Top 10 solar PV inverter vendors cornered 86% of the market in 2022

Our latest Global Solar PV Inverter and Module-Level Power Electronics Market Share 2023 report analyses the top-ranking vendors by quantity of shipments in 2022

3 minute read

Sagar Chopra

Senior Research Analyst, Solar

Sagar Chopra

Senior Research Analyst, Solar

Sagar focuses on PV system pricing for US and LATAM regions.

Latest articles by Sagar

-

Opinion

Liberation Day tariffs threaten to disrupt US wind and solar industries

-

Opinion

Supply shortages and an inflexible market give rise to high power transformer lead times

-

Opinion

Top 10 solar PV inverter vendors cornered 86% of the market in 2022

-

Featured

Brighter skies for US solar in 2023? | 2023 outlook

-

Opinion

Is the end of high US solar system prices in sight?

Our latest ‘Global Solar PV Inverter and Module-Level Power Electronics Market Share 2023’ report reveals a buoyant market in 2023, with 48% year-over-year growth in global PV inverter shipments.

We explored inverter vendor rankings based on careful tracking of the global landscape, using data from annual vendor surveys, public filings, project databases and dozens of conversations with industry stakeholders.

The report highlights the 2022 market leaders, their market share, and their year-over-year growth, with the aim of helping investors make more informed decisions.

Download your free extract from the report by filling out the form on the right. Or, read on for a short summary of some of the report’s key insights:

