Sign up today to get the best of our expert insight in your inbox.

Will falling populations reshape energy demand?

Declining birth rates could change future energy growth projections

1 minute read

Simon Flowers

Chairman, Chief Analyst

Simon Flowers

Chairman, Chief Analyst

Simon is our Chief Analyst; he provides thought leadership on the trends and innovations shaping the energy industry.

Latest articles by Simon

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

Latest articles by Gavin

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

Opinion

Why US Henry Hub natural gas prices are set to rise | Webinar replay

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

Prakash Sharma

Vice President, Head of Scenarios and Technologies

Prakash Sharma

Vice President, Head of Scenarios and Technologies

Prakash leads a team of analysts designing research for the energy transition.

Latest articles by Prakash

-

The Edge

Will falling populations reshape energy demand?

-

Opinion

How is energy transition investment evolving in 2026?

-

The Edge

How the Iran war could change energy markets

-

Opinion

Energy transition outlook: Asia Pacific

-

Opinion

Energy transition outlook: Africa

-

Opinion

Energy transition outlook: Middle East

Peter Martin

Vice President, Head of Economics

Peter Martin

Vice President, Head of Economics

Peter is responsible for our global economic outlook to 2060.

Latest articles by Peter

-

The Edge

Will falling populations reshape energy demand?

-

Opinion

Horizons Live: Strait talking | Webinar replay

-

Opinion

Investing for the long term: quantifying the economic costs of an accelerated energy transition

-

Opinion

European gas: 6 Q&As on prices, supply, and regulatory impact

-

Featured

Metals & mining 2026 outlook

-

Opinion

Tariffs, trade and technology: the macro forces shaping metals markets

The impact of the war in Iran on energy markets isn’t the only new risk factor strategic planners will consider as they refresh their outlooks in the coming months. No less important is how the intensifying downward trend in fertility rates might affect global populations and energy demand in the longer term. Peter Martin, Head of Economics, and Prakash Sharma, Head of Energy Transition, shared their initial thoughts with me.

Declining birth rates, declining population

Economists say that demographics dictate destiny. In that context, the rapid decline of birth rates and fertility rates are eyebrow-raising at the very least. If these trends continue, the global population will severely undershoot current projections, threatening economic growth expectations and reshaping energy and commodity demand.

Population growth is a cornerstone of the anticipated rise in global demand for energy in the coming decades. Current projections by the United Nations (UN) indicate the global population will increase from 8.2 billion in 2025 to 10.0 billion in 2060. Plummeting global fertility rates suggest that number might be far too high.

The decline in fertility rates will simultaneously drive down overall birth rates and accelerate population ageing. The global fertility rate fell from 2.6 births per woman in 2007 to 2.2 in 2025, perilously close to the 2.1 replacement ratio needed to keep the population stable.

Complex socio-economic factors underpin the decline – rising educational attainment, female participation in the workforce, the high cost of housing and even the proliferation of smartphones are cited. Whatever the drivers, women in many countries are having fewer children than previous generations or are opting out of parenthood altogether.

China’s birth rate, for example, fell to 5.6 births per 1,000 people in 2025, the lowest ever recorded, landing between the UN’s expected 6.2 and its low-case scenario of 4.7. China’s population contracted by 3.4 million people last year and now stands at 1.40 billion – 9.6 million below the UN projection from 2024.

Observed reductions in fertility rates suggest that the UN may soon substantially reduce its global population projections. Under the UN’s current low birth rate scenario, the global population could decline even within our forecast horizon to 2060, peaking at 8.9 billion in 2053. By the end of the century, the global population could fall to 7.0 billion, back to 2011 levels.

A new UN World Population Prospects is expected to be released in July 2026. We don’t anticipate a downgrade as extreme as its low birth rate scenario, but any dampened demographic outlook will have economic consequences. Any escalation of global ageing trends and shrinking working-age populations will exert downward pressure on global GDP forecasts.

We currently forecast global primary energy consumption increases by 8% from current levels, reaching a peak of 717 exajoules (EJ)* in 2035, before gradually declining to 672 EJ by 2060. Electricity consumption continues to grow though the period, doubling to 71 petawatt-hours.

What declining fertility rates mean for energy

First, most of the drivers of energy demand appear to be robust through our forecast horizon to 2060, regardless of any demographic downgrade. The global population is still expanding and even a pessimistic scenario would see an increase of around 700 million people by 2060 from current levels.

