Third wave US LNG: a $100 billion opportunity (part 2)

How can developers of new US LNG capacity generate double digit returns and reach FID?

3 minute read

Sean Harrison

Senior Research Analyst, Gas & LNG

Sean Harrison

Senior Research Analyst, Gas & LNG

Sean specialises in North America LNG research, focusing on assets analysis, project economics and LNG contracting.

Latest articles by Sean

-

Opinion

Video | Lens Gas & LNG: Valuing Petronas’ LNG assets

-

Opinion

Video | Lens gas & LNG: Three key LNG M&A opportunities

-

Opinion

Video | Lens Gas & LNG: Golar and partners' FID set to revive Argentina's LNG export ambitions

-

Opinion

Shining a light on the “coal versus LNG emissions” debate

-

Opinion

Video | Lens Gas & LNG: What is Venture Global's LNG strategy?

-

Opinion

Woodside acquires Tellurian and the Driftwood LNG project

So far, three US LNG projects have attracted debt and equity financing totaling over US$40 billion this year, allowing them to take a final investment decision (FID). Despite rising capital costs and interest rates, further US LNG projects are likely to raise finance in 2024.

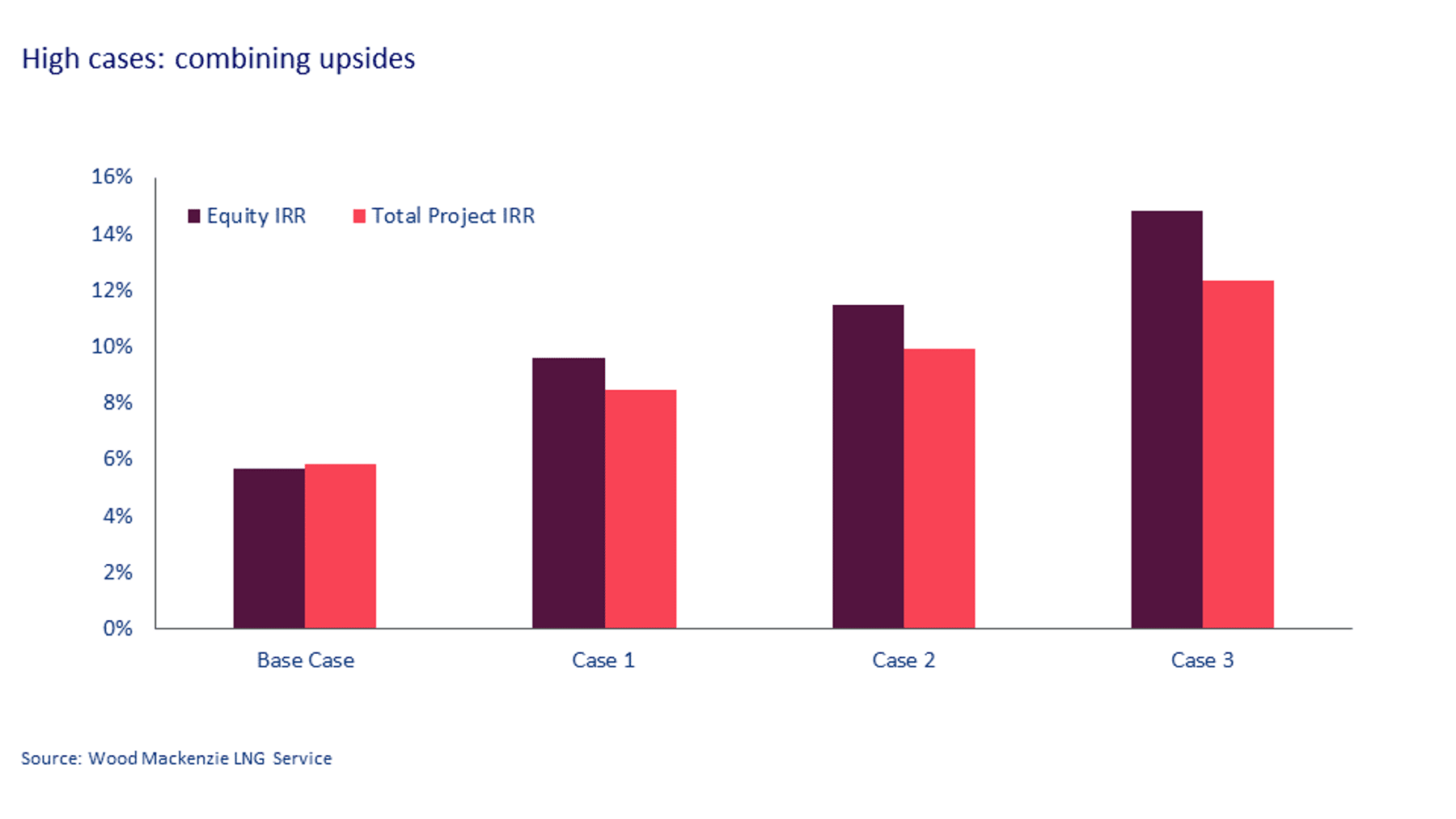

Our base case economic analysis, presented in part one was published back in February showed margins are tight - unlevered internal rates of return (IRRs) are around 5-6% for many greenfield projects.

Using analysis from a new report, the reasons why, despite these rising capital and interest rates, projects are still raising finance are investigated. Read on for an introduction to some of the questions explored in the full report.

1 includes financing costs. US$10 billion has been raised by equity partners (US$7 billion by financial investors including KKR, GIP, GIC and Mubadala Investment, and US$3 billion by strategic investors including ConocoPhillips and TotalEnergies), with the remaining funds raised via debt markets and developer equity.

What upside opportunities are helping projects attract equity investment?

Amidst the financial landscape of 2023, the Plaquemines LNG Phase 2, Port Arthur LNG Phase 1, and Rio Grande LNG Phase 1 projects secured significant financing, marking a pivotal moment in LNG development. The sanctioning of both Port Arthur LNG Phase 1 and Rio Grande LNG Phase 1 was heavily supported by investment from infrastructure investors and major LNG developers. With momentum already behind the projects (both were fully permitted with signed EPC contracts), the capital provided by the equity investors proved the key to securing the funds required to reach FID.

