The biggest topics in global upstream

Some upstream oil and gas sectors gave us supply surprises in 2023, with some regions producing above expectations, others disappointing. What didn’t disappoint was the level of excitement around M&A, which features throughout the regions in our latest global upstream update.

4 minute read

Fraser McKay

Head of Upstream Analysis

Fraser McKay

Head of Upstream Analysis

As head of upstream research, Fraser maximises the quality and impact of our analysis of key global upstream themes.

Latest articles by Fraser

-

Featured

Upstream oil and gas 2026 outlook: half-time report

-

Opinion

Global upstream update: handpicked for small and mid-sized E&Ps

-

The Edge

How quickly can Gulf oil exports recover?

-

The Edge

Ceasefire in the Middle East

-

Opinion

The biggest topics in global upstream

-

Opinion

Middle East conflict set to drive oil and LNG prices significantly higher

The Global Upstream Update is a regular insight produced for global subscribers to our Upstream Service. In this edition, we share some of the most impactful events in 2023, reflect on how they have evolved, and consider what could happen next.

Fill in the form for an extract or read on for a quick introduction to four key themes we will be tracking closely over the course of this year.

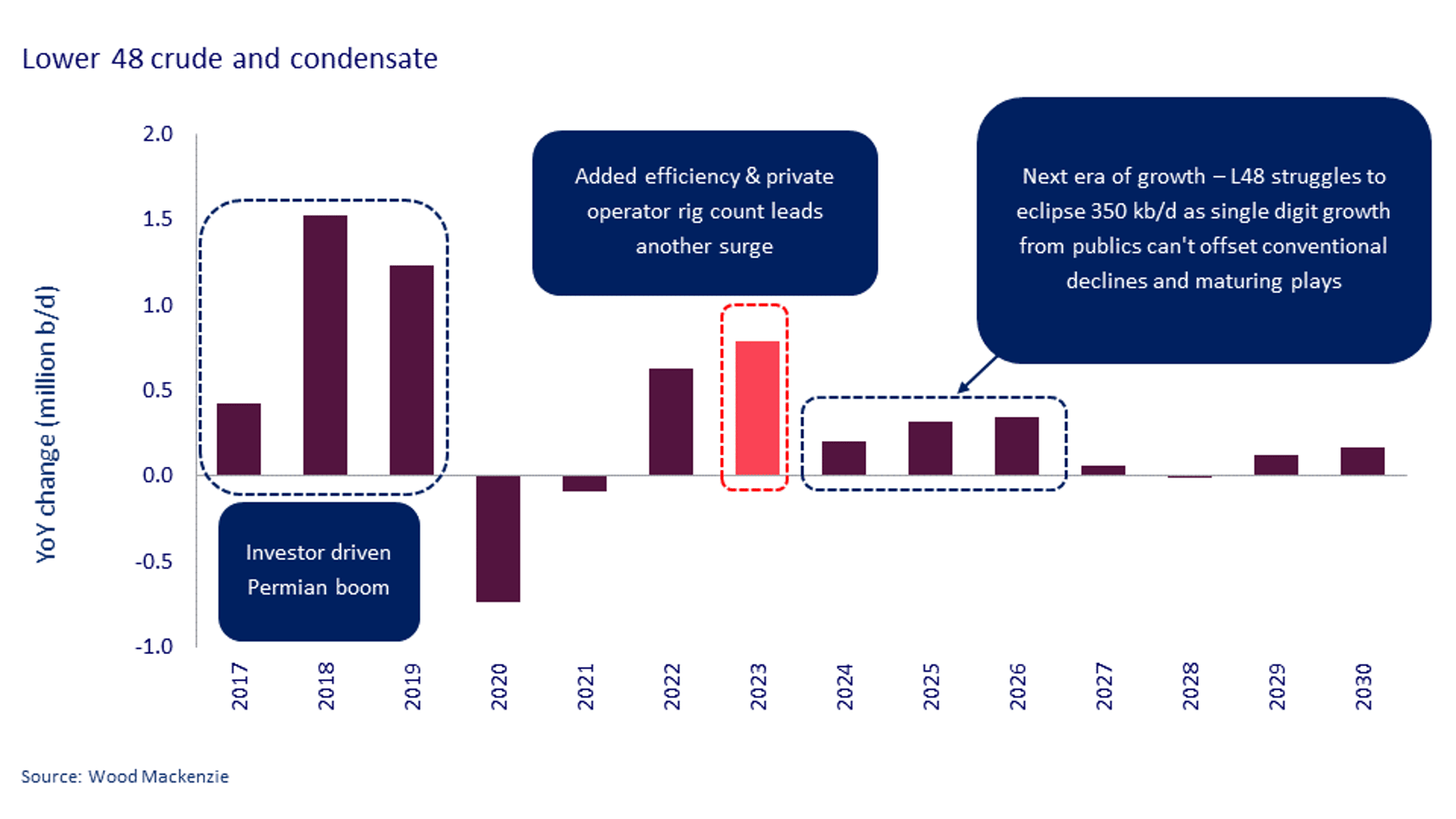

1. Liquids supply: US surprises to the upside while Nigeria continues to struggle

When it comes to supply, the regional outlooks are mixed. In the US Lower 48, liquid supply has been stronger than we predicted, as efficiency gains surprised to the upside.

Faster completion times enabled E&Ps to bring wells online much earlier in the year, without raising capex. Private E&Ps did slowdown in H2 – but only after a stellar H1. Our 2023 growth estimate is therefore up by 150,000 b/d on our previous prediction, and now stands at 860,000 b/d. But going forward, we anticipate a new phase of more measured growth.

By contrast, Nigeria has struggled with maturing assets, falling investment and multiple other above-ground issues for years resulting declining liquids production. Big changes will be needed to bring material growth to Nigeria, with regulatory hold-ups adding to the delays. There are motivated new players waiting in the wings, however, ready to develop onshore and shallow water assets.