Market-leading vendors maintain their positions

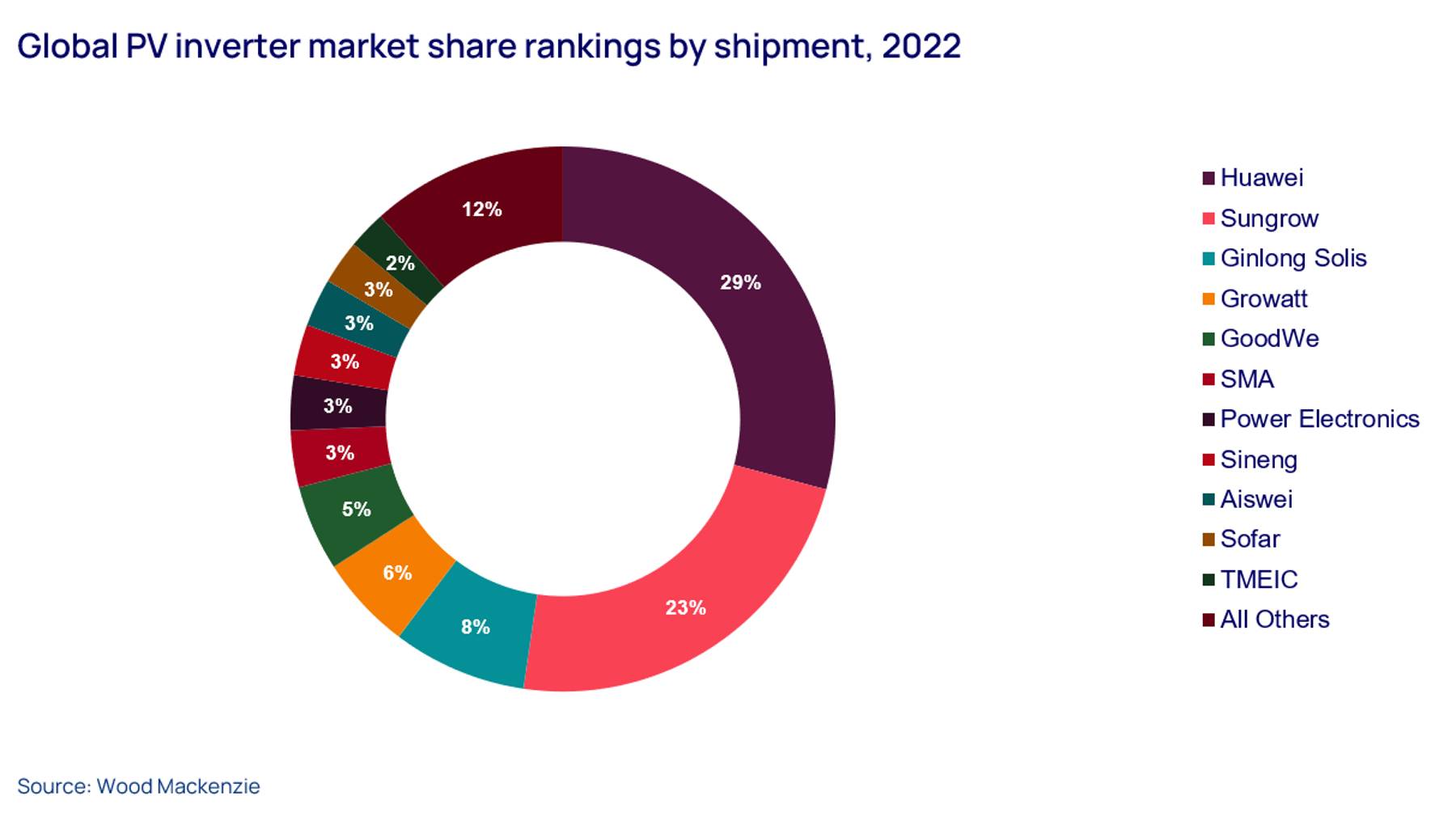

Huawei and Sungrow remained market leaders in 2022, as they have done since 2015, while AISWEI and SOFAR entered the top 10 ranking.

The top 10 global photovoltaic (PV) inverter vendors accounted for 86% of the market – an increase of 4% year-over-year, whereas the top 3 players captured 60% of the market share for shipments in 2022.

A 48% YoY increase in global PV inverter shipments

In terms of market concentration, the top 5 vendors (Huawei, Sungrow, Ginlong, Growatt, and GoodWe) shipped over 200 gigawatts (GW) of inverters, accounting for 71% of the total global PV inverter shipments in 2022 – a year-over-year growth of 8%.

{kind=link}

The market share for vendors in positions 11-20 shrank to 13% in 2022 compared to 16% in 2021. These vendors shipped 44 GW of inverters.

Overall, global PV inverter shipments saw 48% growth year-over-year in 2022, with an additional 100 GW shipped from 2021.

Improvements in chip shortages drives growth

In 2022, the PV inverter industry saw a renewed increase in shipments as the pandemic-related semiconductor chip shortage improved. Huawei and Sungrow covered 52% of the market cumulatively - an increase from 44% in 2021.

Huawei held the number 1 position for market share with an increase in shipments from 23% in 2021, to 29% in 2022. Sungrow ranked second with 23% in 2022, growing from 21% in 2021.

Ginlong Solis jumped from its number 4 ranking in 2021 to take the number 3 position in 2022, driven by the company’s shipments in China.

Increased government support in pursuit of clean energy goals

Strong growth in the PV markets in Europe, Asia Pacific and the United States drove the 333 gigawatts alternating current (GWac) of inverter shipments in 2022. Government support has increased across these regions in a bid to meet clean energy goals.

Europe held 28% of the global market for PV inverter shipments in 2022. It saw an 82% year-over-year growth following its 44% year-over-year growth in 2021. Europe’s progress is driven by its aim of achieving carbon neutrality by 2050 under the European Green Deal plan.

Asia-Pacific held 50% of the global market with a 44% year-over-year growth in shipments. Over three-quarters (78%) of inverters shipped to the region were directed to China.

The US held 13% of the global market in 2022 with 42 GWac of inverter shipments. PV-storage hybrid inverters made up 10% of the country’s shipments as it continues to integrate solar power into the grid.

Download an extract from the report

To learn more about the global solar PV inverter market shares in 2022, fill out the form at the top of the page to download an extract from the report.

Our detailed coverage of the global solar PV inverter market can help guide your investment decisions and corporate strategy, while helping you identify the primary drivers that are influencing trade and price dynamics.