What does the electric vehicle revolution mean for Latin American refiners?

Developed economies lead the charge for electric vehicles, but the impact will be felt around the world

1 minute read

The energy transition is a major shift in how the world’s population consumes energy and natural resources. It’s driven by society’s push towards a more sustainable future and facilitated by rapid technological advancement.

The electrification of transport is just one aspect of the energy transition, and will have far-reaching consequences. The dynamics of change will be different in different parts of the world.

Here’s what it could mean for Latin America, and the strategic questions it might pose for refiners.

Demand for transportation fuels will soon reach its peak

Around the world, the energy mix is changing. And while change does still need to gather pace, progress is being made to reduce the reliance on fossil fuels.

Transportation fuels currently represent ~60% of global oil demand, and new technologies are already making strides in developed economies, reducing or even halting demand growth. This has been possible thanks to higher efficiencies in traditional passenger vehicles (including hybrids) and the increasing penetration of electric vehicles (EVs).

Subsidies have played a big role in the promotion and development of these new technologies. At the same time, costs continue to fall. We now expect EVs to be competitive with standard internal combustion engine (ICE) cars by the end of the 2020s.

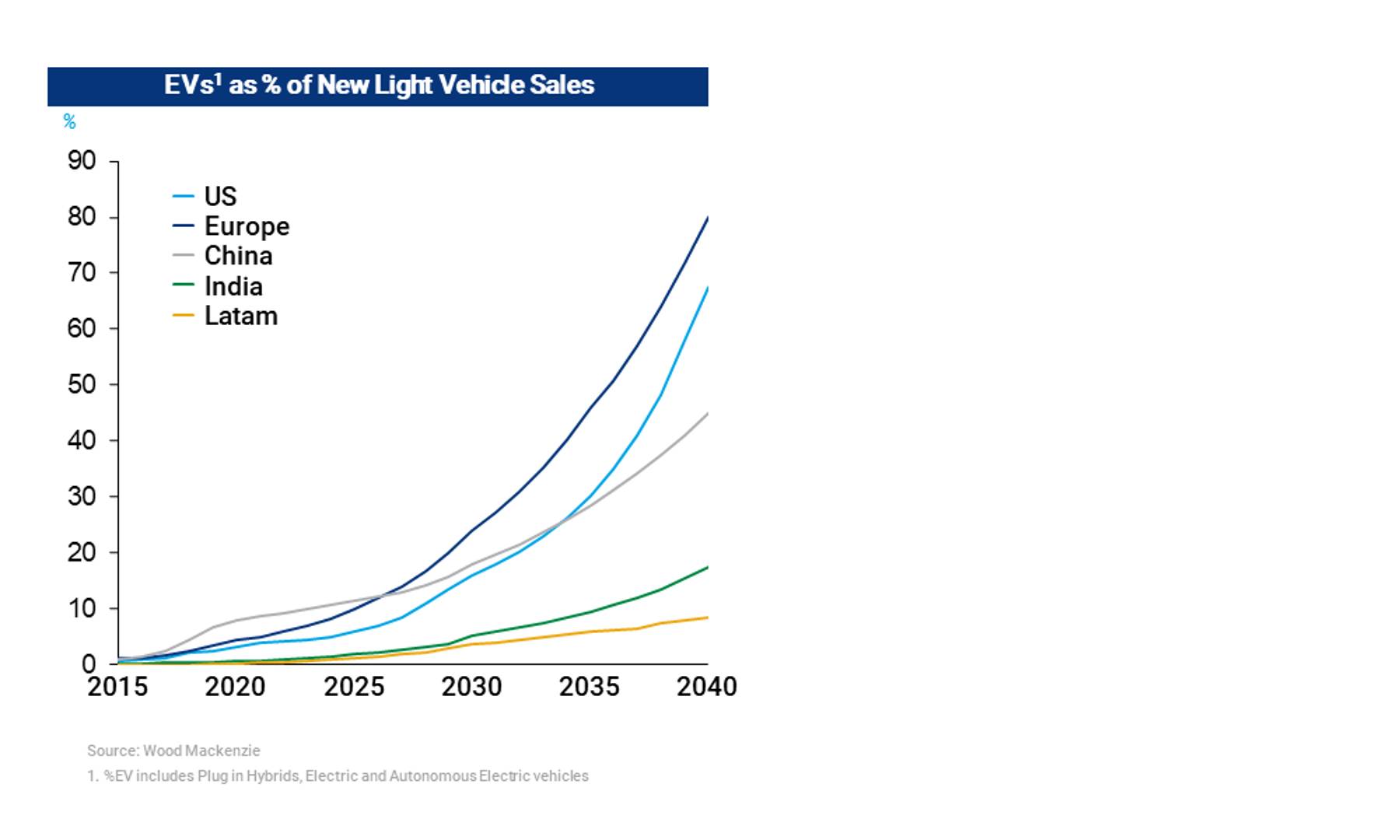

As EVs become more competitive, their penetration will rapidly increase, reaching 70% to 80% of new light vehicle sales in Europe and the US by 2040. Developing economies, including Latin America, are expected to lag as infrastructure limitations delay widespread adoption.

As these trends continue, growth in global demand for transportation fuels will continue to decline, peaking in 2031 at ~68 MMbpd.

What does this mean for Latin America?

In Latin America, there are unique dynamics in play.

Car penetration has been comparatively low, currently around 130 vehicles/’000 capita, compared to ~750 in the US and ~ 475 in Europe. But we are expecting rapid growth, driven by economic development, to increase penetration to ~190 vehicles/’000 capita by 2040.

