Sign up today to get the best of our expert insight in your inbox

Global economy maintains momentum after upside surprise

The global economy is expected to grow at a decent clip again in 2024 – but downside risks have escalated since our last quarterly update

3 minute read

Peter Martin

Vice President, Head of Economics

Peter Martin

Vice President, Head of Economics

Peter is responsible for our global economic outlook to 2060.

Latest articles by Peter

-

The Edge

Will falling populations reshape energy demand?

-

Opinion

Horizons Live: Strait talking | Webinar replay

-

Opinion

Investing for the long term: quantifying the economic costs of an accelerated energy transition

-

Opinion

European gas: 6 Q&As on prices, supply, and regulatory impact

-

Featured

Metals & mining 2026 outlook

-

Opinion

Tariffs, trade and technology: the macro forces shaping metals markets

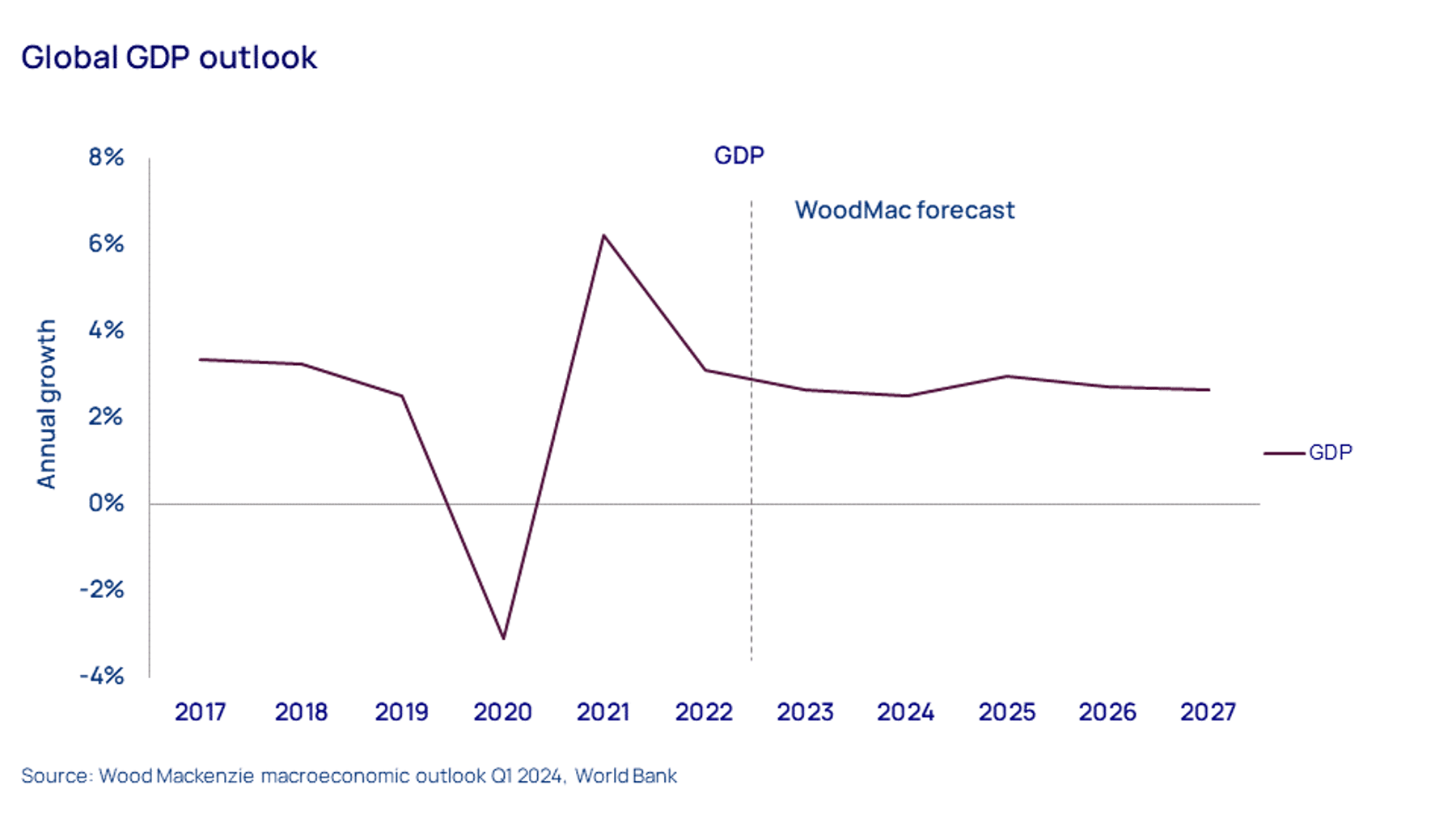

The global economy surprised to the upside in 2023 but still slowed to 2.6% GDP growth from 3.1% in 2022. A resilient and strong US economy helped global growth and defied the gloomy sentiment as China’s recovery faltered.

Cautious optimism remains. After a soft start to the year, we expect the global economy to grow at a decent clip again in 2024, 2.5% year on year. But what factors are shaping this view? Where are the potential growth hotspots – and what are the risks? Visit the store to read the Global economic outlook in full, or read on for a few highlights.

{kind=link}

A pivot to investment is key to our global growth forecast

To maintain momentum, it is imperative to accelerate investment as consumption growth moderates in major economies. This pivot to investment will be helped by monetary easing – the Federal Reserve, ECB and the Bank of England are all expected to begin cutting rates this year.

Interest rate cuts are likely to come in modest increments as central banks manage the final mile of getting inflation back to target rates. Central banks will be wary that supply shocks have the potential to stoke price growth.

US economy poised for continued expansion – but a slower rate than last year

In the US, buoyed by a roaring labour market and unwinding of excess savings, consumers powered GDP growth to 2.5% last year. The US is amid the softest of soft landings.

The economy is set to continue expanding albeit at a slower rate in 2024. Staying on the soft-landing path requires investment to accelerate and sustained real wage growth as job gains inevitably diminish.

