The wind energy industry paradox: short-term headwinds and long-term optimism

Difficult times for the upstream wind supply chain as a multitude of issues deteriorate profit margins

4 minute read

Endri Lico

Principal Analyst, Global Wind Supply Chain and Technology

Endri Lico

Principal Analyst, Global Wind Supply Chain and Technology

Latest articles by Endri

-

Opinion

Wind supply chain financials decoded: colliding margins and rising prices

-

Opinion

Onshore wind: diverging cost trends, converging turbine maker strategies

-

Opinion

Future wind installations: the great divide between Chinese scale and Western strongholds

-

Opinion

Liberation Day tariffs threaten to disrupt US wind and solar industries

-

Opinion

New frontiers: order intake by Chinese wind turbine OEMs advanced beyond domestic dominance in H1 2024

-

Opinion

Wind from the east gathering strength: the outlook for OEMs

The wind energy market has grown fast, doubling in size in the past ten years. The future looks even brighter. We expect an average growth rate of 6.4% and 139 GW of installations each year from 2023-2031.

However, upstream actors within the wind energy value chain, especially turbine manufacturers and component vendors, cannot feel the full benefit of the soaring demand. Negative profit margins, impacted by unprecedented supply chain disruptions, inflation and geopolitical tensions, stand in the way.

Our Global Wind Supply Chain series draws on insight from our Global Wind Markets Service to explore the landscape of the industry. Read on for an overview of the latest edition, and fill in the form for a complimentary extract.

