Global upstream: the biggest topics

New regulations are in play, and costs are rising across the sector. Find out how global trends are playing out

3 minute read

Ian Thom

Research Director, Upstream

Ian Thom

Research Director, Upstream

Ian brings 18 years of experience to his role as head of regional analysis for Europe, Russian, Caspian and Africa

Latest articles by Ian

-

Opinion

Is Nigeria’s deepwater roaring back?

-

Opinion

The unstoppable rise of Africa’s upstream independents

-

Featured

Upstream-oil-gas-2026-outlook

-

Opinion

Video | Global upstream update: winter 2025

-

Opinion

Revitalisation meets frontier exploration in West Africa’s twin-track energy future

-

Opinion

Video | Lens Emissions: Africa’s oil – legacy fields vs low-carbon future

The Global Upstream Update is a regular insight produced for global subscribers to our Upstream Service. Emerging stories in this edition range from decarbonisation legislation in the UK to deepwater developments in Guyana.

Fill in the form for your copy of an extract from the report or read on for a quick introduction to three key themes our team will be tracking closely over the course of this year.

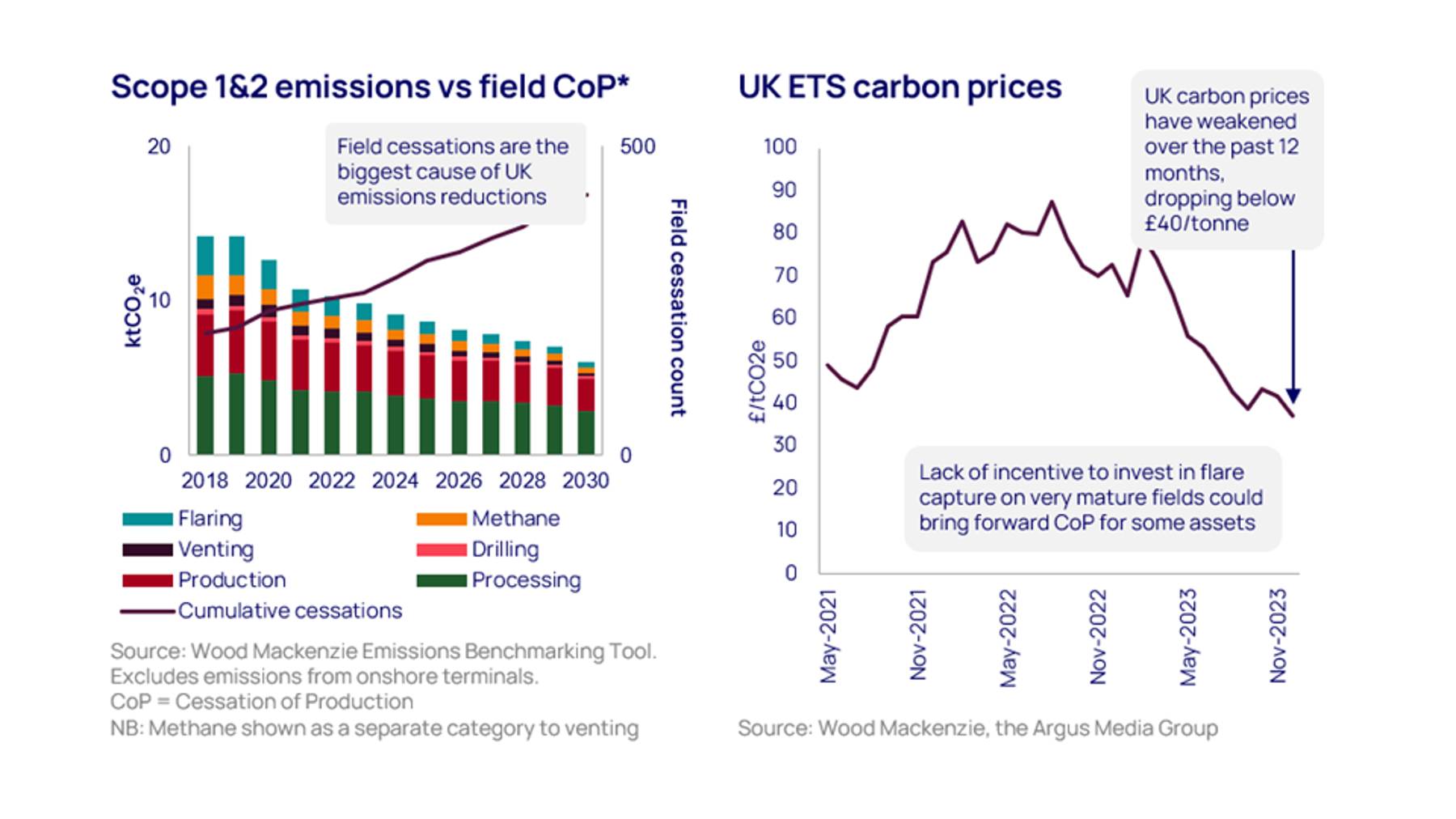

1. The UK’s tough emissions goals come with material risk

The UK regulator (NTSA) published tough emissions targets in March, and while the flexibility of the new rulings is welcome, serious knock-on effects are a possibility. The requirement to end routine flaring and venting by 2030 may present insurmountable challenges to very mature fields, and key hubs may even cease production earlier.

The regulations will impact a wide range of projects. New fields coming online after 1 January 2030 must be either fully electrified or run on alternative low carbon power with similar emission reductions. Tiebacks will be obliged to connect to hosts that are fully electrified or committed to electrification, or low carbon power to the NSTA’s satisfaction. Standalone developments onstream before 1 January 2030 should, at a minimum, come online electrification ready.

With these new targets, and a tougher Energy Profits Levy (expected if Labour wins this year’s general election), the impact on future production could be serious. Our analysis suggests that over 2 billion boe of resources could be left undeveloped, making the UK more reliant on imports.

Reduced production would also impact the economic viability of key pipelines such as CATS, SAGE and FPS. The Central North Sea is now also a crucial area for offshore wind developers, and if hubs cease early, these projects will also be under threat of cancellation.