India’s stellar economic growth continues

Domestic demand – supported by the government’s capital expenditure (capex) splurge ahead of the upcoming general election in April and May – is driving strong economic performance.

Investment in infrastructure today boosts the economic growth prospects of tomorrow. Our long-term GDP growth outlook for India has been upgraded. Furthermore, if Modi’s BJP wins the elections, as we expect, a comprehensive package of reforms will complement the bullish investment outlook.

For a closer look at whether higher investment can be sustained, and how that shapes India’s long-term GDP, read the Global economic outlook in full.

China’s structural slowdown resumes

China’s GDP outlook for 2024 is unchanged from our last update, slowing to 4.6% from 5.2% growth last year. While economic growth beat the government’s modest target of 5% last year, the underwhelming expansion will have a lasting impact.

As China’s structural slowdown resumes, the economy is now on a lower trajectory, a so-called ‘L-shaped recovery’. The property sector will continue to drag on growth, but government support for social housing will offset some of the negative impact.

Infrastructure is again the main stimulus target. Autos and energy transition-related sectors will continue to be the main growth drivers in 2024.

Is Europe on the verge of an upturn?

Growth in Europe is very weak. High inflation, high interest rates, conservative consumer spending and low productivity growth have stagnated the economy. At least eight countries in the European Union, including Germany, suffered a technical recession (two consecutive quarters of economic contraction) during 2023.

With inflation moderating and rates cuts expected, we are optimistic that Europe is on the verge of an upward turning point. Albeit growth is still likely to be soft.

What are the risks to our global economic outlook?

Risks remain skewed to the downside and have escalated since the last update. Supply shocks driven by non-macroeconomic factors are the most probable: conflict escalation and further disruption to the vessels transiting the Red Sea.

Political uncertainty is high with numerous key elections slated for this year. The outcomes will determine paths for fiscal and trade policy. We’ll be monitoring changes closely.

This article draws on our Global economic outlook Q1 2024 report. To read it in full visit the store. And to get a round-up of our latest insights direct to your inbox each week fill in the form to sign up for The Inside Track newsletter.