Lower 48 midstream not immune to oil price volatility

Very little new drilling makes sense at US$35/bbl (WTI). What does it mean for midstream players when E&Ps decelerate production to survive the downturn?

1 minute read

Alex Beeker

Director, Corporate Research

Alex Beeker

Director, Corporate Research

Alex is a research director on our Corporate Research team, focused on the Majors and US Independents.

Latest articles by Alex

-

Opinion

Low hedge strike prices limit upside for oil producers

-

Opinion

Video | Venezuela in global portfolios: risk, restraint, and strategic optionality

-

The Edge

US upstream gas sector poised to gain from higher Henry Hub prices

-

The Edge

The complexity of capital allocation for oil and gas companies

-

Opinion

Ten key considerations for oil & gas 2025 planning

-

Opinion

Chesapeake-Southwestern Energy deal: ten key takeaways

The oil and gas industry is so intertwined that the relative success, failure or financial health of one element has an impact on every other. Midstream is not immune, even where contracts for minimum volumes or acreage exist. Read on to learn more about the impact of the oil market crisis on midstream players, or download the slide pack to find out which companies have been affected and to what extent.

Upstream players in survival mode would rather violate midstream contracts than drill at US$35/bbl

E&Ps in the Lower 48 have rapidly responded to the downturn by cutting capex by 40-50% and cutting the rig count in half since March this year. They are doing whatever it takes to survive. Many are electing to defer drilling and completion activity, in violation of their minimum volume commitment contracts with midstream companies. At low prices, it can be more economic to break midstream agreements than to drill uneconomic wells.

As a result of the Lower 48’s rapid response to the macro environment, oil production is expected to decline by 1.4 million b/d from March to June 2020. Around 1.0 million b/d of this comes from shut-in or curtailed production.

We assume that some shut-in production comes back online in July, with a return to normal levels by August. June is expected to be the low point for production, but it is highly dependent on oil price. Oil demand should recover in the coming months as lockdowns ease, and we expect Brent to reach US$40/bbl by year-end 2020. All flowing production is economic at that price. Re-opening wells could push US Lower 48 production back up to 9.3 million b/d during Q3. Ultimately, higher prices are needed to get oil rigs working again.

