Copper rush: A strategic analysis

Diversify or go pure play?

4 minute read

James Whiteside

Director, Head of Corporate Research - Metals & Mining

James Whiteside

Director, Head of Corporate Research - Metals & Mining

With 15 years of experience in the metals and mining industry, James leads our corperate coverage.

View James Whiteside's full profile

Afdal Saheed

Senior Analyst, Corporate Research

Afdal Saheed

Senior Analyst, Corporate Research

Afdal has been building our metals and mining Corporate Service coverage since joining Wood Mackenzie in 2022.

Latest articles by Afdal

-

Opinion

The end of capital discipline in mining?

-

Opinion

Copper rush: A strategic analysis

-

Opinion

Diversified mining: will capital allocation strategies continue to provide predictable investor returns?

Stuart Ogilvie

Head of Corporate Research Sales

Stuart Ogilvie

Head of Corporate Research Sales

Stuart's focus is on helping companies utilise our Corporate Strategy and Analytics Services to make informed decisions

Latest articles by Stuart

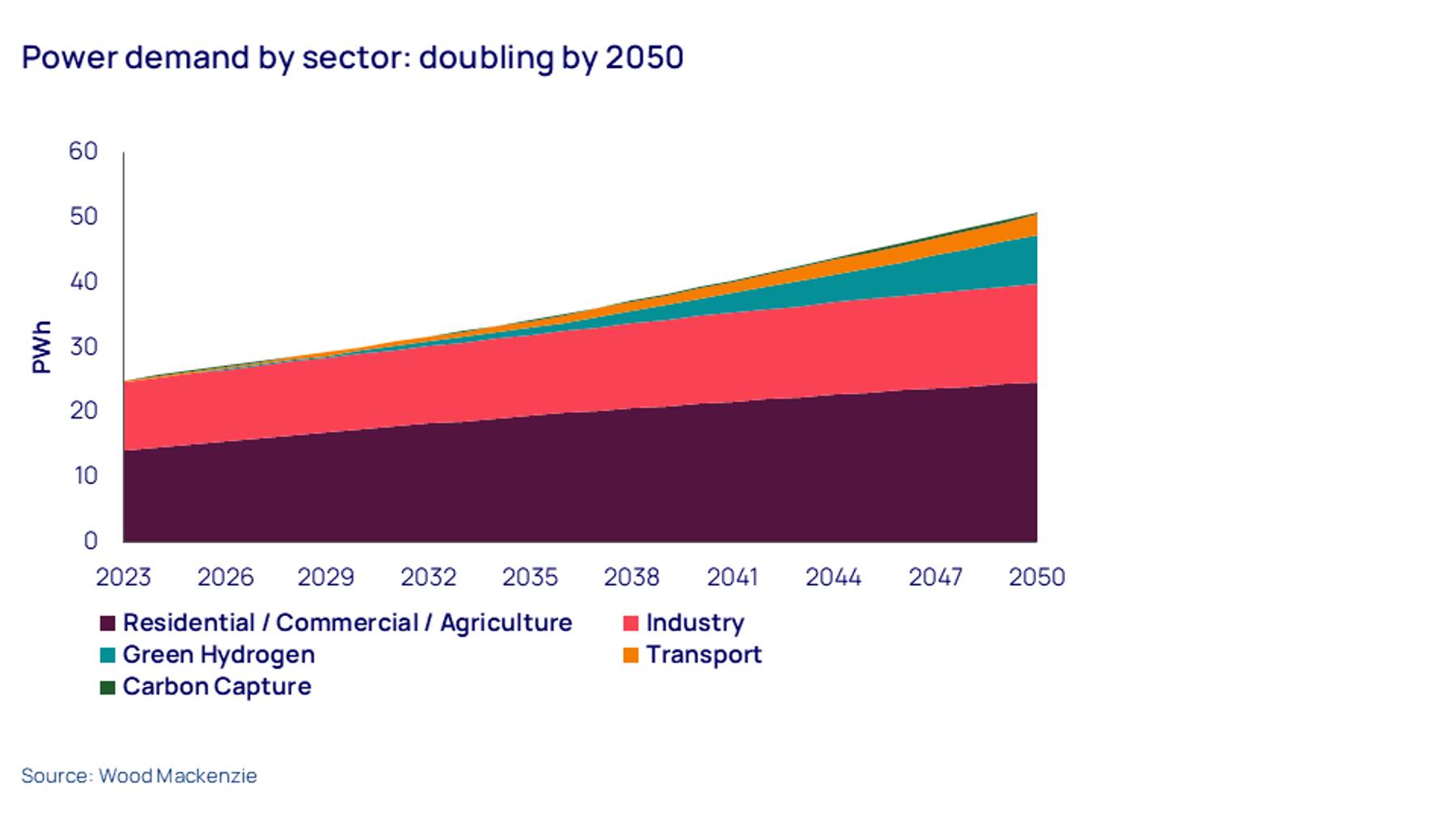

View Stuart Ogilvie's full profilePower demand is set to double through 2050. This will happen amid a shift away from fossil fuels and thermal generation capacity and a move towards more renewable power. Much of that renewable power generation is copper-intensive ‒ indeed, electrification cannot happen without it.

Wood Mackenzie’s Corporate Strategy & Analytics Service recently held a webinar entitled Copper Rush: Diversify or go pure play? exploring how valuations, carbon footprints, and balance-sheet health will shape the merger and acquisition (M&A) strategies and corporate plans of both diversified miners and pure-play copper companies. Fill in the form to receive a complimentary recording of our webinar and read on for an introduction to our discussion.

