Floating LNG is back in vogue

Lower costs and increased demand for quick-to-market LNG supply has made floating LNG (FLNG) an attractive proposition again

3 minute read

Fraser Carson

Principal Research Analyst, Global LNG

Fraser Carson

Principal Research Analyst, Global LNG

Fraser has extensive research and project management experience across the LNG value chain.

Latest articles by Fraser

-

Opinion

The great LNG shipping reset: how geopolitics is rewriting maritime energy rules

-

Opinion

The methane myth: why US LNG still beats coal in the emissions race

-

Opinion

Video | Lens Gas & LNG: Golar and partners' FID set to revive Argentina's LNG export ambitions

-

Opinion

Transforming energy: 5 key questions ahead of Gastech 2024

-

Opinion

The US broadens sanctions against Arctic LNG-2

-

Opinion

Hoegh Galleon helps Egypt’s gas crunch but delays Australian LNG imports

Investor interest in FLNG is back. 8.5 mmtpa of FLNG capacity was sanctioned last year. Currently, 12.5 mmtpa is under construction and by 2026 almost 25 mmtpa of floating supply will be operational. And the story isn’t finished yet. International oil companies (IOCs), upstream producers and midstream specialists are all moving projects towards FID.

But FLNG has its challenges. A simple, fast-to-market solution is every developer’s dream. This can be achieved with FLNG, but not in every situation. The requirement for gas processing or difficult metocean conditions can quickly add complexity and increase costs.

Our latest Global FLNG overview leverages Wood Mackenzie’s unrivalled LNG, upstream and economic expertise to provide a detailed breakdown of the key drivers behind FLNG’s resurgence.

Fill out the form to get access to a complimentary extract and read on for an introduction.

Why is FLNG back in favour ?

FLNG has a chequered history. Projects suffered from considerable delays and cost overruns. The concept has also been plagued by poor reliability. And facilities have been forced to move locations. These factors should make investors cautious.

So, what’s changed?

-

Reliability has improved

After a stuttering start, FLNG is proving to be a reliable commercialisation option. The utilisation of FLNG facilities in Cameroon and Malaysia have been strong over the last year, with the units producing at close to or above 100% capacity.

-

Construction schedules are being met

Coral FLNG, which shipped its first cargo in November 2022, was successfully delivered on time and on budget. Similarly, the under-construction Gimi FLNG has experienced minimal delays and is expected on site in offshore Mauritania/Senegal next year.

-

New fast-to-market LNG supply is more valuable than ever

Europe has rapidly shifted away from piped Russian gas towards the global LNG market, intensifying competition for the limited supply that’s available. There is limited near-term supply growth. And with onshore LNG taking an average of four years to develop, demand is strong for new projects that can be brought online quickly.

• FLNG is cost-competitive

The generally lower capital costs associated with FLNG are attractive to investors. With standardised designs, indicative costs for the FLNG unit can be derived. Golar’s conversion designs, such as the MkII Gimi for Tortue Phase 1, can be as low as US$550/tonne, while SHI’s and WOM’s newbuild orders for ZLNG and Marine XII are both around US$750/tonne. This compares favourably to onshore LNG plant capex, which is currently around US$900/tonne for US Gulf Coast projects.

-

Increased accessibility

The initial, challenging experiences of FLNG project development have generated strong demand for a simplified approach. Shipbuilders like Wison and Samsung now offer standardised newbuild FLNG designs, available for a range of production and storage capacities. Golar offers three standard FLNG designs, two conversions and one newbuild option. New Fortress Energy is developing the liquefaction modules for its Fast LNG designs with a fixed capacity that can be scaled up.

Where will FLNG growth come from?

