The Norwegian emissions dilemma

What is the real impact of curtailing production from Norway on the broader European energy landscape?

3 minute read

Lisa Gillespie

Director, Energy Consulting

Lisa Gillespie

Director, Energy Consulting

Lisa is an experienced project manager working across upstream and the energy transition.

Latest articles by Lisa

-

Opinion

NZIA feasibility report: Is the NZIA achievable from a full value-chain perspective?

-

Opinion

Policy vs. Practicality: assessing the feasibility of meeting NZIA Article 23

-

Opinion

The Norwegian emissions dilemma

-

Opinion

Can carbon offset crude move from idea to reality?

Malcolm Forbes-Cable

Vice President, Upstream and Carbon Management Consulting

Malcolm Forbes-Cable

Vice President, Upstream and Carbon Management Consulting

Malcolm is an expert in strategy development, transaction support and the energy transition.

Latest articles by Malcolm

-

Opinion

Five key takeaways from our Gastech 2025 Leadership Roundtables

-

Opinion

The UK's critical role in Europe's integrated oil system

-

The Edge

No country for oil men (and women)

-

Opinion

The Norwegian emissions dilemma

-

Opinion

The case for developing UK's oil and gas resources: Rosebank and Cambo fields

-

Opinion

Scotland the brave: a Firth of Forth net zero hub for COP26?

The challenges of climate change and the role oil & gas production and consumption play in this are well documented. Over recent years we have seen governments pledge ambitious emissions reduction targets which will require a significant shift in the overall energy ecosystem. This move away from a reliance on fossil fuels to a more diverse energy mix underpinned by renewable energy sources is underway but like any large-scale change, it will take time.

The scale of progress has slowed in recent years, impacted by several factors including macro events, supply chain issues and cost pressures. As the old saying goes, Rome was not built in a day, and whilst we wait for this new energy market to develop, demand for oil & gas remains. The challenge moves to focusing on developing those oil & gas reserves with the lowest possible emissions footprint.

Wood Mackenzie was engaged by Aker BP to conduct a study looking at the future emissions from developments in Norway, and what would be the overall emissions impact of substituting Norwegian supply with that from other countries. The study leveraged our Emissions Benchmarking Tool, LNG Emissions Tool and Crude Cargoes Emissions Tool to provide a country-level assessment of future emissions. Here are the key findings.