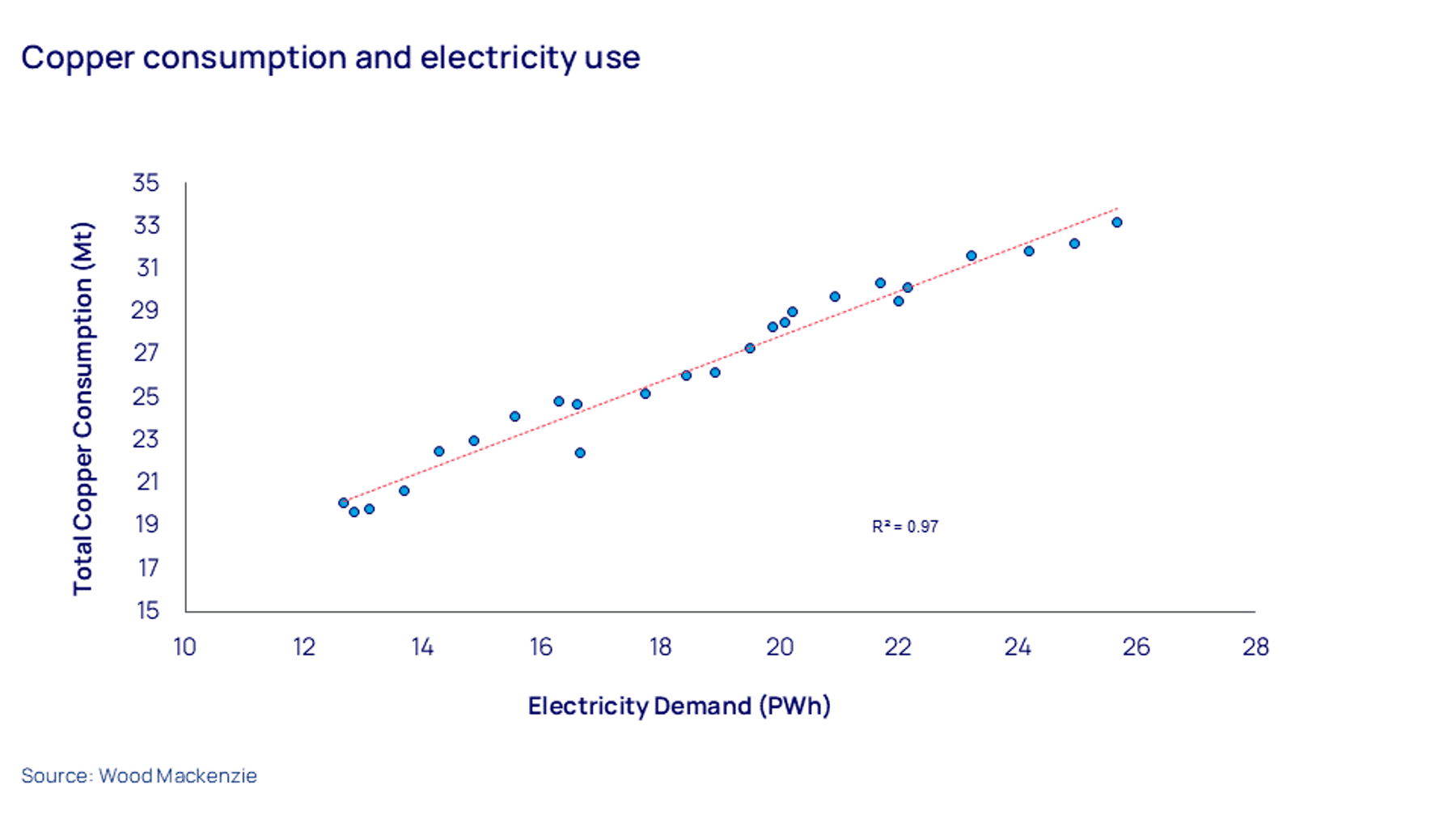

Copper consumption set to almost double

Around 90% of the world’s copper's consumption is intrinsically linked to its property as an electrical conductor. Consequently, we also expect copper consumption to nearly double through mid-century. That’s equivalent to growth of around 2% per annum.

The demand for copper is set to stem from a range of sub-sectors – construction, transport, the electrical network, industrial machinery, other appliances, and goods and services. We see transport, for example, growing from around about 10% of the current copper end-use market to close to 20% over the next 10 years. What’s more, as the world electrifies and builds out new power-generation capacity, that electricity will have to be transmitted and distributed through an electrical network.

This is a solid foundation for the growth of copper, which means that new mine projects will be required to meet future supply needs. On a 10-year time frame, that's something like 5 million tonnes of copper; under a net zero scenario, it could be closer to 9 million or 10 million tonnes.