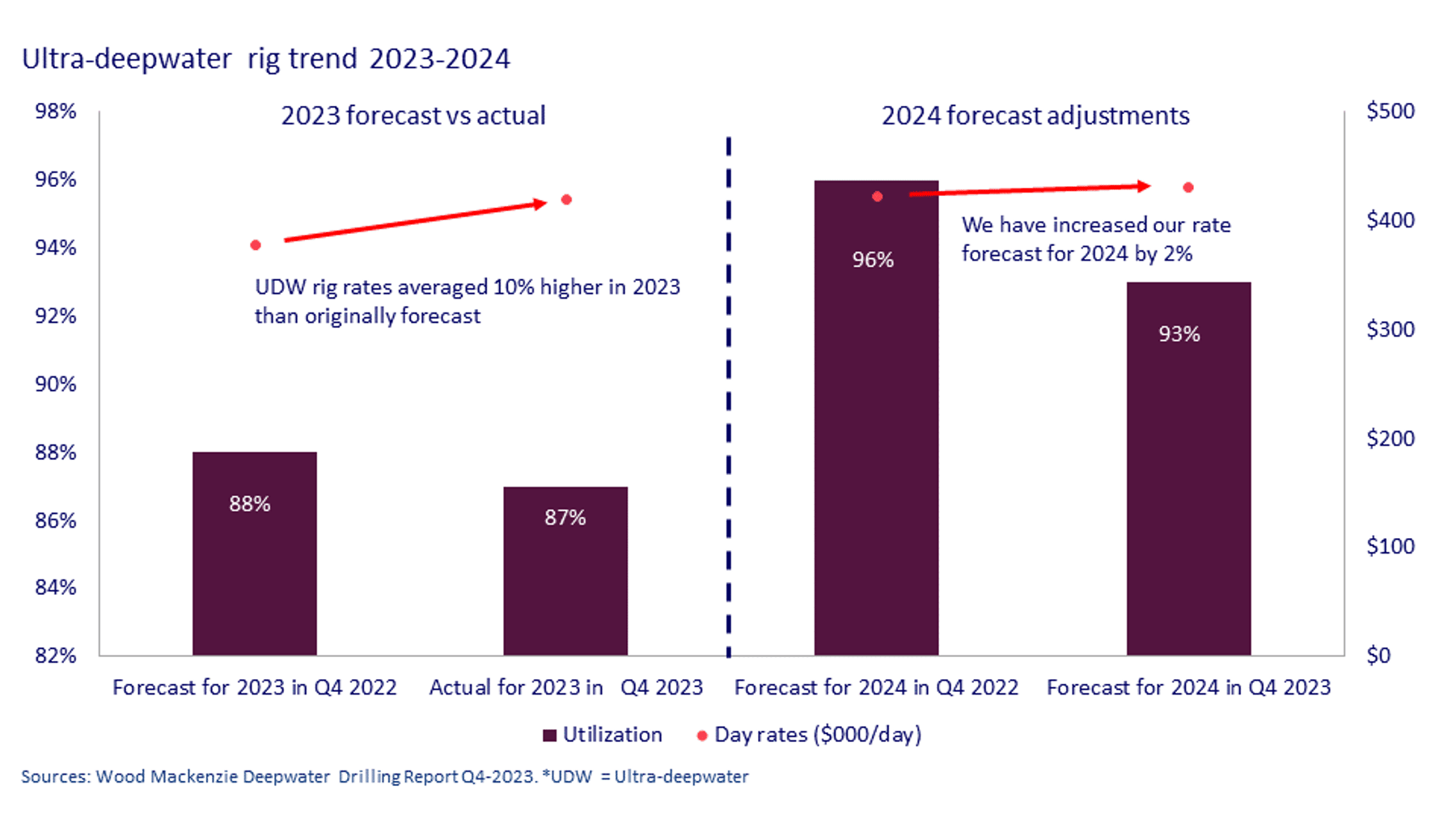

2. Investment: ultra-deepwater rigs are in short supply

The impacts of a stretched supply chain are being felt; the ultra-deepwater rig supply is extremely tight, with rates for the highest spec rigs in the hottest sectors reaching nearly US$500k/day. We forecasted these rigs to be utilised globally at a rate of 88% in 2023 and 96% in 2024, with rates climbing to US$419k/day this year.

While our 2023 forecast has been accurate, rate hikes accelerated, and resultant rates have exceeded our forecast by 10%. Our 2024 utilisation estimate has fallen slightly, but average global rates will still nudge up 2% to US$430k/day.

We expect the UDW rig market to remain very tight. Rig owners aren’t interested in adding capacity. It’s all hands-on deck to free up supply; look out for some idle rigs returning this year, more operators locking in rigs for longer via multi-year contracts, and longer lead times on new contracts as near-term availability is lacking.

{kind=link}

{kind=link}

3. Mergers & Acquisitions: a turbulent year for Australia

It looked like it was going to be a huge year for asset deals in Australia, with Japan LNG, bp, INPEX and Saudi Aramco snapping up high quality gas and LNG projects. The biggest attempted deal, however, didn’t make it over the line. Origin Energy’s acquisition by Brookfield Asset Management and MidOcean Energy was set to go ahead in March for US$13 billion but fell through. Even this would have been trumped by the rumoured merger of Woodside and Santos, which fell apart before it really got going.

At the time, we felt the moves from Aramco and Japan were symptomatic of Australia’s valuable long-term assets, and that short-term regulatory uncertainty and government intervention in the gas market could be overcome. After the collapse of the Origin deal, we felt a possible merger with Woodside and Santos didn’t sufficiently address lingering investor concerns, and sure enough, talks were abandoned.