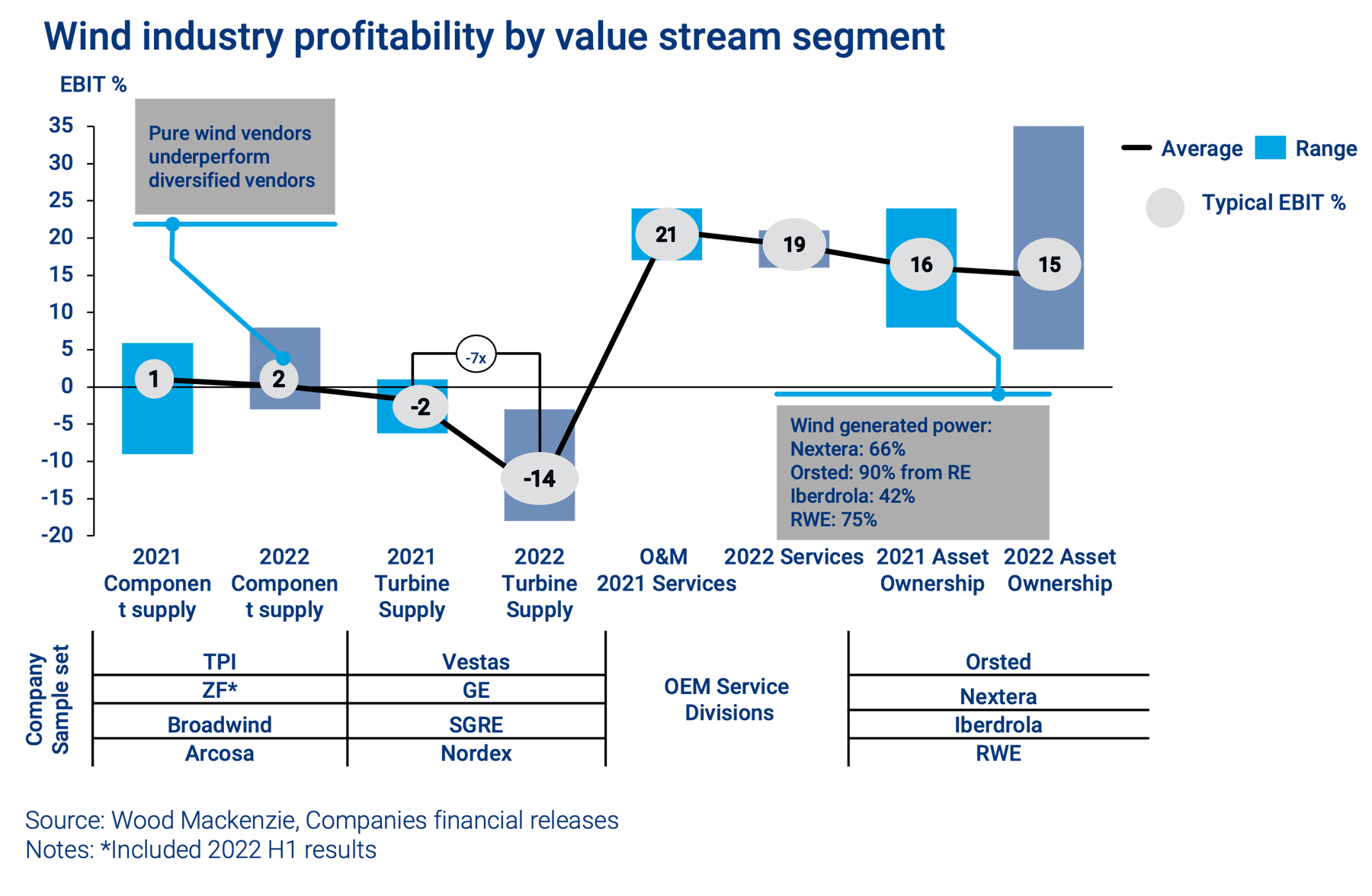

Profitability pressure varies across wind value chain

Low profits are more acute in the upstream portion of the value chain, due to a myriad of factors. Low-priced turbine orders placed years ago are now being fulfilled, due to the long lead times for turbine delivery. This exposes wind turbine original equipment manufacturers (OEMs) to dramatic raw material volatility. Large amounts of regional variability in installations, driven by policy uncertainty and permitting timelines, have left some factories underutilised, further dragging profitability.

Specialised logistics costs for massive wind turbine components have skyrocketed. This has led to project delays, higher costs and reconfiguration of the global supply chain. As a result, western OEMs lost more than €3.7 billion in the first nine months of 2022. The operations and maintenance (O&M) sector became the lone steady source of profits for OEMs supplying spare parts and technical support to the massive fleet of installed wind turbines.

On the other end of the value chain, asset owners are enjoying the best-in-class margins. They’re capitalising on record energy prices, diversifying across multiple energy sources and leveraging their size and scale to drive efficiencies in capex and opex.