Major-league opportunities

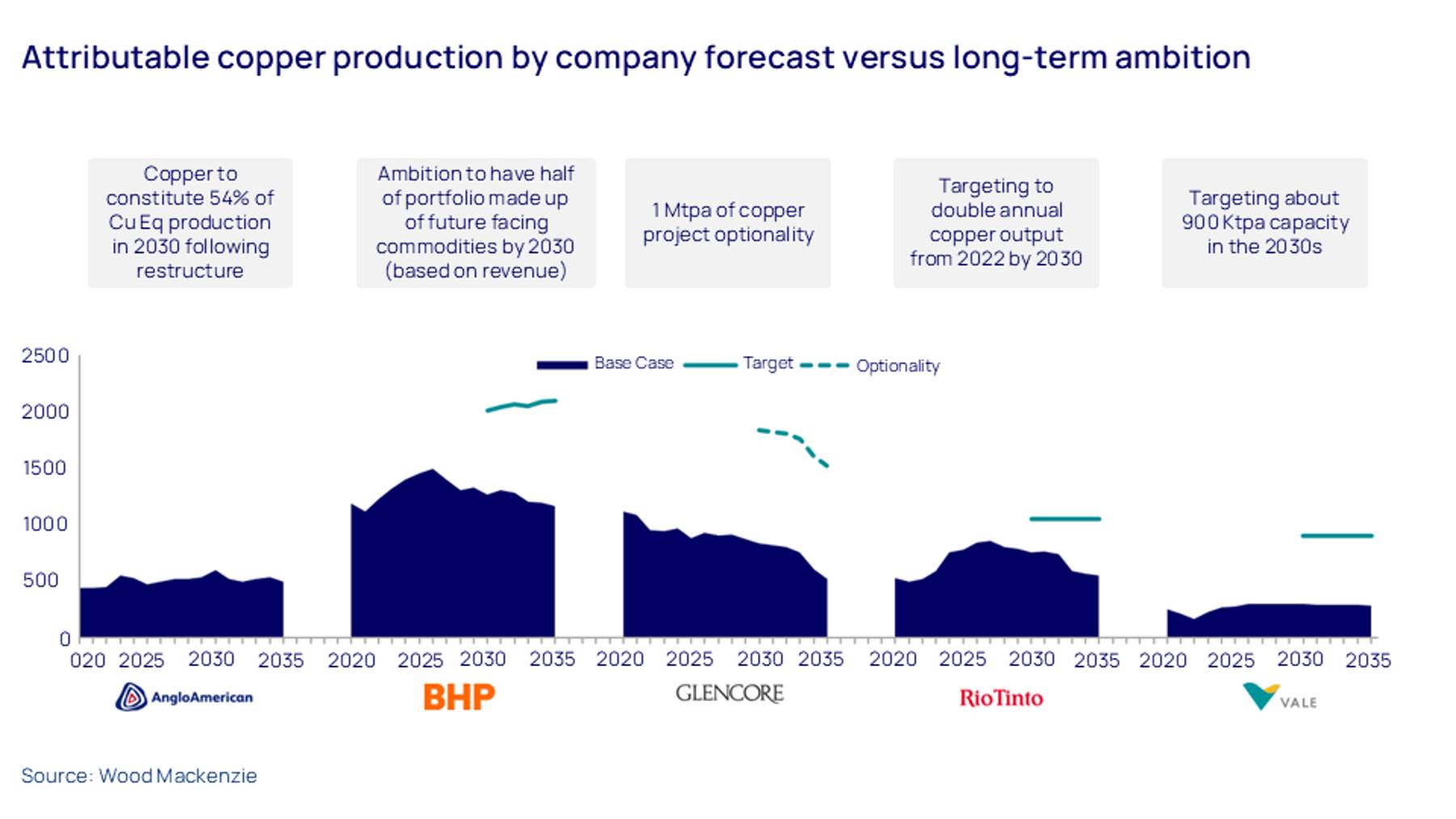

Wood Mackenzie has examined how the major mining companies are forming their strategies around this opportunity, looking at things such as diversification, value delivery and strategic merit.

Companies are increasingly seeking to expand their geographical footprint, and that's both to mitigate fiscal risks and to secure growth opportunities outside of some of their mature and declining asset bases in traditional jurisdictions. Such copper opportunities exist in Africa and parts of South America ‒ still very much frontier markets in terms of the potential for copper

growth and diversification for some of the majors. There are numerous assets out there that could be transformative in terms of scale for their portfolios, however.

Value delivery involves a company’s ability to enter a market at an attractive valuation, but also the ability to generate meaningful earnings throughout the commodity cycle. For some, current copper valuations could pose a challenge.

In terms of strategic merit, companies need to consider how well a commodity aligns with their core competencies and strategic direction. Copper's potential to enhance corporate valuation and its durable outlook make it a compelling choice right now and a highly attractive option for the majors.

{kind=link}

{kind=link}

{kind=link}

The value of copper exposure

Copper-focused miners are currently trading at a significant premium in terms of EV/EBITDA relative to their diversified peers, and the market is placing far higher value on companies with concentrated copper exposure.

The diversified miners are trading at around 4x-6x EBITDA over the next 12 months, close to a typical through-the-cycle multiple. Copper miners, meanwhile, are receiving growing value recognition, and are now valued at about 8x-12x earnings, up from about 6x-10x only two years ago. Dividend yields have been similarly buoyant.

