How Asia’s NOCs can learn to stop worrying and love the energy transition

Time for a gear-change in how Asia’s national oil companies respond to climate change and emissions

1 minute read

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

Latest articles by Gavin

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

Opinion

Why US Henry Hub natural gas prices are set to rise | Webinar replay

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

All oil and gas companies are in a state of flux. Driven by the energy transition, upstream supply must now be low cost, low risk and, increasingly, lower carbon. Lenders and shareholders seek clear strategies on emissions reduction, while still expecting the returns that attracted them to oil and gas companies in the first place.

Corporate strategies are now fluid as companies increase their focus on long-life gas projects or even begin their transformation into broad-based energy providers.

The European majors may have been the quickest out the blocks in their response to the energy transition, but even they have been outpaced by Repsol’s December 2019 commitment to net-zero carbon from Scope 1, 2 and 3 emissions by 2050. This announcement did not go unnoticed in the boardrooms of Asia’s national oil companies (NOCs).

This is because Asian NOCs do not live in a bubble. From Tokyo to Jakarta, the energy transition is the hot topic, with management fully aware that they must respond to what is now the single most important challenge facing their companies. By and large, the Asian NOCs understand that doing nothing is no longer an option.

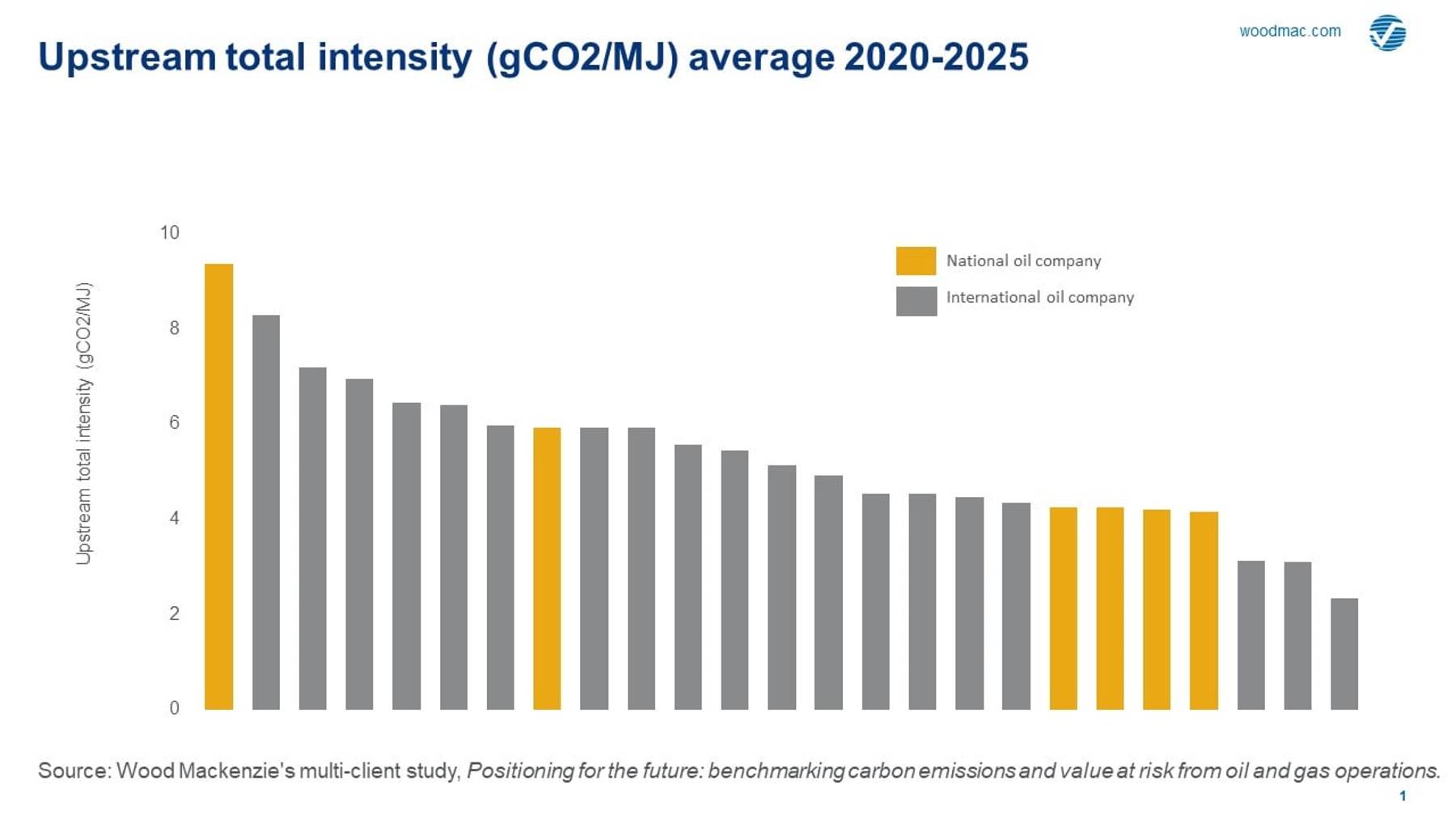

But with very few exceptions, most are struggling with their response. Yes, we have seen some organisational changes to incorporate new energies businesses and modest investment in renewables is underway. But many have yet to formulate a coherent strategy towards climate change risk, let alone communicate it well. This is a pity, as some Asian NOCs are actually well positioned in terms of carbon intensity within their portfolios, while others have laid foundations for change.

A pathway to action

Let me be clear, I am not suggesting that the remit of Asia’s NOCs will radically shift away from the development of national oil and gas resources (I heard this message loud and clear on recent visits to India and China. And shouting at developing economies to stop producing/consuming oil and gas is frankly ludicrous).

But this does mean that companies must now work to emulate industry best-practice; reducing carbon intensity, investing in cleaner energy and increasing transparency and disclosure.