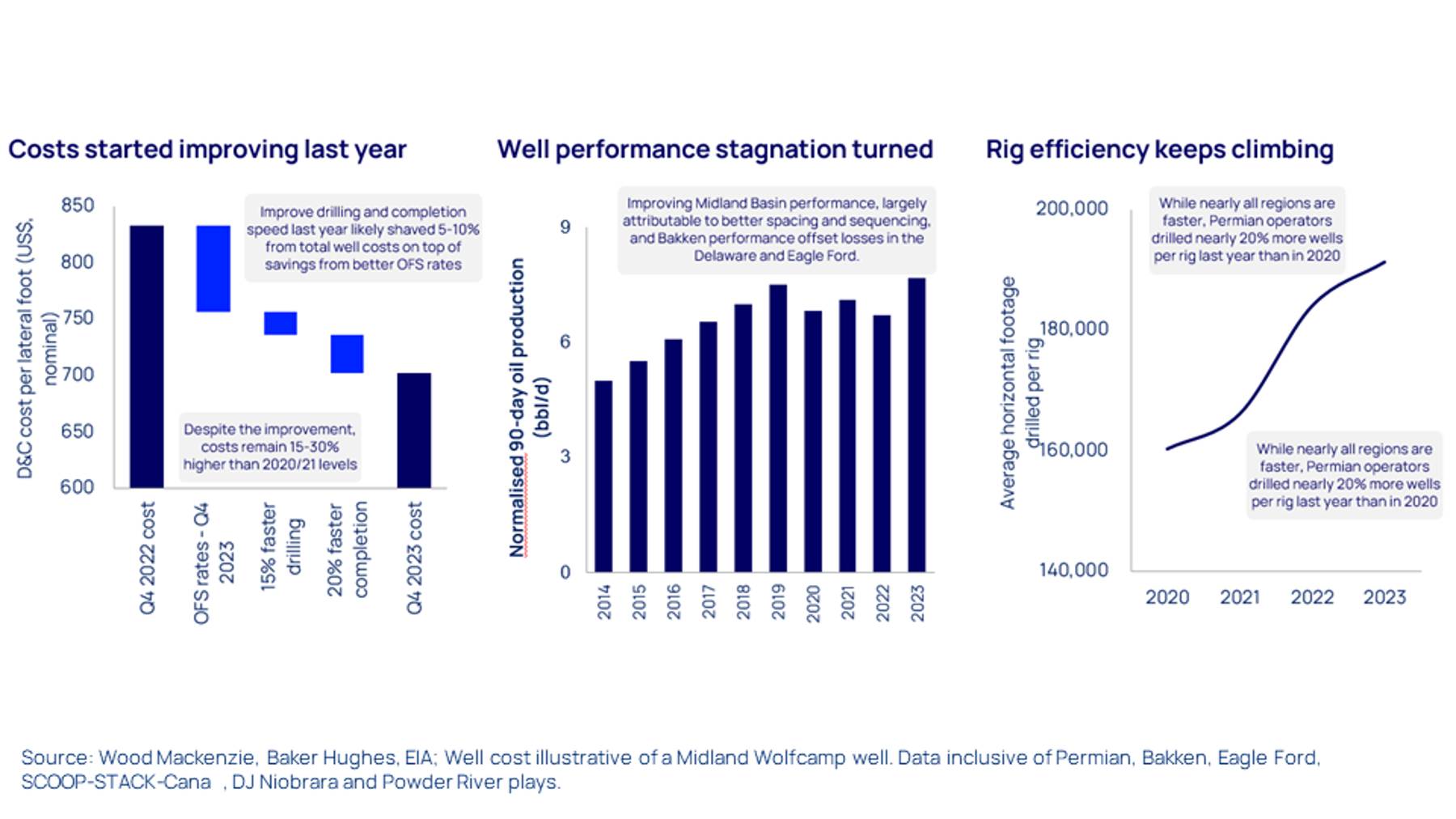

2. An unexpected improvement in US oil efficiency

When it comes to tight oil in the US Lower 48, it is now looking likely that some public investors overplayed the risks around capital efficiency erosion last year. Contrary to a trend of rising development costs (US$/boe) that began in 2020, we have recently seen costs reduced, wells performing better, and faster drilling and completion times.

With an array of more effective processes being widely put to use, like super-spec rigs, more experienced crews, and new technologies like trimulFRAC, operators have managed to reverse some recent worrisome cost and performance signals. In fact, several leading tight oil players improved their spending efficiency by an average of 25% from 2022 to 2023.

Going forward, development costs could keep falling. Updated spacing and sequencing could boost performance post-M&A, and recent buyers haven’t been shy about their plans for massive operational improvements.

{kind=link}

{kind=link}

3. Latin America: Guyana momentum with FPSO 6 but gas challenges

While a sixth floating production, storage and offloading (FPSO) vessel was long expected in Guyana, reaching a final investment decision at Stabroek represents another significant milestone for the development. The three onstream FPSOs have shown great operational performance, and three additional FPSOs are expected to come onstream in 2025, 2026 and 2027 – with total production forecast to reach 1.3 million b/d of oil.