So what is driving this trend? The root cause is growing recognition of copper's robust earnings outlook relative to other commodities. On the back of this, diversified miners are seeking to capitalise on the potential value uplift associated with getting that exposure to the energy transition theme.

What we have seen, however, is that companies with a significant portion of steel raw material in their portfolios have not experienced the same value recognition, probably due to concerns about the longevity of some of those commodities and Scope 3 emissions. It is also questionable whether an iron-ore major with significant copper exposure can truly overcome those challenges and gain that valuation uplift. This creates a unique set of environmental and commodity-market considerations that could limit valuation upside.

Another aspect to the uplift in copper valuations is the obstacles it creates to M&A. The higher valuations make share-based purchases excessively dilutive, limiting the opportunities for

corporate acquisitions in the copper space. Still, copper doesn't come with the same emissions baggage as some commodities, so the scale of ambition in the copper market remains higher than in any other commodity.

To learn about the expansion options available to the copper majors, to find out whether they make sense from an economic perspective and much, much more, fill in the form to receive a complimentary recording of our webinar.

Wood Mackenzie Corporate Strategy and Analytics Service

With greater complexity and connectivity across the energy value chain, organisations need to continually evaluate their strategies and portfolios, as well as those of their competitors.

Whether analysing risk associated with capital allocation, benchmarking competitor strategies, or looking to develop more sustainable practices through the energy transition, organisations need reliable data combined with industry-leading insights.

Wood Mackenzie's Corporate Strategy and Analytics Service provides unrivalled data-driven analysis to gain a deep understanding of a company or peer group’s strategic, operational and financial motivations across the oil and gas, power and renewables, and metals and mining sectors.