Government policy will be the key driver for change in Asia. As recent action on winter air quality in North Eastern Asia has highlighted, governments can move fast in this part of the world. Some NOCs (notably PTTEP and PETRONAS) have already pegged some of their emissions reduction targets to national goals.

European oil and gas companies may have largely been spurred into action by investors, but in Asia it is unlikely equity markets, for example, will play an equal role in strategic change. Public listings are relatively small, and some NOCs are not listed at all. But as companies look to refinance debt or seek project financing over the next few years, lenders will increasingly scrutinise their ‘green’ credentials.

{kind=link}

What can Asia’s NOCs really do? Quite a lot. Here I bring in my colleague Max Petrov from our Corporate team, who covers the Asian NOCs. In his recent insight, Max burnishes his credentials as a realist. He knows that oil and gas production will remain critical to the Asian NOCs but argues that they must also act on the following key areas:

- Transparency and disclosure: Asian NOC disclosure on environmental performance is mixed. PTTEP leads the pack. Much more is required.

- Optimising the existing portfolio: a sustainable future means building structural resilience into the business, positioning lower down the cost curve and managing key risks. Sinopec Group and CNPC could certainly take a bolder approach to international upstream rationalisation.

- Decarbonisation: NOC carbon emissions vary widely, but we do see scope for big improvements that could help NOCs' industry competitiveness. PTTEP and CNPC have both made carbon reduction commitments, but others are yet to follow.

- Diversification into new energies: PETRONAS’s purchase of AMPLUS SOLAR in April 2019 led the way, while CNOOC Ltd is growing its presence in offshore wind. But how far Asia’s NOCs will diversify their portfolios is debatable.

Change is hard, but the alternative is worse

No single solution will fit all Asian NOCs. Each will have to change according to its capabilities, portfolio and the needs of its own domestic energy market. It’s all well and good for Asia’s NOCs to attempt to emulate the majors in their response to the energy transition, but none has their operating capabilities. To build resilience into their portfolios, companies must now begin to provide clarity on strategy, continue to manage costs and get moving on reducing emissions. This will be the key to long-term NOC sustainability.

APAC Energy Buzz is a blog by Asia Pacific Vice Chair, Gavin Thompson. In his blog, Gavin shares the sights and sounds of what’s trending in the region and what’s weighing on business leaders’ minds.