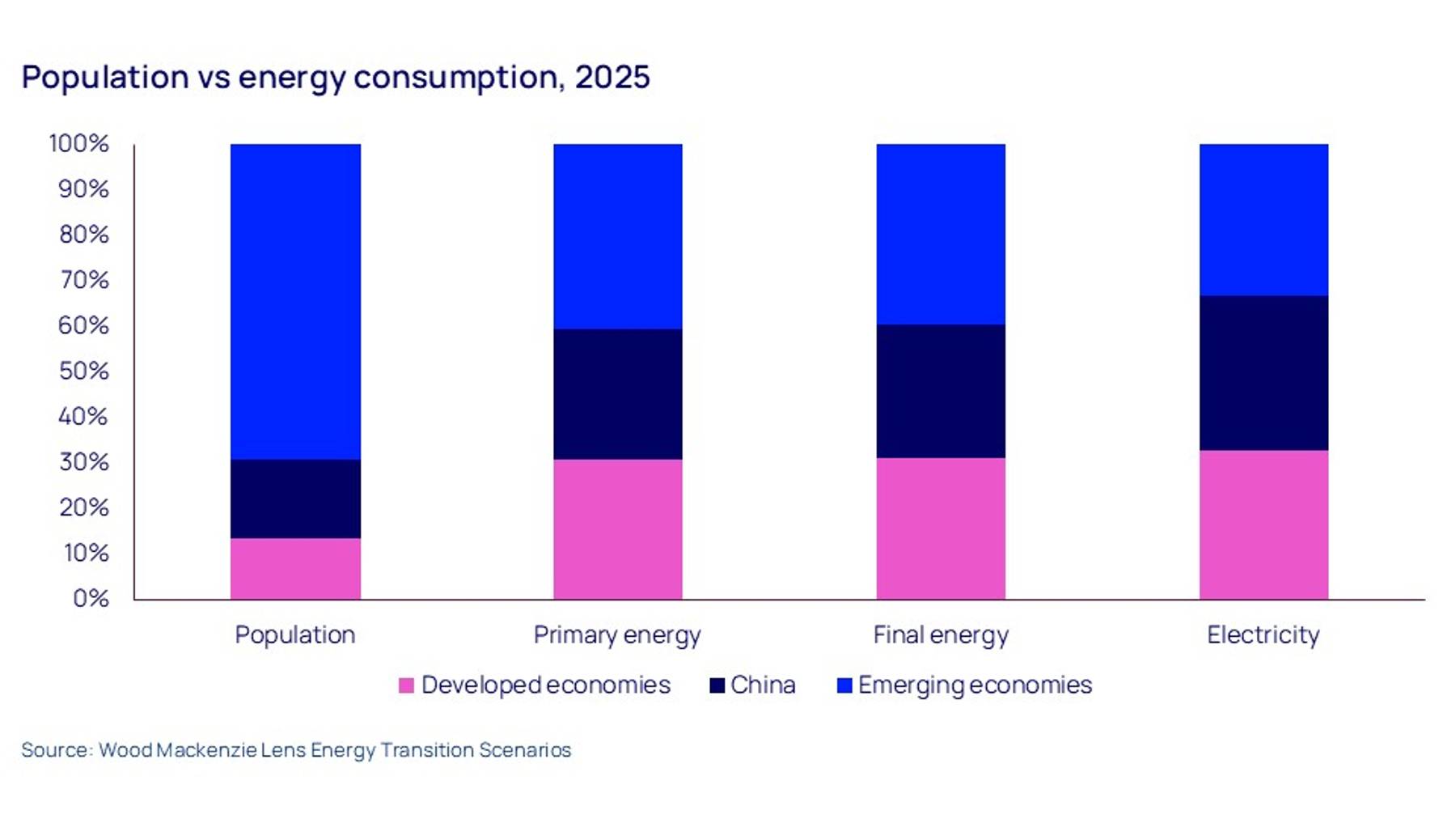

There are also still vast unmet energy needs across the emerging markets of Asia and Africa – we expect convergence towards developed economy usage (see chart). Rising incomes and wealth will drive greater consumption of material goods. The rapid scale-up of electrification, renewables and AI adoption will create an unprecedented draw on critical minerals while reinforcing the decoupling of economic growth and hydrocarbons.

Second, the impact of lower population would exacerbate existing trends and challenges for energy markets. Shrinking workforces will increase the incentive to invest heavily in AI-driven automation across all sectors, embedding the upside for electrons and related critical minerals – and a downside for molecules. An unintended consequence, however, is that automation could lead to social inequality – wealth concentrated among capital owners at the expense of labour. Fewer workers and reduced purchasing power will eventually limit the upside in consumer demand.

Third, pressures on public finances and the cost of living are likely to progressively intensify. Governments, therefore, need to act decisively to secure private and public capital to ensure the energy system adapts and evolves before the demographic profile changes dramatically after 2060. That includes incentivising a sustainable energy system – smart, clean grids – while finance is available. If done effectively, the upside is that AI-driven productivity gains could boost economic growth by offsetting the demographic drags, and public finances could be more resilient post-2060.

Finally, an earlier and lower global population peak is now viable and capable of making or breaking the next commodity super-cycle. Whether it manifests as a headwind or a catalyst for energy demand depends on how the world manages the intricacies of demographics, economic growth and technology. Amid this friction, the role of governments to maintain stability becomes ever more critical.

{kind=link}

*1 exajoule – 0.5 million b/d of oil approximately

Make sure you get The Edge

Every week in The Edge, Simon Flowers curates unique insight into the hottest topics in the energy and natural resources world.