Guyana has established itself as a key producer in Latin America – and will soon be second only to Brazil. It should be said, though, that Guyana is a rarity among South American countries, most of which have traditionally struggled to attract investment in their oil and gas discoveries.

Guyana’s biggest challenge will be in monetising its gas. Although oil discoveries have been developed, large gas and condensate discoveries are being left untapped. There are many possible development directions for gas, including the production of methanol, fertiliser and LNG. Even with the right infrastructure and partners, gas monetisation routes all require significant costs.

Gas resources have increased by an average of 2.5 tcf per year since 2015. While the estimated gas-to-oil ratio (GOR) has remained between 1,000 and 2,000 scf per barrel, some recent discoveries have shown ratios of 6,000 or higher.

A gas-to-power project (receiving about 50 mmcfd) is tabled to start in 2025, and the government has asked Stabroek Block operator ExxonMobil to assess an LNG development. It has also released a Request for Proposals (RFP) for an offshore gas gathering system.

But while the right noises are being made, the truth is that an ultra-deepwater LNG project will require outstanding productivity to be successful, alongside a highly effective commercial structure, the right financing and perfect timing. Energy transition headwinds will fire up competition in the long term, too.

For more information, analysis and charts on the global upstream picture, and our latest predictions for the coming year, fill in the form at the top of the page to receive an extract of the report.