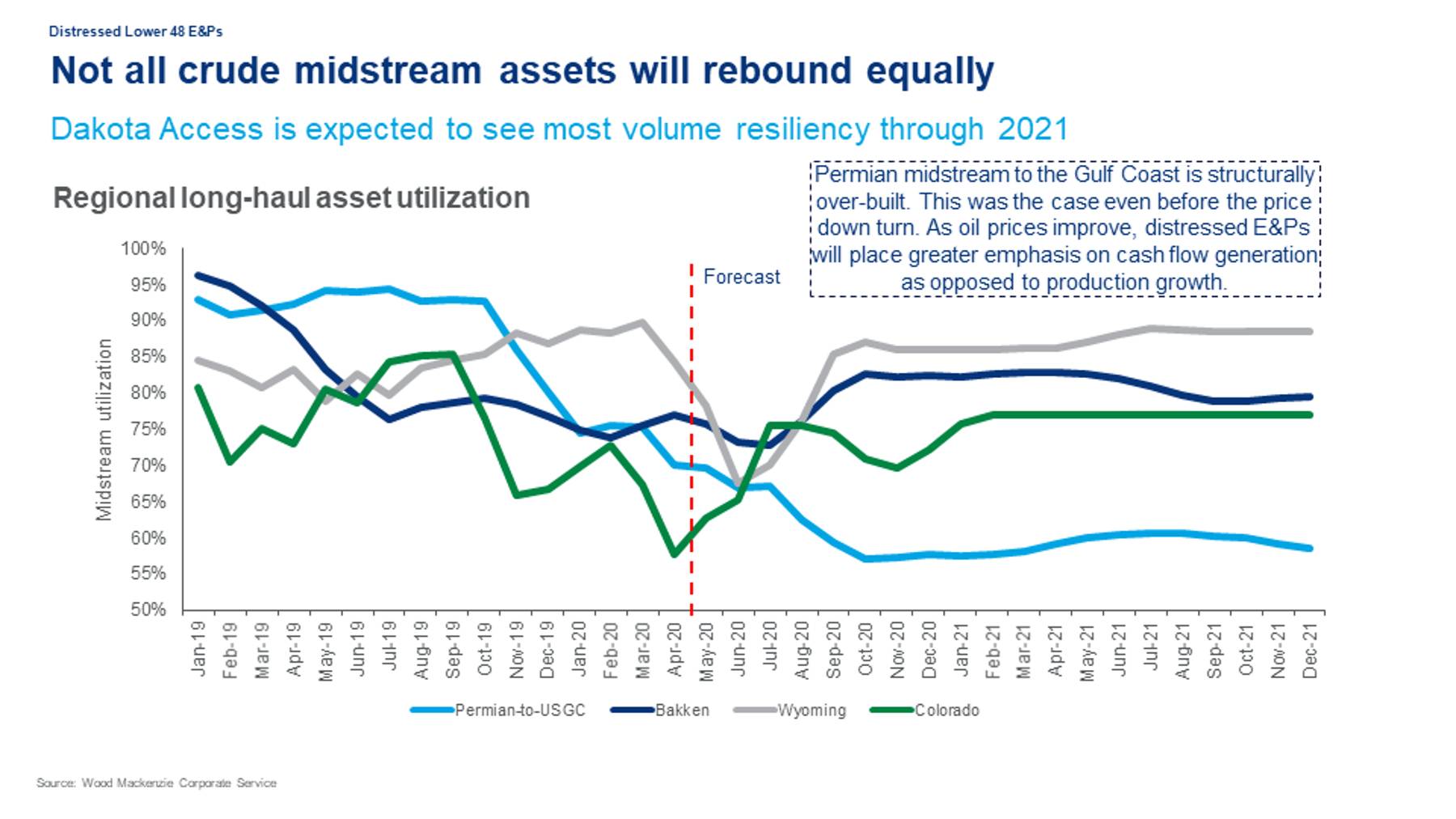

Distress in the upstream sector is spreading to the midstream, but not all companies are affected to the same degree

Several years of significant production growth in the Lower 48 saw an accompanying growth of midstream infrastructure, including gathering and processing lines, as well as long-haul pipelines to get the oil to market. For midstream companies that made huge investments based on pre-Covid-19 production forecasts, low utilisation now presents a challenge. Midstream infrastructure projects, many of which were financed with high levels of debt, will struggle to deliver projected returns. And cash flow is falling in tandem with utilisation, limiting the ability of the midstream to increase distribution.

Structural overbuild in Permian basin will hamper midstream recovery

The Permian basin was branded as the growth engine of the US, which drove investments in infrastructure. As a result, long-haul pipelines between the Permian and the US Gulf Coast were overbuilt even before the price downturn. We forecast Permian utilisation will fall further and faster than the Bakken, Wyoming and Colorado to 60% by October this year, and stay at around that level until at least December 2021. By contrast, Colorado and Wyoming midstream infrastructure utilisation rates show a v-shaped recovery, returning to normal levels by early 2021: Bakken stabilises at about 80% utilisation by October 2020.

{kind=link}

{kind=link}

As oil prices improve, distressed E&Ps in the Permian will place greater emphasis on cash flow generation as opposed to production growth. Long-haul capacity is expected to exceed supply by July 2020, reaching an excess of 2 million b/d by July 2025.

To find out how the downturn is affecting the financial health of midstream players in the Lower 48, fill in the form on this page; we'll send you the slide pack from our recent webinar.

How we assess the financial health of players in the Lower 48

We use the Wood Mackenzie Financial Health Index to assess which operators are best-positioned to survive the downturn. Our Wood Mackenzie Financial Health Index ranks companies on a scale from 1 to 10 – with 10 being the strongest – based on six financial indicators. A FHI score below 4 is a strong indicator of financial distress. We've applied that methodology to a number of the midstream companies in the Lower 48. Fill in the form on this page to discover which companies are most severely affected by the downturn and why.