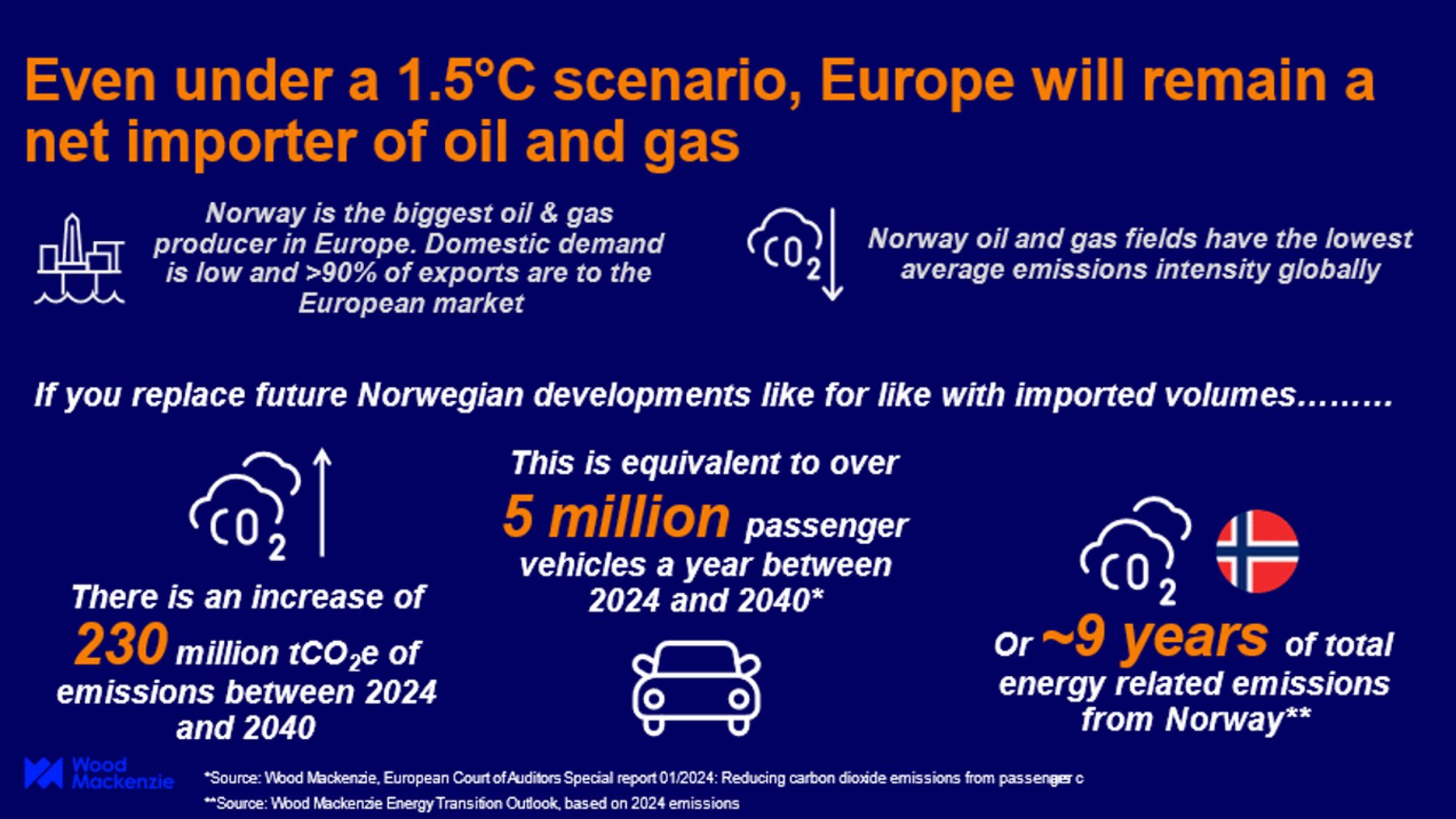

1. Norway is the largest and lowest emissions supplier of oil and gas in Europe.

Norway is the largest producer of oil and gas in Europe and with low domestic demand, it is a net exporter with Europe the primary market. It is Europe’s largest primary source of oil and gas but does not fulfil all demand hence Europe also relies on imports of oil and gas from North America, the Middle East and West Africa. Of all the main European supply sources, Norway has the lowest average upstream emissions intensity which means there are fewer emissions per barrel of oil and gas produced compared to competing supply sources.

2. Even under our most ambitious climate change scenario, Europe will remain a net importer of oil and gas.

Wood Mackenzie models a Net Zero 2050 scenario which is consistent with 1.5˚C warming and assumes a more aggressive adoption of low-carbon and renewable technologies. Under this scenario, our forecast for European oil and gas demand out to 2040 never exceeds supply meaning that Europe will need to import oil and gas even in our most ambitious scenario.

3. Alternative sources of supply into Europe have a higher upstream, transport and midstream emissions intensity than Norway.

Using Wood Mackenzie’s oil & gas market databases and analysis we established the main supply sources of oil and gas in Europe to understand the relative positioning of Norway in terms of emissions intensity. As previously highlighted, Norway has the lowest average upstream emissions intensity and due to its proximity to the European market relatively low transport emissions. One of the key drivers of low emissions intensity in Norway is the electrification of upstream developments, which is particularly impactful as Norway’s grid is almost exclusively powered by hydro. By 2026 Wood Mackenzie forecasts that over 60% of Norwegian production will be electrified.

{kind=link}

4. The net impact of no future developments being sanctioned in Norway is an increase of 230 million tonnes of CO2e emissions between 2024 and 2040.

Wood Mackenzie modelled two future scenarios to quantify the impact of no future developments in Norway. The first scenario modelled emissions assuming Norway continues to develop the discovered resources considered commercial and the second scenario assumes no future developments are sanctioned and Europe substitutes oil & gas supply from Norway with supply from other countries. The impact of no future developments in Norway is an increase of 230 million tonnes of CO2e from upstream, transport and midstream emissions from 2024-2040, equivalent to approximately 9 years of energy-related emissions from Norway.

The study highlights the challenges faced in managing the complexities and long-term undertaking of the Energy Transition, and the need to focus on meeting the continued demand for fossil fuels whilst mitigating emissions during their production, transportation and consumption. Norwegian oil and gas, through electrification of its developments powered by renewable energy and strict methane management, coupled with proximity to the market results in oil and gas that is supplied to the market with a lower emissions intensity than alternative sources. The overall impact of curtailing production from the Norwegian Continental Shelf results in higher absolute emissions.

Don’t forget to fill out the form at the top of the page to access your complimentary copy of this report.