Discuss your challenges with our solutions experts

Can North American Independents remain internationally diversified?

We discuss how to find the optimal balance for future investments

1 minute read

As the oil sector starts to stabilise following the turbulence of the past three years, many companies are revisiting their portfolios and operating strategies to consider what the optimal balance will be for future investment.

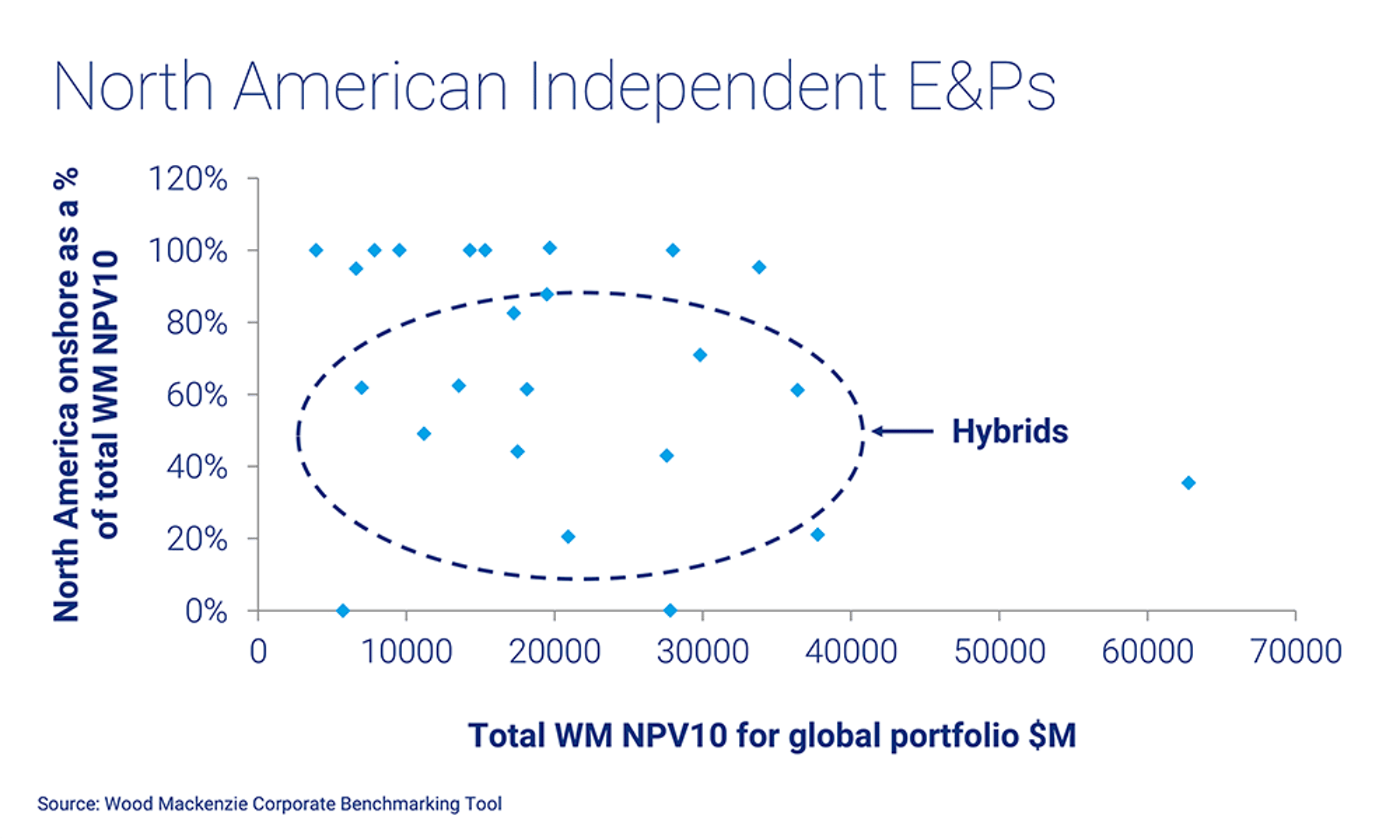

One of the company peer groups that potentially faces making the biggest decisions is the North American Independent E&Ps, having historically adopted a "hybrid" business model.

In the current market environment, two distinct business models and opportunities for investors have emerged:

- The North America onshore "drilling factory", with successful players having assets towards the lower-end of the global oil supply cost curve.

- The international "conventional" approach which, depending on the scale of the specific player, is typically focused on offshore production in a range of geographies with 4-5 year development lead times. Though there are exceptions, many of the future development assets are positioned in the upper-middle or upper end of the global oil supply cost curve.

Both operating models lack many natural synergies, but the investment patterns and legacy asset base of some companies — specifically the North American Independent E&Ps — have resulted in their portfolios adopting a hybrid approach.

{kind=link}

How could the hybrid model change the industry landscape?

Thinking about how the industry could potentially evolve over the next three to five years raises two questions:

- Will this hybrid model continue to flourish given the market’s expectation that the oil price will remain lower (say US$50-70/bbl) than prior to 2014?

- Five years from now, will a significant number of these "hybrids" have evolved their company structure to create a standalone onshore North America entity by spinning off, merging or selling their international operations?

Should creating a standalone North Americas entity be the more attractive option, management teams will need to carefully weighup several key factors.

These include comparing the relative size, growth potential and cash flow profile of the North Americas portfolio, testing whether the international/conventional portfolio could function as a standalone entity or if the scale, growth outlook and cost competitiveness of the North Americas business unit is sufficiently attractive that the business would be valued at a premium once it becomes a pure-play.

What are the potential implications for the broader E&P market?

If a subset of these hybrids refocus on a “pure-play” North America asset base, this will have consequences for the wider E&P market.

From the US perspective, the move would be readily accepted. There is a large existing “Lower 48” E&P sector ranging from <US$1 billion to >US$30 billion in market capitalisation. Investors have a relatively sophisticated understanding of the business model and key performance indicators for the peer group, and the underlying medium-term growth thesis is well established.

Taking an international view, the implications are less clear. Would the international assets (US$50-US$100 billion in aggregate across the peer group) enable the establishment of a new wave of Independent E&Ps, perhaps with mergers playing a role to enable sufficient scale and diversity?

Or is an outright sale of the assets (either in a package or through a series of transactions) a clearer route to maximise value? This could provide a natural buying opportunity for NOCs and other players who are interested in large-scale opportunities to reposition their portfolios through M&A.

Stepping back from the argument for “pure-plays”, is there a risk of companies becoming opportunity-constrained at any point if they focus exclusively on Lower 48 investment opportunities? This seems like a remote prospect from a resource perspective but, as more companies ramp up investment levels in Lower 48 plays, the ability to secure attractive full-cycle returns (including cost of acreage acquisition) is likely to come under pressure.

Investment patterns in the oil and gas industry typically ebb and flow over long periods of time and it is normal to see some contrarian behaviour within a group of companies. So, while it is likely that we will continue to see a gradual drift towards pure-play Lower 48 and international players in the mid-cap E&P sector, we expect some companies will continue to take the view that the hybrid model provides an attractive balance of risk and reward for their investors.