The substantial $40 billion influx of financing underscores the confidence developers and financiers hold in these ventures, indicating promising prospects for returns on investment. In response, we've constructed scenario cases, delving into potential upsides and their capacity to enhance project economics.

We have demonstrated that upsides – increasing LNG output, extending plant lifetime, higher liquefaction fees, and selling uncontracted volumes at a higher differential between global spot prices and Henry Hub – could increase returns for equity investors to above 10%. This is shown in the chart below.

{kind=link}

These returns build a stronger case for equity investment, both from financial investors looking for best in class investments, and strategic investors searching for high returns and low-cost supply to add to their portfolio.

Other upsides exist including achieving a margin on feed gas procurement, selling pre-commercial volumes; marketing uncontracted volumes on higher prices through short-term deals; charging fees for services, such as low carbon-intensive LNG and developing additional trains. These could further bolster returns.

However not all projects will still have access to all upside opportunities, and how upsides affect each project will vary depending on debt-to-equity financing splits, uncontracted volumes, and commercial structure.

What are the risks?

Although there is a case for equity investment, the situation is not without risks. Risks of lower returns will still pose concern for investors, while debt financiers typically invest based on guaranteed returns and so will want projects to ensure a minimum level of return without relying on uncertain upside.

Investors will likely be concerned about regulatory uncertainties and wary of backing projects with un-credit-worthy sponsors. Additional FIDs may also lead to labour shortages and construction risks.

What is the 2024 outlook for US LNG?

While risks do remain, equity infrastructure investors and major LNG players are showing a continued interest in US LNG. Therefore, developers who can mitigate costs, secure credit worthy off-takers and partners, overcome regulatory hurdles, and showcase the ability to access upsides will be well-placed to attract further investment as they seek to sanction projects. Will we see a wave of new FIDs soon to increase capacity even further?

Full the analysis presented in this report as well as insight into our scenario analysis is featured in our LNG Service.