Thin margins are transforming the wind energy supply chain

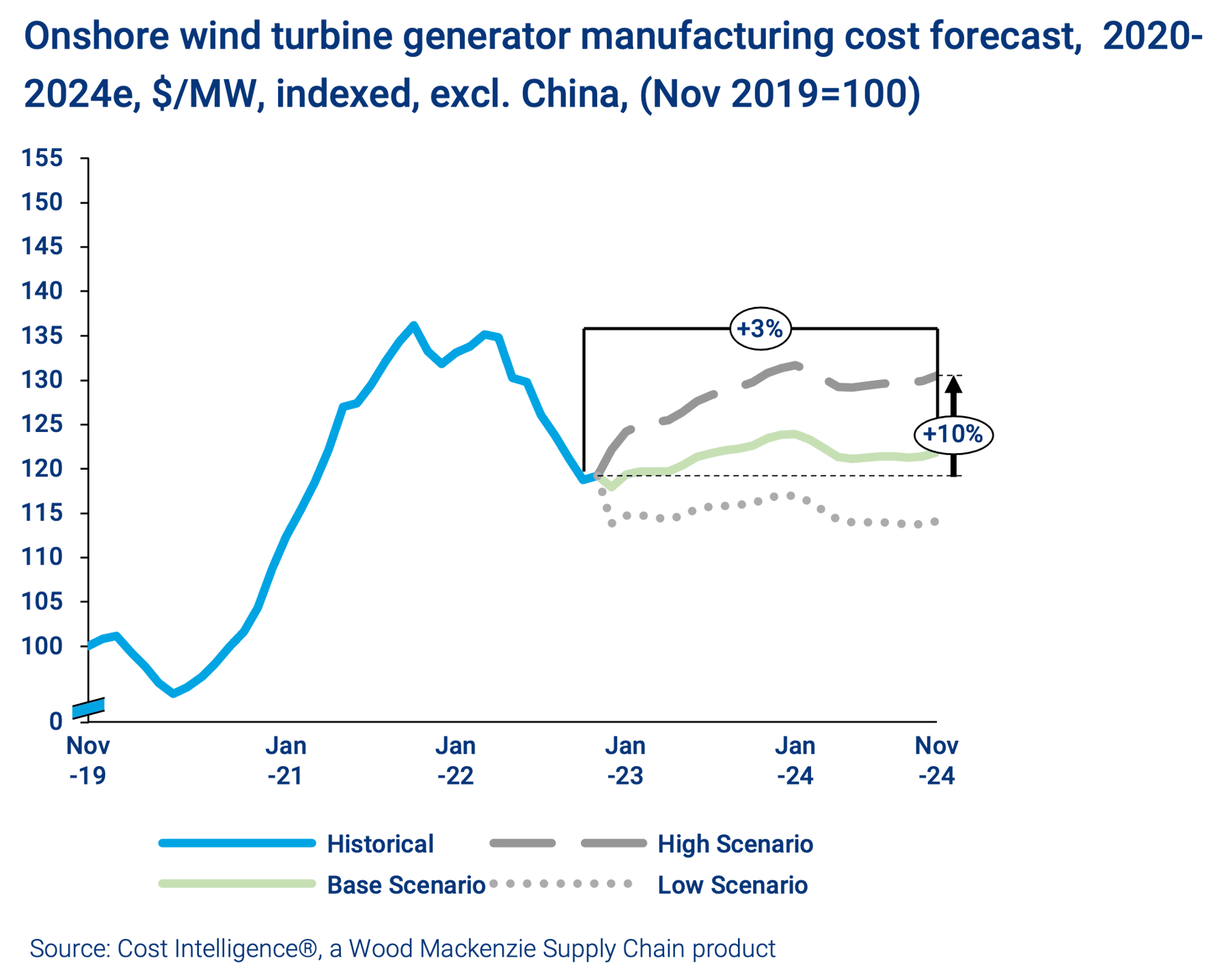

The perfect storm that hit has forced these companies to take drastic measures to reverse the current profitability challenges. The average onshore selling price (ASP) outside China has increased by close to 40% compared to pre-Covid levels in November 2019.

Western OEMs have reversed their global expansion strategy, focusing on executing profitable projects rather than prioritising volumes and market share growth. Intense cost discipline has lead OEMs to reduce headcounts, close factories, divest vertically-integrated segments of their supply chain and focus on their core business.

New product introduction has significantly slowed, particularly in the onshore segment, as OEMs seek to simplify their global product portfolio.

Huge opportunities for Chinese overseas expansion

With the Western OEMs suffering financially, Chinese OEMs see a golden opportunity to gain market shares outside China. Our research into both onshore and offshore segments indicate that Chinese OEMs are leveraging their strong financial position, massive domestic supply chain and reduced exposure to raw material and logistics volatility to reduce turbine pricing on the next generation of wind turbines that eclipse the products offered by Western OEMs.

Chinese wind companies are active across the entire wind value chain and are targeting overseas expansion through multiple channels. This is particularly focused on the emerging markets under the Belt and Road Initiative and giga-watt scale green hydrogen projects.

Chinese overseas expansion is perceived as a threat from Western OEMs and governments. It’s triggering a new wave of protectionist policies, intended to drive local job creation, reduce dependency on China and support the Western OEMs with established manufacturing presence.

As a consequence of increasing geopolitical tension and skyrocketing logistic costs, we expect a rush of new factory announcements will be forthcoming in Europe and the Americas.

Global wind supply chain shift will inevitability increase capital costs

Turbine OEMs and suppliers have just begun to feel the first signs of cost relief as the costs of specialised logistics and raw material start to soften. However, the current cost baseline remains almost 20% higher compared to pre-Covid levels.

Costs are expected to further increase by 3-5% over the next two years on our base scenario as inflation continues to affect raw material and labour costs, supply chains localise to higher costs markets and growing demand imposes shortages on critical components.

{kind=link}

{kind=link}

Key drivers for the future

Despite multitudes of factors pressuring the wind industry and supply chain in the short- to medium-term, we stand firm that all the fundamentals for sustained growth are apparent.

First and foremost, the electrification of the global economies will drive a strong demand for further wind deployment. The political mandate stands even stronger in light of the energy transition and recent geopolitical tensions. Wind energy has demonstrated that is a reliable energy source and can play a pivotal role in reducing dependency on fossil fuels and bolstering energy security.

Moreover, despite the recent inflationary pressure, onshore wind remains one of the cheapest energy sources globally, while offshore wind leads the cost reduction race. by 2050, due to capex and opex improvements and economies of scale.

Finally, technology progress and coupling wind with Power-to-X and storage offers new opportunities to tap into the full potential of wind.

Find out more about the wind industry landscape

Our report extract includes charts on:

- Wind turbine margins

- Regional manufacturing capacity

- OEM outsourcing trends

- And more.