Growth in car parc will not result in a proportionate growth in demand for transportation fuels. This disparity is due to increasing fuel efficiencies in ICE vehicles and increased adoption of EVs – albeit the latter at a lower level in Latin America as compared developed markets.

For EVs to become mainstream in this region, new grid and charging station infrastructure must be developed. This will take time, and we expect it to limit sales and penetration of EVs to big cities.

At the same time, regulatory changes could have an impact in Latin America as the world moves towards a lower carbon future. Not only incentives could accelerate EV penetration, but product spec regulations on higher content of biofuels could effectively reduce the demand for refinery fuels.

Supply-side dynamics are changing

The supply side of the equation raises plenty of questions for Latin America. Its own market dynamics need to balance out with those of the markets it interacts with, mainly the Atlantic basin.

Some of the dynamics we expect to play out in the coming years include:

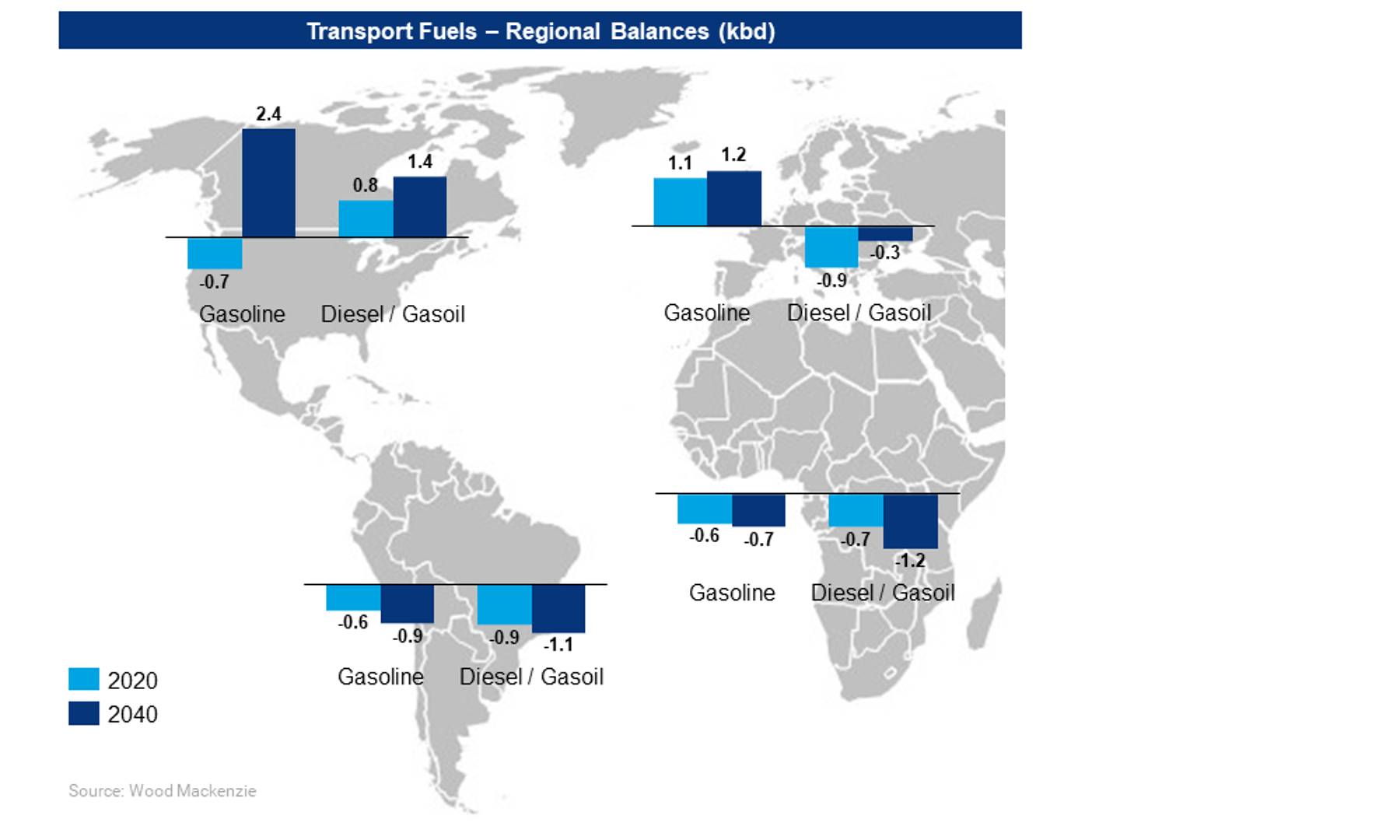

- Latin America is already short of transportation fuels by ~1.5 MMbpd. This equates to around a third of the demand. And as demand grows we expect this imbalance to increase to ~2 MMbpd by 2040.

- The Atlantic basin will move from being gasoline short to an excess, mainly driven by the evolving car fleet in the US and declining demand in Europe.

- Heavy transport vehicles will be less affected by these changes. While efficiencies will affect demand in both North America and Europe, the distillate market seems to be a safe haven for refiners in the Atlantic basin in the mid to long term.

{kind=link}

{kind=link}

{kind=link}

What does this mean for Latin American refiners?

Refiners need to adapt to a changing market and find answers to critical questions that should drive their strategies for the coming years.

- Is demand decline primarily a Northern Hemisphere problem, that will only impact Latin America in the very long term (beyond 2040)?

- Should Latin American refiners expect to operate at high utilisation under this scenario? Or even build new refineries?

- What would be the optimal product portfolio for a refiner in Latin America, given the changes in market balances and product demand?

- Are there any opportunities Latin American refiners could capture in this new environment?

We'll be discussing these topics and more at Latin America's Refining & Petrochemical Conference (LARTC) in Cartagena on 2 October, 2019.