Santos remains under pressure from shareholders and remains under pressure to unlock value for shareholders. We think its LNG assets in PNG and Australia could appeal to a range of parties, so a future deal could still shake out. We also expect a busy year ahead for SE Asia too.

4 Decarbonisation: balancing extra volumes with emissions targets

Mega-mergers have helped advance the biggest global IOCs’ decarbonisation plans. They are expected to keep outperforming the sector, but there’s still some way to go. With production on the rise, 2024 will certainly bring higher total sector emissions.

Of last year’s megamergers, ExxonMobil’s emissions outlook in particular will be greatly impacted, with low intensity barrels added. However, the extra volumes will increase absolute emissions.

Going forward, the largest companies will continue to hone their portfolios, focusing on the most advantaged barrels in an effort to balance reduce portfolio emissions.

Geothermal technologies present huge potential, with the possibility of a technological breakthrough that could transform a tiny market into a global industry. Success here could result in geothermal heat and power growth from around 50 GW in 2023 to over 250 GW by 2050, with over US$1 trillion of investment. This growth would be equivalent to over 3 million barrels of oil per day, or the UK’s offshore oil industry at its peak.

For more information, analysis and charts on the global upstream picture, and our latest predictions for the coming year, fill in the form at the top of the page to receive an extract of the report.