{kind=link}

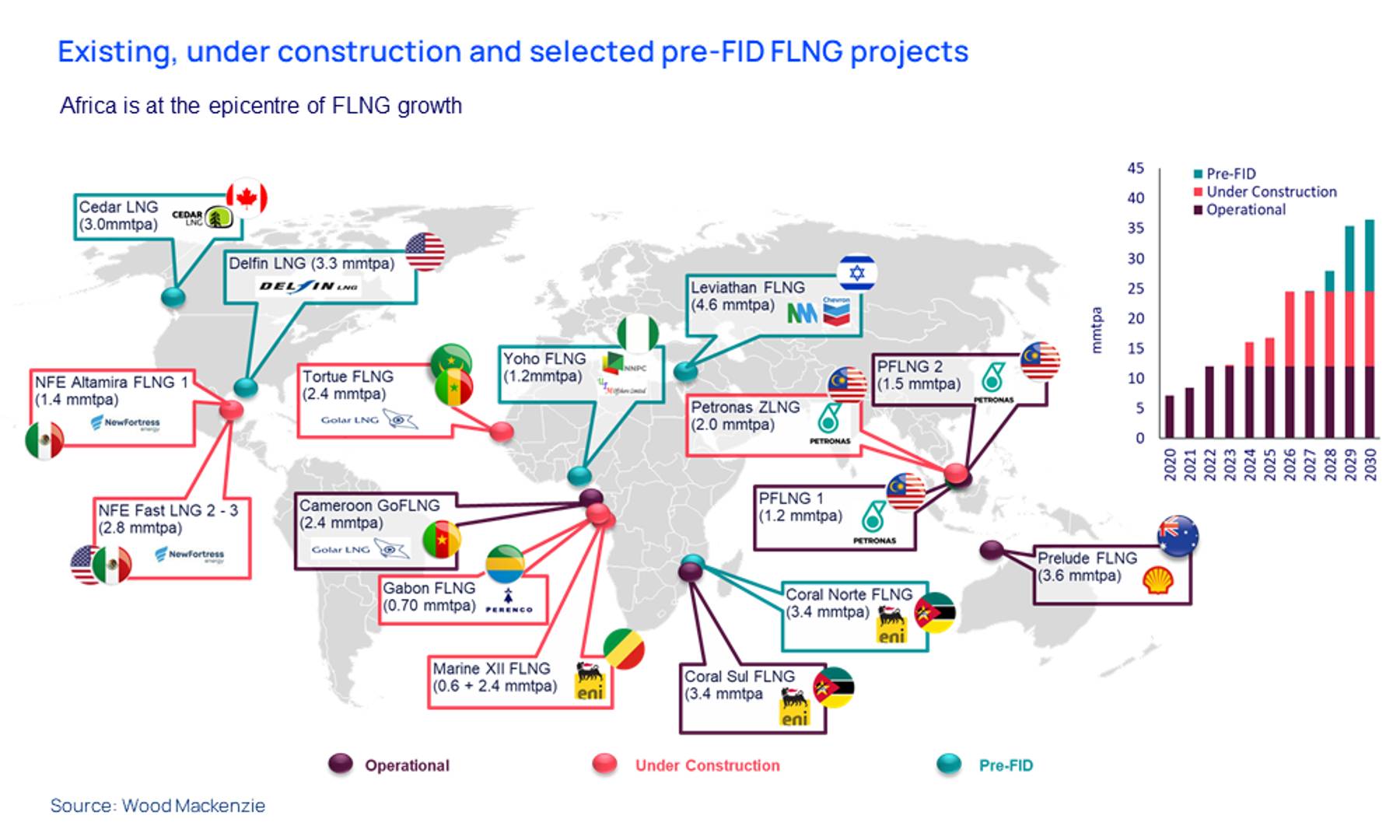

Africa has been at the epicentre of FLNG momentum. In recent years, resource-rich markets have faced challenges developing gas for export, including from armed insurgency and infrastructure sabotage. FLNG is removed from these above-ground risks. It also provides African producers with an alternative to supplying the domestic market.

Within the last year, experienced FLNG developers Eni and Perenco sanctioned a two-phase floating development in Congo and a barge-based project in Gabon, respectively. But new entrants, such as UTM offshore and NNPC, are also considering FLNG to develop Nigeria’s stranded offshore volumes. In East Africa, FLNG continues to be linked as a potential development option for the Rovuma partners.

Outside of Africa, NewMed Energy and Chevron have confirmed Leviathan FLNG’s design concept and are targeting an FID on the Israeli project in 2024. Recent large gas discoveries by the Majors in Cyprus could also lend themselves to FLNG. In North America, Delfin LNG and Cedar LNG have both made considerable commercial progress over the last 12 months, while New Fortress Energy has now sanctioned three of its Fast LNG fixed platform units.

FLNG is not without risks. That said, we estimate that up to 20 mmtpa of new FLNG capacity will be sanctioned over the next two years. This will primarily be developed in markets where there are concerns of cost blowouts, scheduling delays and security risks.

Our latest Global FLNG overview explores the opportunity – and the risk – in detail. Fill in the form at the top of the page for a complimentary extract.