neodymium, praseodymium, dysprosium, and terbium that are really in demand, given their use in permanent magnets for electric vehicles and wind turbine generators. Most other rare earth elements remain in oversupply.

In the production of these four rare earth elements, China is king. China Northern Rare Earth Group’s Bayan Obo operation, for example, is the largest producer of both neodymium and praseodymium, contributing almost half of the global output of these two rare earths.

{kind=link}

Supply chain integration at the core of China’s dominance

China’s unrelenting rare earth value chain investment is by design, not accident. This is being forged through a clear strategy that initially began with the production of rare earths but has long since moved to integrating supply and refining with high value-add manufacturing within its own borders. For China’s leadership, energy independence and decarbonisation are inseparable: state-backed investment in rare earths is just one part of a broader plan to reduce reliance on others while dominating the resources and technologies the world needs to meet its carbon goals.

To achieve this, China is morphing from the largest producer and refiner of rare earth elements, to being the world’s dominant high value-add manufacturer of the clean energy products dependent on these metals. This is China’s ‘dual circulation’ policy in action, and progress has been both swift and decisive.

What can the rest of the world realistically do in response?

Concerns about China’s control over rare earths are not new, but is it possible to break such a commanding supply chain, particularly if costs in markets such as the US, Europe and Japan are significantly higher?

We do see that opportunities exist, particularly as China moves further downstream. Just a decade ago, China accounted for over 97% of both rare earths mined supply and refined output. This has since fallen to 63% and 84% respectively, mainly due to governments around the world responding to fears over Chinese dominance and the potential for market disruption.

Chinese rare earth producers could also face mounting ESG challenges as scrutiny by downstream purchasers and lenders increases. Plans by a consortium of European companies to establish a blockchain tracking system for rare earths could raise pressure on Chinese producers and potentially encourage alternative supply if China decides not to participate.

But looking beyond rare earth production, the outlook for those trying to compete with China remains challenging. This will require re-thinking the rules of the game – or at least trying to replicate the Chinese model, likely with state-backed projects less contingent on immediate shareholder returns. One example is the Lynas rare earth project in Western Australia, with the company producing neodymium and praseodymium from its Mt. Weld mine and then shipping them to Malaysia for processing. The project is almost 100% financed by a government-backed Japanese consortium, with upfront financing on flexible terms and output dedicated to Japan’s magnet market.

Another option is removing the need for rare earths all together. Not all energy transition technology requires rare earths, but while induction motors and rare earth-free permanent magnets offer alternatives, they aren’t a ‘get out of jail’ card for the rest of the world. Using these technologies on a large scale will drive demand and prices for other energy transition metals, including copper.

As others look to catch up, China is already moving on

As governments increase support, more supply projects outside of China are now expected to move forward. As a result, China’s share of global rare earth supply is likely to fall to around half by 2050 as mines in Australia, the US, Africa and elsewhere progress. A ray of light, perhaps, but with a catch: with China dominating the rare earth processing market, the bulk of rare earths mined elsewhere will still be sent to China for processing and value-add manufacturing.

With energy security now at the top of the western political agenda following Russia’s invasion of Ukraine, attention could soon shift from reducing dependence on Russian hydrocarbons to reducing dependence on Chinese clean energy technology. But China isn’t Russia: with its supply chain strength and a huge domestic market to fall back on, any attempt to compete through tariffs (or even sanctions) on Chinese manufacturing could backfire if countries deny themselves access to the technology needed to decarbonise.

China’s dominance over energy transition rare earths is a compelling case for first mover advantage. As Julian Kettle, Wood Mackenzie’s senior vice president for metals research, succinctly puts it, "in the critical raw material restaurant, China is eating its dessert while the rest of the world is reading the menu."

Check out our Rare Earths Research Suite to find out how we can help your business.

APAC Energy Buzz is a weekly blog by Wood Mackenzie Asia Pacific Vice Chair, Gavin Thompson. In his blog, Gavin shares the sights and sounds of what’s trending in the region and what’s weighing on business leaders’ minds.