LNG trade disrupted as Suez Canal transits stop

The implications of no LNG carriers transiting through the Red Sea and Suez Canal

2 minute read

Fraser Carson

Principal Research Analyst, Global LNG

Fraser Carson

Principal Research Analyst, Global LNG

Fraser has extensive research and project management experience across the LNG value chain.

Latest articles by Fraser

-

Opinion

The great LNG shipping reset: how geopolitics is rewriting maritime energy rules

-

Opinion

The methane myth: why US LNG still beats coal in the emissions race

-

Opinion

Video | Lens Gas & LNG: Golar and partners' FID set to revive Argentina's LNG export ambitions

-

Opinion

Transforming energy: 5 key questions ahead of Gastech 2024

-

Opinion

The US broadens sanctions against Arctic LNG-2

-

Opinion

Hoegh Galleon helps Egypt’s gas crunch but delays Australian LNG imports

Since mid-December, LNG traffic through the Gulf of Aden and Red Sea has steadily reduced due to conflict in the region. Global trade and commodity markets have been disrupted due to Houthi terror attacks on merchant vessels. This has prompted shipowners and operators to divert ships, reducing utilisation of the Suez Canal.

Our latest insight LNG trade disrupted as Suez Canal transits stop summarises the implications to LNG trade of no LNG carriers transiting the Red Sea and Suez Canal. Read on for a summary.

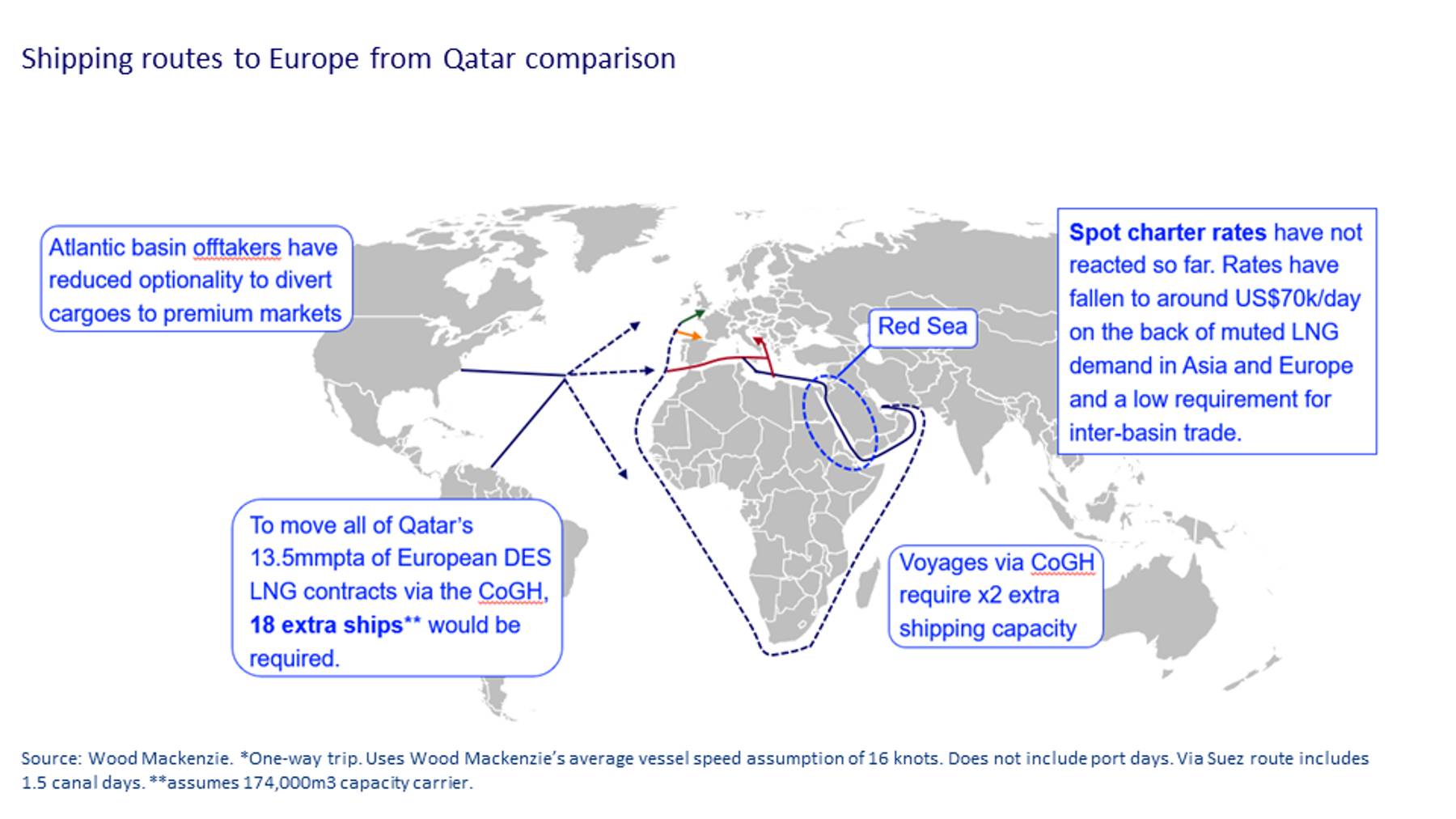

The Suez Canal is utilised by several LNG suppliers and deliveries into both Europe and Asia will be impacted. Russian LNG, often after being transhipped in Belgium and France, accounted for 25% of all laden cargoes transiting the Canal southbound to Asia between 2021 - 2023. Over the same period, US LNG recorded close to half of all laden transits travelling in the same direction. Going the other way, towards Europe, Qatar LNG accounted for more than 90% of laden, northbound voyages, averaging 220 transits over the last three years. For all concerned, non-utilisation of the Suez Canal will mean longer journeys over a greater distance. But we think it is unlikely to impact LNG shipping demand and spot rates in the near-term.

Atlantic basin LNG, especially from the US, will be affected. Amidst recent global gas price volatility, traders and portfolio players have increasingly directed FOB cargoes towards the Mediterranean area, as the Suez Canal provides optionality to deliver into Asia. Cargoes can spend several days slow steaming while waiting on their final delivery destination. Without that option, ships will spend less time waiting for direction and will deliver straight into Europe or deliver into Southern Asia via CoGH. The slightly longer journey time into South Asia will be offset by the more direct voyages - a result of less trading being taken ‘on the water’.

{kind=link}

Qatar will be impacted most. To continue delivering into these markets, Qatari ships will travel to Europe via the Cape of Good Hope (CoGH), adding up to 8,000 nautical miles to the journey each way. Assuming use of a standard 174,000m3 capacity LNG carrier travelling at 16 knots, a round-trip voyage will take an extra 24 - 38 days - the equivalent round-trip journey time to deliver from Qatar to Europe via Suez. Effectively, Qatari LNG deliveries to Europe will take twice as long. To move all of Qatar’s European DES contracts via the CoGH, we estimate that the equivalent of 18 extra ships would be required.

The additional journey time will require some re-scheduling of cargoes and management with its LNG buyers, but its supply to Europe will not be constrained by a lack of shipping.

Furthermore, European and Asian LNG inventories remain well supplied, in the upper range of five-year averages. Despites some cold snaps, winter weather has not resulted in a significant drawdown of stocks or an increased demand for prompt LNG. With solid nuclear generation keeping demand in South Korea and Japan muted, and Chinese LNG demand remaining close to contracted levels, the requirement for cross-basin trade is expected to be low for the rest of the winter. This, combined with Qatar managing the extra shipping demand from within its fleet, will keep a pin in LNG shipping spot rates into the spring.